This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

National appraisal management company Class Valuation is extending its reach, with the acquisition of yet another appraisal management company. Class Valuation said it would bring on AppraisalTek’s 75 full-time employees. The acquisition is Class Valuation’s fifth in recent years.

The Department of Veterans Affairs will raise appraisal fees and lengthen allowable turnaround times in select markets across the country in response to high demand for appraisals. The VA said it had taken note of increased market demand in a “seller’s market,” in a notice explaining the increases. “As

Reforming the appraisal review process is essential to maintaining the integrity of the real estate market and protecting consumers and homeowners. In mortgage financing, the appraisal process is often seen as the foundation of accurate property valuation and market stability.

By now, most appraisers are aware that Fannie Mae and Freddie Mac (GSEs) have embarked on a complete overhaul of the Uniform Appraisal Dataset (UAD). These codes, or language, make sense to appraisers but confuse uninitiated readers of our reports. Really, appraisers have always thought this way.

Indianapolis, Indiana, July 20, 2022 (AppraisalBuzz.com; Newswire.com) – SettlementOne Valuation, a leading provider of credit, data, and appraisal management services to the U.S. mortgage industry, today announced the hiring of Michelle Mencarini, Vice President of National Sales. About SettlementOne Valuation .

That’s how I first got involved in valuation technology. He taught me more than just appraisal; he taught me about life, often through a multitude of enigmatic phrases like “better than a poke in the eye with a sharp stick” or “don’t borrow trouble.” We know we are part of the valuation future as envisioned by the GSEs.

On a quarterly basis since 2014, the FHFA and the CFPB have sent surveys to borrowers who recently obtained mortgage financing. The purpose is to gather feedback on a series of ideas about the market, including consumer experiences of the mortgage process, future expectations and perceptions of the wider market.

Overall, appraisers are excited that a new player has entered the appraisal space. “As As far as Appraisal Direct goes, I want it to succeed in a massive way,” said Matthew Vasicek, chief appraiser at Expert Valuation and Consulting. “It

The bill summary was: Relates to the registration of real estate appraisal management companies or an individual or business entity that provides appraisal management services to creditors or to secondary mortgagemarket participants including affiliates by the department of state. No, it isn't.

Desktop appraisals arrived in March of 2020, allowing the housing market to keep humming while many stayed indoors to prevent the spread of COVID-19. Allowing appraisals without a walk-through was one of several flexibilities the Federal Housing Finance Agency allowed in light of the pandemic.

The appraisal is for their benefit, but at the same time, the appraiser needs to complete a fair and supportable valuation. Even though the lender is the client, the borrower is by regulation, required to be given a copy of the appraisal report. When a sale is involved, the valuation may be lower than contracted price.

After completing countless Veterans Administration (VA) mortgage loan transactions over the years, Chris Pascoe, a Marine veteran turned RE/MAX agent, has developed something of a system. Even under “normal” market conditions, VA buyers struggle to successfully purchase a home using their benefit.

It is presented as part of the GSEs “Appraisal Modernization” initiative, which aims to streamline the mortgageappraisal process. However, a closer examination reveals potential drawbacks, raising questions about its efficacy and impact on the housing market.

She may have to change from VA to conventional to be more attuned to the current market,” Williams said. If she is unable to wait the six months or more it could take to finish construction, she may forgo her hard-earned government benefit altogether. For loan originators who represent VA borrowers, the aversion to VA deals is confounding.

In a department memo, the VA explained that the move was a response to “high demand for appraisal services and limited availability of appraisers in certain local market areas.”. The VA explained that allowing desktop and exterior-only appraisals would help to reduce delays and address a longstanding shortage of VA appraisers.

Dan Sullivan of Alaska and Congressman Mike Bost of Illinois, would address a long-standing gripe that VA appraisal requirements are both lengthy and costly. Yet, on average, veterans wait longer and pay more during the closing process due to VA’s out-of-date appraisal requirements,” said Bost.

There are many areas that appraisers and agents can inform and educate one another so that each of their jobs is done more successfully. Understanding the Roles: Agents and Appraisers: Real estate agents bring their expertise in marketing and negotiations, while appraisers provide impartial and accurate property valuations.

In the dynamic world of real estate, the role of a real estate appraiser is paramount. Whether you’re buying, selling, or refinancing a property, a precise and professional appraisal is essential to ensure fair market value. Appraisal Hub Inc., At Appraisal Hub Inc., At Appraisal Hub Inc., Appraisal Hub Inc.

What is a Reverse MortgageAppraisal? A reverse mortgageappraisal is an evaluation of a property’s value to determine how much money can be borrowed through a reverse mortgage. The appraisal is important because it helps lenders assess the risk associated with the reverse mortgage loan.

Appraisers Helping Accountants In the realm of real estate transactions, residential appraisers play an important role in providing accurate valuations. Their expertise goes beyond helping buyers and sellers determine accurate market value.

