This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Homebuilder confidence in single-family homes jumped one point to 84 in February from 83 in January , according to the National Association of Home Builders and Wells Fargo HousingMarket Index. Strong buyer demand in February helped offset supplychain challenges and a surge in lumber prices, according to Chuck Fowke, NAHB chairman.

That’s up 37% from a year ago, but it’s important to take into account that the COVID-19 virus first took hold of the housingmarket in March 2020, said Doug Duncan, chief economist at Fannie Mae. A positive indicator for the housingmarket is the overall number of permits issued for single-family homes, which increased 4.6%

HousingWire spoke to housingmarket economists and mortgage industry veterans to get their take on how they believe the jobs report will impact the mortgage and housing industries. The post What a dismal jobs report means for the housingmarket appeared first on HousingWire.

I have been part of the mortgage banking industry since 1983 — 39 years to date through different housingmarkets. So when I talk to loan originators today, I harken back to my early days when fixed mortgage rates were over 14% and there were absolutely no refinances to be had.

Economists at Fannie Mae say the Federal Reserve ‘s fiscal policy is having its desired effect on the housingmarket – home price growth began to slow in the summer, and the GSE says the housing slowdown will continue through 2023. The latest forecast also projects total mortgage origination activity at $2.44

Rising interest rates and a slowing economy overall are already taking some of the air out of the rapid home-price appreciation the housingmarket has experience over the past year, according to the recently released Federal Reserve Beige Book for July. Overall, annual mortgage origination levels are expected to be $2.8

It is very good news for the housingmarket, which has suffered greatly from the affects of rate hikes over the last nine months. from a year ago, suggesting that supply-chain issues may be easing. 2023’s forward thinkers are investing in mortgage tech now. Housingmarket observers are watching closely.

Describing the modern-day mortgagemarket as challenging would be an understatement, to say the least. Mortgage interest rates have steadily ramped up throughout 2024. The average rate throughout 2024 for 30-year fixed mortgages was 6.72% higher than it was during the 2008 market crash.

The average 30-year-fixed rate mortgage climbed to 3.09% during the week ending Oct. 21, rising from 3.05% the week prior, according to the latest Freddie Mac PMMS Mortgage Survey. A year ago, the 30-year fixed-rate mortgage averaged 2.80%. The MBA has forecast purchase mortgage volume to hit a record $1.73

Thanks to a boom in the housingmarket and a historic refinance market, the past two years have been a favorable period for the mortgagemarket. In the process, a historic $9 trillion of mortgage loans were closed over two years. What are the drivers of housing demand in 2022? 2022 Forecast series.

Limited inventory, supplychain disruptions and concerns about inflation have led economists at Fannie Mae to lower their mortgage origination forecasts for the remainder of this year and into 2022. It also downsized its 2022 mortgage origination volume forecast by $55 billion to $3.25 trillion from the $4.36 in 2022.

Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the predictions for next year, along with a roundtable discussion on how these insights apply to your business. Measuring the housing deficit. The event is exclusively for HW+ members , and you can go here to register.

The average 30-year fixed-rate mortgage declined slightly to 2.86% for the week ending in August 19, according to mortgage rates data released Thursday by Freddie Mac ‘s PMMS. The week prior, mortgage rates rose to 2.87% , after six consecutive weeks of mortgage rate declines. Last week, mortgage applications decreased 3.9%

For the third consecutive week, mortgage rates pushed past 3% – with the average mortgage rate for a 30-year fixed loan up four basis points last week to 3.09%, according to Freddie Mac ’s Primary MortgageMarket Survey. Nevertheless, mortgage rates remain near historic lows (they are still 0.8

The bigger story here is that if we want to see mortgage rates fall, we need more rental units, and right now we have a massive backlog of 2-unit homes under construction — over 900,000. Traditionally, housing starts, permits, and completions would move together, like what we saw in 2002-2005.

