This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One reason that home prices have stayed elevated is that inventory nationally is still restricted. But if current trends continue, the inventory shortage will be effectively gone by next spring. In fact, while home prices are higher than a year ago, inventory has increased at the rate price appreciation has decreased.

That’s 12% more sellers than a year ago. It seems more sellers are coming out every week and that will keep inventory pushing upward. Mortgage rates pushed this week close to 7.25%. Its only two weeks into January and mortgage rates have hit the high end of the range we forecasted for the entire year.

Last year, spring home sellers who put their house up for sale in the second half of May were able to get the most money for it. Sellers can list their house when the most buyers are seeking by focusing on late spring. Sellers might demand a greater price when there is competition among buyers for property.

Mortgage rates continue to rise, serving as a bucket of cold water for lenders and consumers that were warming to lower borrowing costs just a few months ago. According to HousingWire ‘s Mortgage Rates Center , the average 30-year conforming rate was 6.61% on Tuesday. With mortgage rates back above 6.5%

Rising housing inventory levels in 2024 may not be the positive sign of market health that they appear to be. High inventory levels contribute to another problem as active listings are remaining unsold for longer periods. Redfin refers to these listings as “stale inventory.” ” According to the report, 54.5%

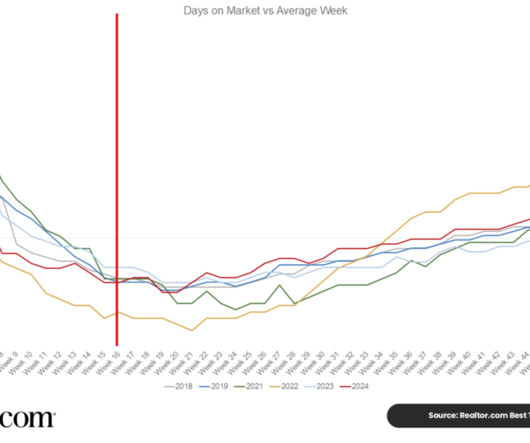

Timing is crucial in a difficult real estate market, and this year, the Realtor.com Best Time to Sell study indicates that the best time for sellers to discover the best balance of market circumstances is between April 13 and April 19. Demand may increase more quickly and forcefully if mortgage rates decline this spring as well.

Housing inventory, which saw an excellent pickup a few weeks ago, has been slowing down and last week we saw a slight decline. Has seasonality finally kicked in or did back-to-back hurricanes slow things enough to influence inventory data? Since then, inventory growth has been slowing down and even declined last week.

Altos considers anything above 30 to be indicative of a sellers market. While the markets steady conditions certainly give sellers confidence when listing their homes and ensure buyers know what to expect when entering the market the current market conditions, including higher mortgage rates , are not what many buyers would define as ideal.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

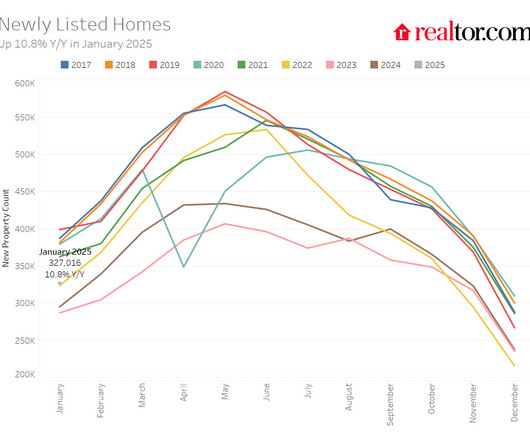

Rising mortgage rates that are now above 7% have continued in January. But there may be some improvement on the horizon as newly listed home inventory grew 37.5% more homes were actively listed for sale on a given day in January, following a 15-month trend of higher annualized inventory levels. year over year. .”

According to a report from Redfin, for-sale inventory at the end of January in Florida was up 22.7% Redfin agents in the state say that its now a buyers market where sellers have to make concessions to bring buyers to the table. Redfin attributes the rise in inventory to several factors. year over year. year-over-year jump.

