This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008. While the median age of buyers gradually increased over the course of two decades, the COVID-19 pandemic sped it up.

It’s an excellent time to discuss housing inventory. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. How can housing inventory be so low today when it skyrocketed back in 2009? I don’t believe housing inventory below 1.52 What is going on here? housing market.

On Friday NAR reported that total housing inventory levels broke under 1 million in December, dropping to 970,00 units for a population of 330 million people. million in January down to about 4 million in December, We now have total inventory levels near all-time lows again. Unsold inventory sits at a 2.9-month months in Nov.

Both existing housing inventory and home prices have been rising together year over year, which might seem odd at first glance since existing home sales are trending near all-time lows. When you connect the dots, this is a short and simple answer to why housing inventory and home prices are both rising. Sales descended 2.8%

If there’s one sector of the economy that benefits from the very low levels of total housing inventory , it’s the homebuilders , but for a reason you might not think. If national housing inventory were back to normal, we would have 2 to 2.5 All this is happening while housing permits have fallen noticeably from the recent peak.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. This is because the biggest buyers of homes are mortgage buyers.

Inventory has broken to all-time lows, but it doesn’t look like the year-over-year data will be positive at all this year unless demand softens up. NAR Research : Unsold inventory sits at a 1.7-month NAR Research : Unsold inventory sits at a 1.7-month However, negative year-over-year inventory is not what we want to see.

The housing market of 2002-2005 had four years of sales growth facilitated by credit. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. This is significantly different than the period from 2002-2005 when credit expansion was booming. Housing inventory. Home sales.

. “This is about the same rate of price growth that occurred during the 2002 through 2006 period when subprime lending drove exuberant housing demand. “But that is where the similarities end.

Second, because of the downtrend in inventory since 2014 and the demand pick-up we will see in the years 2020-2024, we had a risk of home prices accelerating too much. It’s also driven more by mortgage buyers who tend to be older and make more money than the new-home buyers. First, total home sales should be 6.2

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. Since they were distressed forced sellers, inventory skyrocketed in 2006 and stayed very elevated in 2007 and 2008. Total inventory levels. NAR: Total Inventory levels 1.22

Inventory, which has been falling for years, broke to all-time lows in 2020. We didn’t have a seasonal push in inventory in 2020, and things worsened in 2021. Of course, this has brought back some inventory, as demand weakness always creates inventory through accumulation. million active listings, but at just 1.28

This is something that I said would change the tone of housing, and we are seeing that result this year as sales decline and inventory picks up. We were told that population growth is slowing, we were told that Americans would panic sell and that massive inventory would hit the marketplace once rates got to 4%. Wait, what? I use the 1.52-1.93

A traditional primary resident seller is also a buyer, which means if they don’t list, they’re not just taking a potential home to be bought off the table — they’re taking a future sale off the books as well. Total Inventory data fell in this report from 1.31 I am a big fan of inventory to 2019 levels. million to 1.28

The home-price growth from 2020 through 2022 has been so unhealthy that I’ve labeled this a savagely unhealthy housing market as inventory has once again collapsed on a year-over-year basis in 2022. Inventory is still showing negative year-over-year data. 2014 was the very last year total housing inventory grew in America.

Inventory levels broke to all-time lows and thus created massive housing inflation quickly, which broke my model. This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. Traditionally, inventory levels have been between 2 million to 2.5 nominal per year at most.

Home prices are skyrocketing, housing inventory is at all-time lows and homebuyers have to contend with multiple bids. Inventory velocity. April 10, 2020: We needed a lot of inventory, fast. The velocity of inventory rising in the next three months is limited. April 2022: Inventory has not recovered. Can this last?

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. If we had a massive credit boom-to-bust, inventory would have skyrocketed in 2022. NAR Total Inventory Data going back to 1982. housing credit channels have changed.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housing market trying to get national inventory levels back to pre-COVID-19 levels. Housing inventory issue with no booming demand. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. million listings.

I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers. As you can see below, we don’t have a booming credit housing market as we saw from 2002-2005; we have steady replacement buyer demand.

housing market is more tied to mortgage buyers. Unlike those two cities in Canada, we aren’t as reliant on foreign buyers to such a great extent. foreign buyers have always been less than 300,000 of total home sales for many years. from 2002-to 2005, which led to forced credit selling. In addition, the U.S.

However, the real story of 2022 is that the savagely unhealthy housing market continues as inventory is still lower than last year, sending home prices growth into double digits again. Housing demand has been stable for the past few years; we have never had a credit boom in demand since 2002-2005. Unsold inventory sits at a 2.0-month

Of course, housing starts today aren’t collapsing in the way they did from the peak of 2005 because we haven’t had a sales credit boom in recent years as we did from 2002-2005, which inflated new home sales toward 1.4 The credit cycle looks much different now than the build-up from 2002-2005.