Today, escalating real estate costs—particularly in high-cost areas—are pricing millions of Americans out of the housingmarket. Extending the traditional 30-year mortgage to 40 or even 50 years. This could provide the financial flexibility needed to make homeownership achievable for those priced out of the current market.

What is the best news for mortgage rates long-term? It’s getting more supply of apartments! The best way to fight inflation is always by adding more supply; if your goal is to destroy inflation by killing demand, that is only a temporary fix. The housingmarket is still in a recession until housing permits rise in duration.

Finally, some good news: the growth rate of inflation is cooling off for now, and with the CPI inflation report being positive, the 10-year yield fell noticeably, and mortgage rates will fall with that! This of course led some people to believe that bond yields and mortgage rates would go much higher today.

However, since I had the possibility of the 10-year yield getting to 2.42% and 4% plus mortgage rates, I accounted for that in the range. Due to this reality, I have downgraded the housingmarket from unhealthy housing to a savagely unhealthy housingmarket. The days on the market to sell a home is too low.

A stunning rise in mortgage rates, historically low levels of inventory , and skyrocketing housing prices are fueling consumer pessimism. Fannie Mae ‘s Home Purchase Sentiment Index, which tracks the housingmarket and consumer confidence to sell or buy a home, dropped by 2.1 It’s a depressing combination.

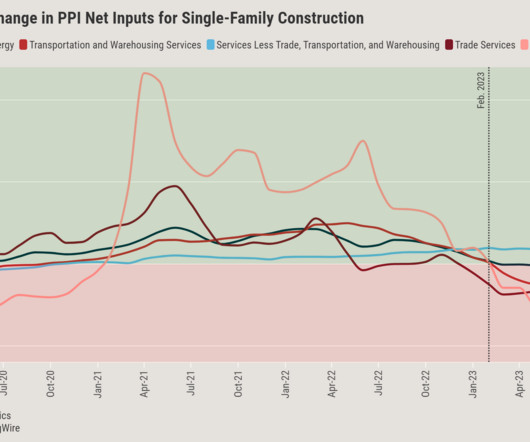

“This transaction volume is taking place against a backdrop of continuous supplychain and labor disruptions.”. months supply. Buyers are facing a housingmarket that looks to be as competitive as ever,” Handy said in a statement. This is an increase of 3.3% after a 10.4% drop in January.

However, as mortgage rates hit multi-decade highs , cooling demand and shrinking the pool of qualified buyers for new homes, homebuilders slowed their pace of construction, which settled at a plateau that is still well above pre-pandemic levels. ” However, Basu notes supplychains are already facing new pressures in 2024.

Despite this, the NAHB is optimistic that the recent drop in mortgage rates over the past two months might signal that affordability conditions may have reached their low point for this cycle of the housingmarket. In addition, Q4 also saw average mortgage rates reach a series high of 6.80%.

A homeowner is considered equity rich when they have at least 50% equity in their home, a feat more easily accomplished when skyrocketing home price appreciation widens the gap between what someone owes on their mortgage and the value of their house. The portion of mortgaged homes that were equity rich rose from 41.9%

We’ve had the sharpest and yet also the shortest recession in history, record-low mortgage rates leading to record origination volumes, and record home prices as housing demand far outstripped supply. How will the Federal Reserve respond to economic developments in 2022, and what will be the impact on mortgage rates?

Temperatures are slowly starting to rise in many parts of the country as we head into spring — and so is homebuilder sentiment, according to the National Association of Home Builders (NAHB)/Wells Fargo HousingMarket Index (HMI) report, released Wednesday. In January, the survey had 107 respondents.

Purchase mortgage rates have risen faster in the last three months than at any time since May 1994, climbing ever closer to the 5% mark due to a combination of rising inflation , the war in Ukraine, and disruptions to the supplychain. Another index shows mortgage rates even higher. Mortgage rates have increased 1.5

But what about the 1970s inflation that led to 18% mortgage rates in the early 1980s? The global pandemic created supply shortages, an extra boost in demand for goods over services, and a massive burst in inflation. Like all pandemics, disinflation follows the pandemic inflation boost as supplychains improve.

