This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Last year, spring home sellers who put their house up for sale in the second half of May were able to get the most money for it. Sellers can list their house when the most buyers are seeking by focusing on late spring. Sellers might demand a greater price when there is competition among buyers for property.

Mortgage rates continue to rise, serving as a bucket of cold water for lenders and consumers that were warming to lower borrowing costs just a few months ago. According to HousingWire ‘s Mortgage Rates Center , the average 30-year conforming rate was 6.61% on Tuesday. With mortgage rates back above 6.5%

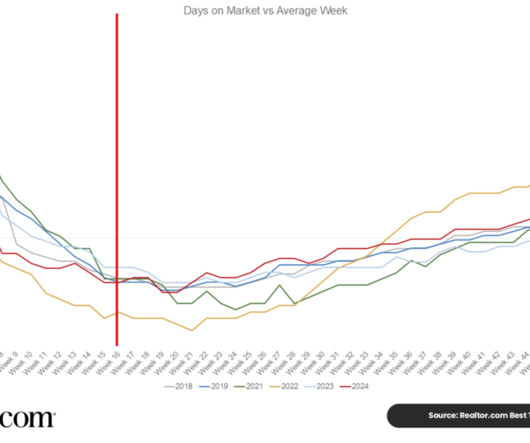

Timing is crucial in a difficult real estate market, and this year, the Realtor.com Best Time to Sell study indicates that the best time for sellers to discover the best balance of market circumstances is between April 13 and April 19. Demand may increase more quickly and forcefully if mortgage rates decline this spring as well.

That’s 12% more sellers than a year ago. It seems more sellers are coming out every week and that will keep inventory pushing upward. Mortgage rates pushed this week close to 7.25%. Its only two weeks into January and mortgage rates have hit the high end of the range we forecasted for the entire year.

The post Buyers and Sellers Embrace Market in Wake of Mortgage Rate Dip first appeared on The MortgagePoint. The post Buyers and Sellers Embrace Market in Wake of Mortgage Rate Dip appeared first on Appraisal Buzz. To read the full report, including more data, charts, and methodology, click here.

Home Sales Report , which shows that home sellers made a $122,500 profit on typical sales nationwide in 2024, generating a 53.8% Margins fell back as the increase in home values failed to keep up with larger price spikes recent sellers had been paying when they originally bought their homes. ATTOM has released its Year-End 2024 U.S.

Potential home sellers notice weak demand, fewer offers and price reductions, prompting them to back away from the market. If potential sellers avoid the market, this will keep a lid on supply growth. New listings are hitting the market Last year was an environment with 5% to 10% more sellers each week than a year prior.

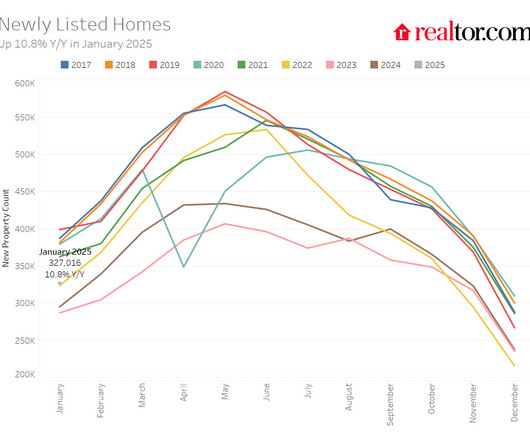

According to the Realtor.com January Monthly Housing Report, January saw a positive shift in seller activity despite recent hikes in mortgage rates, with the number of newly listed homes increasing 37.5% The uptick is likely due to some residual benefit from falls lower mortgage rates, which could fade. month-over-month.

Introduction As part of our ongoing discussion on the concept of movement in the mortgage industry, it is readily apparent that the failure of mortgage companies to pivot or tweak their business models to satisfy changing market and other conditions has resulted in consolidation based on liquidity, buyback, financial and other concerns.

As inventory builds and, as there are fewer offers from homebuyers , more sellers feel the need to reduce the asking price of the homes for sale. Sellers who dont get an offer may choose to cut their price. There are few offers being made right now, so more sellers are finding the need to reduce their asking price. There are 27.7%

As real estate practitioners adjust to the practice changes that took effect in August, and the industry waits for final approval of the NAR settlement from the court in November, questions continue about seller offers of compensation. Lowering commissions will not cause sellers to reduce their prices.