We had more housing starts during the bubble years because from 2002 to 2005 that demand curve was higher, but it was facilitated by unhealthy credit growth. So the meager inventory in the existing home sales market has benefited the builders because it makes their products more valuable. Housing completions. From Census: Privately?owned

The one thing that has happened in 2022 that has been worse is that national inventory levels have worsened in 2022 to start the year. Inventory has been falling for years. Logan Mohtashami: People know that I haven’t been a big fan of this housing market since inventory levels broke under 1.52 months on a 3-month average.

Traditionally, housing starts, permits, and completions would move together, like what we saw in 2002-2005. The housing recession story is separate from the housing completion story and inventory backlog. From 2002-2005 it was a steady rise to the top of the housing bubble, and then it burst.

The new home sales market doesn’t have a 28% cash-buyer profile as we saw in the last existing home sales report. So, while cash buyers as a percent of sales have been growing, this sector is driven by mortgage buyers primarily. Builders have to find buyers for canceled homes, then think about their demand.

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. You could have specific buyers that need to sell their current home in order to buy a new home and don’t want to bother with it now since rates are so much higher.

Also, the market we have today doesn’t look like the credit boom we saw from 2002-2005. Housing inventory has been falling since 2014 and mortgage purchase applications have been rising since then. When demand is stable, it’s extremely rare for inventory to skyrocket and American homeowners have never looked better on paper.

can’t have a credit sales boom like we saw from 2002-2005. The builders are in a better position to manage their inventory glut than when they were working from a credit boom in 2005 that took new home sales up to 1.4 This is 12.6 percent (±16.9 percent)* below the revised June rate of 585,000 and 29.6 percent (±10.9 months and above.

The loan profile of buyers during the post-2010 expansion is excellent, so when the next job loss recession happens, we won’t lose as many homeowners (compared to what occurred after the Great Recession). The market of 2002-2005 not only had an explosion in debt growth, but the debt structures themselves were also very exotic.

This scarcity in inventory exerted upward pressure on prices, although it coincided with a 19% decline in sales. Despite this decline, motivated buyers were out there trying to secure a home while also trying to navigate lower affordability and low inventory. Average prices for closed sales increased by 7.2% Sales Decline by 18.9%

In 2002, when Dara Alperen Cipollone purchased her first home in East Boston, her real estate agent suggested she would be a great fit for residential sales. A: The obstacles Millennial real estate buyers face for owning a home in the Boston market come down to low inventory.

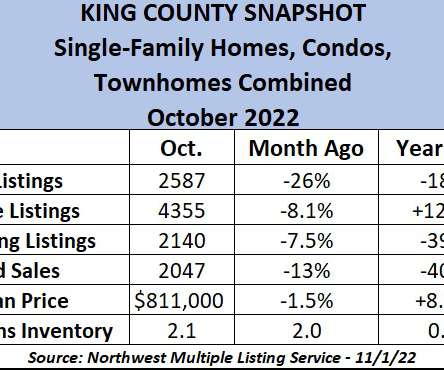

The housing market in and around King County was moving along swimmingly at the start of 2022, with homes selling briskly and buyers taking advantage of interest rates in the 3s. Historically low interest rates brought buyers and investors out of the woodwork for any homes for sale. They’re also down 19% in Seattle and 4.0%

We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. ( At least buyers will have more options and time to weigh their decision to purchase a home – but at what cost to the bottom line? Dining out. Theme parks.

I have never been a housing sales boom person because I don’t believe we can have a credit boom in America like we saw from 2002 to 2005. As we are getting closer and closer to the spring selling season, we are at fresh new all-time lows in inventory and mortgage rates, and the unemployment rate is below 4% still.

GREATER BUYING POWER Buyers who are struggling to purchase a home in this frenzied housing market will receive a bit of a lifeline in 2022. For example, a mortgage-approved buyer will be able to purchase a $938,000 single-family home (or possibly townhome or condo) with 5% down and keep within the new threshold.

In 2000 and 2002, Architectural Digest named him one of the top 100 architects in the United States. Most buyers were tech people from the Bay Area. Lower rates from week to week have helped buyers in the market, but limited for-sale inventory remains a challenge for many homebuyers.

Inventory levels. But what will happen in the future when buyers say they paid too much or lenders say the appraisal was too high or not USPAP compliant for appraisals you did in the past? My comments: Fun to look at but does it appeal to many buyers? So, what metrics are worth watching? Absorption rates and marketing times.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content