The housingmarket is no stranger to supply constraints. In doing so, he noted, three-quarters of the supplychain simply wasn’t produced. The post Doug Duncan and the housingmarket’s supply conundrum appeared first on HousingWire. This content is exclusively for HW+ members.

Housing completions were at a rate of 1.045 million in April, just 0.1% million — proof that builders are delaying housing starts due to the marked increase in costs for lumber and other materials, said Mike Fratantoni, Mortgage Bankers Association ‘s chief economist. above the March rate of 1.04

For the first time in nearly a year, homebuilder confidence moved into positive territory thanks to strong consumer demand , limited competition from the existing home sales market , and an improving supplychain. The score in June was 55, up five points from May.

Homebuilder confidence continued to rise in October despite increasing affordability issues due to rising material prices and ongoing shortages, according to the latest National Association of Home Builders (NAHB) and Wells Fargo HousingMarket Index (HMI) report released on Monday. Treasuries and mortgage-backed debt.

With a rapid spike in interest rates, inventory at historic lows, home prices rising at unprecedented levels above income, and a purchase market that is both highly anxious and digitally reliant, mortgage and real estate professionals must be strategic to capture the market opportunity today.

Homebuilder confidence remained unchanged in the latest National Association of Home Builders (NAHB) and Wells Fargo HousingMarket Index (HMI) report , holding steady at 83 for newly built single-family homes in May. The Northeast and Midwest both saw significant drops of four and three points, respectively, to 82 and 75.

The housingmarket over the summer of 2021 appears to have settled at a level lower than the surge in the second half of 2020 into early 2021,” Ben Ayers, a senior economist at Nationwide , said in a statement. Sales of new homes were down 24.3% higher than August 2020.

Consumer desire for homeownership paired with a low supply of for-sale homes were the main contributors to a red-hot housingmarket in 2021. However, the data vendor said that the market is beginning shift. months of supply. On a month-over-month basis, home price gains rose by 1.3% by December 2022. “As

Horton , the nation’s largest homebuilder by gross revenue and total closings, this week released its second quarter earnings for the fiscal year, which executives deemed “outstanding,” despite ongoing supplychain challenges , “a very tight labor market ,” and the massive uptick in mortgage rates. per diluted share.”

” More recently, Beckwitt helped Lennar navigate the most challenging housingmarket in decades. Surging mortgage rates resulted in cancelations and reduced profits for Lennar and other homebuilders, who still had persistent supplychain issues and worker shortages. billion in the same period last year.

In the first quarter of 2024, 38% of a typical household’s income was needed to make a mortgage payment on a median-priced, new single-family home in the U.S. That’s according to the Cost of Housing Index (CHI) unveiled Thursday by the National Association of Home Builders (NAHB) and Wells Fargo.

Skyrocketing mortgage rates and a slowdown in new home constructions led to a drop in home purchases in April. Mortgage applications for new home purchases dropped 10.6% in April from the same period last year, according to the Mortgage Bankers Association builder application survey.

Rising home prices, limited inventory and the uptick in mortgage rates continued to deter some homebuyers last month as sales of existing homes fell 6.6% The median existing-home price for all housing types in February was $313,000, up 15.8% Fannie Mae on how to make housing more affordable. 2020, as prices rose in every region.

Despite the decline, many industry observers see big potential for the housingmarket in the year ahead. It’s no secret that low mortgage rates and societal shifts brought on by COVID-19 have collided to form a red-hot housingmarket. But home prices have increased. Presented by: Fannie Mae. million in 2020.

Indeed, privately‐owned housing units authorized by building permits in October were at a seasonally adjusted annual rate of 1,487,000, up from 1,471,000 in September. Builder confidence declined again on Thursday for the fourth consecutive month as elevated mortgage rates have dampened homebuyer demand.

For the first time in nearly a year, homebuilder confidence moved into positive territory thanks to strong consumer demand , limited competition from the existing home sales market , and an improving supplychain. The score in June was 55, up five points from May.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content