This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The desire to invest in appraisal modernization came in third place, with 29% of lending institutions reporting that this was a top-of-mind investment. Lenders also mentioned concerns and roadblocks with adopting new appraisal modernization tools.

Fannie Mae and Freddie Mac are not designing the software for the future, but they have provided the specification for the Uniform Appraisal Data set (UAD) they want to receive. It is up to appraisal software companies to develop solutions to provide this specific data set.

What is a Reverse MortgageAppraisal? A reverse mortgageappraisal is an evaluation of a property’s value to determine how much money can be borrowed through a reverse mortgage. The appraisal is important because it helps lenders assess the risk associated with the reverse mortgage loan.

Reverse mortgages are becoming an increasingly popular financial tool for homeowners over the age of 62 who want to access equity in their homes. One important aspect of the reverse mortgage process is the appraisal, which determines the value of the property and plays a crucial role in determining the size of the loan.

This can come in the form of a pre-listing appraisal to help establish a market-supported asking price for the seller. The appraisal can also give potential buyers peace of mind that the home is accurately priced and will most likely not have any value issues when the mortgageappraisal is performed.

There has been a lot of talk about the Uniform Appraisal Dataset (UAD) and Uniform Residential Appraisal Report (URAR) redesign initiative, and how it will make life easier for appraisers. The mortgageappraisal forms we use today were designed in 2005 using technology and mortgage processes in place at the time.

Traut notes that the Federal Housing Finance Agency (FHFA) announced in late October 2021 at the Mortgage Banker Association’s annual conference that banks and mortgage lenders will be able to use desktop appraisals in place of traditional appraisals for qualifying Fannie Mae or Freddie Mac backed mortgages.

I have the tools, skills, and experience to do most of the work. CE Course: Learn about the differences between traditional mortgageappraisal assignments and foreclosure assignments in our course, Appraising REO Properties. Actually, considering holding and sale costs, this type of buyer would lose money.

. == == Appraisal Business Tips Humor for Appraisers Click here to subscribe to our FREE weekly appraiser email newsletter and get the latest appraisal news!! To read the listing with 44 photos, Click Here = The Illogical Reality of MortgageAppraisal Reviews By Dallas T. Private Island on New York’s St.

Chat GPT For Fannie Form Appraisal Reports By Dustin Harris Excerpts: The world of real estate appraisal is constantly evolving (much to our dismay sometimes), and as professionals in this field, it is crucial to stay ahead of the curve by embracing innovative tools and technologies. You don’t need a website.

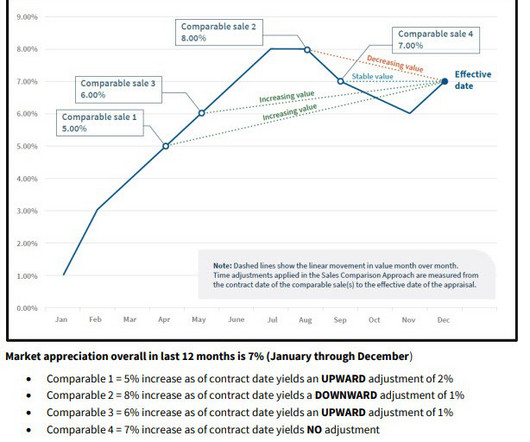

Fannie Mae encourages the use of these tools to provide supporting evidence for market trends and conditions. Failure to make market-derived time adjustments when indicated by market data is an example of an unacceptable appraisal practice.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content