If you’re selling, it’s best to schedule a home appraisal in Toronto before setting the price and listing your property on the market. An impartial appraisal can help you set a fair price and attract more potential buyers. Where Can I Find An Appraiser In Toronto? Appraisal Hub Inc.

Are you considering a reverse mortgage but unsure of what role appraisal plays? In this post, we will cover everything you need to know about reverse mortgageappraisal. We will start by discussing the basics of reverse mortgages and who can benefit from them. Why an Appraisal is Crucial for a Reverse Mortgage?

One important aspect of the reverse mortgage process is the appraisal, which determines the value of the property and plays a crucial role in determining the size of the loan. Meeting these eligibility criteria is the first step in applying for a reverse mortgage.

In the bustling real estate market of Toronto, understanding the true value of your residential property is more crucial than ever. Whether you’re considering selling your home, refinancing your mortgage, or simply looking to understand your property’s market value, a professional residential appraisal is the key.

Appraisers recently contacted by McKissock tend to agree that the profession will go generally well in 2022, with no major changes to the real estate market and no events on the horizon that could seriously upset appraisers’ business. Desktop appraisals, with information provided by third-party hirelings, may increase.

There has been a lot of talk about the Uniform Appraisal Dataset (UAD) and Uniform Residential Appraisal Report (URAR) redesign initiative, and how it will make life easier for appraisers. The mortgageappraisal forms we use today were designed in 2005 using technology and mortgage processes in place at the time.

Once the HVCC, Home Valuation Code of Conduct, is enacted the majority of lender and mortgageappraisal requests will be diverted through Appraisal Management Companies (AMCs). Although this may curb the evils of “lender pressure” on us appraisers, it will also take up to 50% of our fee!!

The technology has been drifting into mortgage lending reliance for more than a decade because it has been marketed as having the ease of “pushing a button.” The technology has been drifting into mortgage lending reliance for more than a decade because it has been marketed as having the ease of “pushing a button.”

What is a MortgageAppraisal? A mortgageappraisal is an appraisal that is done for mortgage lending purposes. Lenders, including banks and mortgage companies, require an appraisal to justify the loan they are making. Who is the Appraisal for? Appraisal vs Home Inspection.

Once the HVCC, Home Valuation Code of Conduct, is enacted the majority of lender and mortgageappraisal requests will be diverted through Appraisal Management Companies (AMCs). Although this may curb the evils of “lender pressure” on us appraisers, it will also take up to 50% of our fee!!

How To Appraise Rural Properties Excerpts: Appraising residential properties in rural areas can be both challenging and rewarding. Unlike the standardized expectations of urban and suburban properties, rural properties often present unique characteristics that require a nuanced approach to valuation.

This can include improper influence to inflate the appraised value, overlook repair items, misstate facts, ignore or conceal external influences, and misrepresent market conditions. Because of this reality, many laws and regulations have been enacted over the past 10 years to discourage improper communication with the appraiser.

This can include improper influence to inflate the appraised value, overlook repair items, misstate facts, ignore or conceal external influences, and misrepresent market conditions. Because of this reality, many laws and regulations have been enacted over the past 10 years to discourage improper communication with the appraiser.

Home negotiations can be deadlocked because of the valuation differences of a property by both prospects and homeowners. The seller wants to max out the estimate based on the growing inflation and number of renovations made, while the buyer wants the best deal in the market even as home affordability worsens. What Is an Appraisal?

Relocation appraisals play a vital role in the relocation industry by determining a property’s fair market value. These aren’t your everyday mortgageappraisals; they look into many details that matter when companies move their employees around. That’s where relocation appraisals come in.

That’s why HousingWire invited Rachel Robinson, director, collateral policy and product development at Rocket Mortgage , to HW Annual to discuss how technology can play an important role in the appraisal process and help eliminate discriminatory practices. .

I have been reading about using Chat GPT for appraisalmarketing and narrative reports, but this is the first I have read about form reports. Appraisal Business Tips Humor for Appraisers Click here to subscribe to our FREE weekly appraiser email newsletter and get the latest appraisal news!! No hassles.

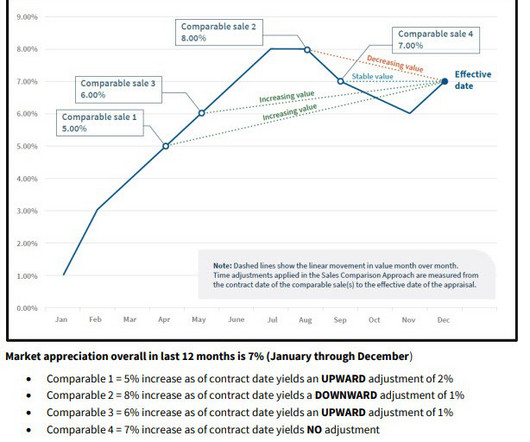

These methods provide a solid foundation for demonstrating how changing market conditions affect property values over time. Below is a detailed explanation of each technique to ensure the adjustments are well-supported and align with market trends. SEE GRAPH BELOW. FANNIE DOES NOT REQUIRE THiS TYPE OF GRAPH.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content