In markets across the South, increased multi-family inventory is easing competition among renters and driving down prices. The post Buyers and Sellers Embrace Market in Wake of Mortgage Rate Dip first appeared on The MortgagePoint. The balance between housing supply and demand is a key factor shaping regional rent patterns.

According to the Realtor.com January Monthly Housing Report, January saw a positive shift in seller activity despite recent hikes in mortgage rates, with the number of newly listed homes increasing 37.5% The uptick is likely due to some residual benefit from falls lower mortgage rates, which could fade. month-over-month.

Redfin cited a number of reasons for this increase in the nations housing inventory, including: The mortgage rate lock-in effect is fading: A number of homeowners who scored low mortgage rates during the pandemic have been staying put because moving would mean taking on a higher rate. month-over-month, and 4.7% year-over-year.

Potential home sellers notice weak demand, fewer offers and price reductions, prompting them to back away from the market. As such, housing inventory isn’t shrinking. If potential sellers avoid the market, this will keep a lid on supply growth. This week, the new listings stat has grown with slightly more sellers.

Inventory of unsold homes on the market ticked down fractionally this week. Its not uncommon for January to have a little up and down in the inventory numbers. If inventory were jumping each week, that would be notable, but its not. At this time, of year theres new inventory and new buyers are shopping. A shrinking U.S.

However, there are two big trends that stand out as we launch into 2025 affordability and sellers in the market. Home prices finished 2024 up a few percent nationally and mortgage rates are at their highest level in seven months back over 7% as we head into January. The elephant in the room is affordability.

This housing market is on hold until mortgage rates come down. We knew that mortgage rates over 7% were possible for the year, and here we are. I still expect well spend most of the year under 7% for the 30-year fixed rate mortgage , but until that happens, home sales are at a standstill. When will that be? I have no idea.

We track inventory and home sales very closely, so the biggest surprise this year has been the resiliency of home prices. Given the unrelenting mortgage costs, generally weak homebuyer demand, and the year’s rising supply of unsold homes, I’ve been expecting home prices to recede a bit in the second half of this year. They have not.

As real estate practitioners adjust to the practice changes that took effect in August, and the industry waits for final approval of the NAR settlement from the court in November, questions continue about seller offers of compensation. Lowering commissions will not cause sellers to reduce their prices.

However, housing demand surged when mortgage rates fell in the early 1980s during a recession. A similar situation could occur now, but we haven’t had mortgage rates low enough for long enough to increase home sales significantly. For me, the highlight of 2024 was the growth in active inventory. months, not the 10.8

Inventory grew by almost 14,000 homes this week. Available inventory of unsold homes continues to grow but that growth in seems a bit less intense than it could be. Sellers can just wait it out, and it looks like the U.S. I think it’s worth examining if sellers will indeed just wait it out now. Inventory increases by 2.2%

Will inventory levels skyrocket as federal workers leave? Weekly housing inventory ramps up What do we see in the data on housing inventory levels in the D.C. Weekly housing inventory ramps up What do we see in the data on housing inventory levels in the D.C. But inventory remains well below historical averages.

As 2025 draws near, mortgage rates are once again in the news. More inventory should shake loose in 2025, giving buyers a bit more room to breathe.” In September, mortgage rates dropped, momentarily raising the proportion of affordable properties to a 19-month high. increase in property values in 2025.

We know inventory has been climbing all year. The MBAs mortgage applications data has been surprisingly strong. The northern cities have tight inventory and rising prices, some of the Sunbelt cities have the most inventory in many years, and some markets even have falling prices, too. When demand slows, inventory grows.

We already see many signals for what to expect, including last week’s data on inventory , new listings and price reductions, which I analyze below. Mortgage rates continue to move higher and that’s impacting buyers. Mortgage rates continue to move higher and that’s impacting buyers.

At the same time, mortgage rates jumped back over 7%. What were trying to track are what the real-time signals are telling us about homebuyers and 7% mortgage rates. Inventory fell There are 635,000 single-family homes unsold on the market now. Inventory falls quickly over the holidays, so this week has 2.4%

Last year was weak as mortgage rates were hitting 8%. Inventory is past peak for the year, so the momentum looks to keep the trends in a positive direction for now. Inventory drops again There are 736,000 single-family homes unsold on the market in the U.S. The inventory peak came a month earlier than in 2023.