Ranking second easiest for sellers is Allentown, Pennsylvania, with 57.4% In cities like Rochester and Allentown, the combination of lower home values and high buyer demand creates a favorable sellers market, added the Calgaryhomes.ca The post Home Seller Hot Spots first appeared on The MortgagePoint. of houses sold.

But if buyers and sellers were compelled to transcribe their inaction, it would read like a sociopaths diary entry: We could have watched you grow up, but your grandpa and me werent willing to give up our 2.875% rate to move closer to you. Buyers and sellers are ready to step away from the spreadsheet and get on with living their lives.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

Higher mortgage rates are forcing many first-time homebuyers to adopt a “wait-and-see” approach to the market. Agents reported that 27% of first-timer buyers requested mortgage rate buydowns from sellers. Other agents reported that the NAR settlement complicated things for buyers and sellers.

Fast-growing mortgage servicing platform Valon has secured $100 million in a Series C funding round, the company announced this week. It is utilizing a cross-selling strategy that offers additional products to its existing customers in an evolving mortgage landscape.

This housing market is on hold until mortgage rates come down. We knew that mortgage rates over 7% were possible for the year, and here we are. I still expect well spend most of the year under 7% for the 30-year fixed rate mortgage , but until that happens, home sales are at a standstill. When will that be? I have no idea.

Economists pointed to lower mortgage rates as the reason for slower growth. Despite the Federal Reserve’s half-point interest rate cut in September, rates for 30-year conforming loans have climbed back up to 6.7%, according to HousingWire ’s Mortgage Rates Center. gain year over year, less than the 4.8% gain from July.

Indiana-based lender Ruoff Mortgage is making a move designed to help more homeowners get into new homes with ease. Ruoff Mortgage is teaming up with fintech company Calque to offer two “buy before you sell“ programs to customers. The Trade-In Mortgage — Calque’s most popular program — functions similar to a vehicle trade-in.

As 2025 draws near, mortgage rates are once again in the news. Mortgage Rates to Drop, Increase, & Drop Again in 2025 Although there are indications that mortgage rates may ease in 2025, as we witnessed in 2024, mortgage rates rarely move in the anticipated direction.

However, there are two big trends that stand out as we launch into 2025 affordability and sellers in the market. Home prices finished 2024 up a few percent nationally and mortgage rates are at their highest level in seven months back over 7% as we head into January. Theres another set of sellers that we call immediate sales.

Mortgage rates are a big variable here. In 2024, we saw a notable increase in buyer demand when mortgage rates got close to 6%. However, mortgage rates were climbing to their highest level of the year at this time in 2024. Mortgage rates now are lower than they were a year ago. This year its 2%. There are 28.7%

If 2024 was a rollercoaster, 2025 is shaping up to be a championship gameand every buyer , seller and homeowner has a shot at winning big. Although no person can truly predict mortgage rates for there are several factors involved; Industry forecasts predict interest rates will hover between 5.5% A Mortgage Agency.

Employment data for October is set to be released Friday, and it will go a long way in determining the path for mortgage rates, which have surged upward in the past month. At HousingWire’s Mortgage Rates Center on Tuesday, the average rate for 30-year conforming loans was 6.72%. This equated to homes being 9.2%

There is constant movement in the mortgage industry with the desire for growth and expansion. Thus, it has never been more important to focus on due diligence in analyzing a mortgage industry acquisition target. Regulatory compliance The mortgage industry is heavily regulated and subject to scrutiny by both State and Federal agencies.

The mortgage professional of the future goes beyond the transaction. Our mortgage industry is experiencing a fundamental shift. Traditional loan officers who focus solely on transactions are being replaced by mortgage professionals who act as financial strategists, long-term advisors, and educators.

It’s still April, so there could be as many as eight more weeks of seller growth in the spring housing market. And seller growth is happening pretty much everywhere across the country, with Florida and Texas leading the way. The bearish take is that there are many more sellers than buyers and inventory is rising. orate further?