We saw a big jump in mortgage rates last week. The 30-year fixed rate mortgage, according to the HousingWire Mortgage Rates Center , is now over 7.2% — that’s 50 basis points above where we were at the start of the year. At that time, most of the voices in the media assumed that mortgage rates had peaked and would fall by now.

The 30-year fixed mortgage has followed suit, recently falling as low as 6.75%, the lowest level since mid-December. Its quite obvious that stubbornly high mortgage rates slowed down early season homebuyers in the first quarter of 2025. So, mortgage rates have been declining for several weeks now. Thats a pretty notable swing.

The mortgage rate lockdown premise says that if rates rise, inventory can’t grow meaningfully. The idea is that nobody will trade their low mortgage rates to buy another home — even though this happened every week last year. With mortgage rates higher, will this stop inventory from growing year over year?

Recently, weve shared that the inventory of unsold homes is growing. In recent weeks, home sales also faltered in the face of 7% mortgage rates. There are already plenty of markets nationwide where the inventory of unsold homes has built up over the past few years and home prices have ticked down. this week is $421,000.

The unsold inventory of homes on the market across the country is 28% greater than last year at this time. Withdrawals keep a lid on inventory growth. That suggests a shadow inventory of homes that want to be sold but the market isnt there for it. Last year at this time, mortgage rates were heading higher to peak in May at 7.5%.

If 2024 was a rollercoaster, 2025 is shaping up to be a championship gameand every buyer , seller and homeowner has a shot at winning big. Although no person can truly predict mortgage rates for there are several factors involved; Industry forecasts predict interest rates will hover between 5.5% A Mortgage Agency.

While inventory of unsold homes in the housing market in each of the last two years headed higher during September and October due to mortgage rate spikes, we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year.

Lower mortgage rates tend to take housing supply off the market and demand has been picking up lately as rates have fallen. However, the recent drop in housing inventory has more to do with seasonality factors than lower mortgage rates. Mortgage rates and the 10-year yield The 10-year yield ended the week roughly flat.

It’s still April, so there could be as many as eight more weeks of seller growth in the spring housing market. And seller growth is happening pretty much everywhere across the country, with Florida and Texas leading the way. The bearish take is that there are many more sellers than buyers and inventory is rising.

Housing credit channels directly impact housing inventory channels. Home prices escalated out of control after 2020 and when we look at why that happened, we can see that housing credit mattered more to inventory data than most people realize. This matters because inventory was already heading toward all-time lows before COVID-19.

It’s the end of May and unsold inventory on the market is increasing across the U.S. Every state in the country has more homes on the market now than a year ago and, in many places, new construction is being completed and added to inventory, so it’s not just resale inventory that’s growing. Higher rates create more inventory.

Housing inventory, new listing data and mortgage rates are all rising, but the price cut data percentages are falling. I will watch for rising mortgage rates to see if they change the weekly data. I will watch for rising mortgage rates to see if they change the weekly data. So far, so good in 2024.

How will mortgage rates impact seasonal inventory in 2024? In the last four years, we have had abnormal seasonal inventory data, meaning that the spring inventory bottom happens later in the year. Also, when mortgage rates rise, the inventory peak happens later in the year.

As high mortgage rates reshape the housing market, existing homes are making up a larger percentage of for-sale inventory, and homebuyers are taking notice. The available inventory of existing homes rose by 22% year over year in Q3 2034. New construction inventory has grown in recent months. million units. year over year.

s largest metros, a monthly mortgage payment is less expensive than the average rent. In Chicago , the typical rent payment is $2,074 per month, but a monthly mortgage payment is $1,640 – a savings of nearly $434 a month by owning rather than renting. With inventory up 22% compared to a year ago, buyers are gaining bargaining power.

We finally have six weeks of numbers that hit my housing inventory growth model perfectly in 2024. Last year, with higher mortgage rates , we had zero weeks at this level so I am now giving 2024 inventory growth a grade of A. have higher inventory than the national data.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content