Given the unrelenting mortgage costs, generally weak homebuyer demand, and the year’s rising supply of unsold homes, I’ve been expecting home prices to recede a bit in the second half of this year. Maybe next year, if mortgage rates stay in the high 6s, inventory will build closer to the old normal after five years of a severe shortage.

While inventory of unsold homes in the housing market in each of the last two years headed higher during September and October due to mortgage rate spikes, we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year.

The majority of homebuyers are still expecting sellers to cover their agent’s compensation, according to The Real Brokerage ’s August 2024 agent survey. While it appears that most sellers are still offering some level of compensation, 12% of agents reported they were still unsure of what the emerging trend will be. 30 and Sept.

More than half of home buyers (52%) negotiated with the seller, with 94% of those who did achieving success. About 34% of buyers paid below the asking price in 2024—up from 27% in 2022, when the market was more favorable to sellers. home ($501,500) adding $75,255, the upfront cost totals a staggering $107,230.

High mortgage rates, low inventory and sky-high prices resulted in historically low sales at a time when agents are already wrestling with the changes related to the $418 million antitrust settlement signed by the National Association of Realtors (NAR). In the current climate, homebuilders have advantages over existing-home sellers.

The recent CoreLogic Homeowner Equity Insights report for Q3 shows a continued positive trend of a lack of underwater mortgages in America today. Underwater mortgages where borrowers owe more on their home than what it is worth pose a risk of foreclosure and hinder people from selling their homes, something that was rampant after 2008.

Nearly three quarters of recent American home sellers said in a Clever survey that using a traditional real estate agent is the best way to sell. Of the surveyed pool, 42% have sold since late 2022 as rising mortgage rates cooled the post-pandemic market.

However, housing demand surged when mortgage rates fell in the early 1980s during a recession. A similar situation could occur now, but we haven’t had mortgage rates low enough for long enough to increase home sales significantly. months we saw with distressed sellers in 2008. A few key notes on the charts below 1.

Although higher home prices , rising mortgage rates and other expenses are obvious factors, there may be more to the story. “I explain to sellers that their house will sit on the market if its not fairly priced. There is some hope for potential buyers and sellers if mortgage rates decline.

According to a recent Zillow poll, nearly half of recent homebuyers who obtained a mortgage did so at a rate lower than 5%. Even though mortgage rates are currently close to 7%, many purchasers who bought a home within the last year used unconventional thinking to become homeowners.

The 30-year fixed mortgage has followed suit, recently falling as low as 6.75%, the lowest level since mid-December. Its quite obvious that stubbornly high mortgage rates slowed down early season homebuyers in the first quarter of 2025. So, mortgage rates have been declining for several weeks now. Thats a pretty notable swing.

Rising mortgage rates that are now above 7% have continued in January. Home buyers and sellers are ending a longstanding stalemate, Realtor.com chief economist Danielle Hale shared in the report. She also highlighted lower mortgage rates and a decline in lock-in effect as key drivers behind more listings in January.

Last year was weak as mortgage rates were hitting 8%. Mortgage rates were super high and inventory was building. That difference can be attributed to mortgage rates staying higher for longer through September. When you include the 9,400 immediate sales, the total is 13% more sellers than a year ago.

The MBAs mortgage applications data has been surprisingly strong. During that time, mortgage rates continually moved lower. Supply growth could also come from more sellers, such as investors or distressed borrowers unloading. However, in most of the country, we have no growth from the seller side. That’s normal.

Data from Altos Research shows an area with expensive housing, rising inventory and conditions that lean favorable to sellers. LAs housing market has largely stabilized after the turbulence of the post-pandemic years and the rapid rise of mortgage rates beginning in 2022. The current median home price is $1.47 million, $3.9

s largest metros, a monthly mortgage payment is less expensive than the average rent. In Chicago , the typical rent payment is $2,074 per month, but a monthly mortgage payment is $1,640 – a savings of nearly $434 a month by owning rather than renting. In some of the U.S.’s In Pittsburgh , the savings are about $321 a month.

In recent weeks, home sales also faltered in the face of 7% mortgage rates. Now some of them are sliding below the year prior, which is driven by relentlessly high mortgage rates. This market is at a standstill as long as mortgage rates are above 7%. Home sellers and listing agents know where demand is for homes.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content