This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housingmarket, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025. However, this year, mortgage rates rose during this timeframe.

All the housingmarket data for 2024 is in, and its fair to say that the housingmarket surprised us again! However, there are two big trends that stand out as we launch into 2025 affordability and sellers in the market. Homes are already staying on the market 20% longer than a year ago.

As 2025 draws near, mortgage rates are once again in the news. Zillow anticipates a more active housingmarket with more buyers obtaining the upper hand in 2025. In September, mortgage rates dropped, momentarily raising the proportion of affordable properties to a 19-month high. Pets deserve homes too!

The COVID-19 pandemic turned a number of nontraditional cities into housingmarket hotspots. While some of those markets have since seen a reversal of fortunes, 2025 may bring a few more surprises. Locked-in mortgages have been widely credited with cutting off housing inventory.

ATTOM has released its latest Special Housing Risk Report , spotlighting county-level housingmarkets around the nation that are more or less vulnerable to declines, based on home affordability, equity, and other measures in Q4 2024. HousingMarkets Are Most At-Risk? They included four in the Washington, D.C.,

Despite the frequency of departures, real estate agents in the state say the housingmarket remains strong. On the balance, there are still more buyers with their eye on a purchase than there are houses on the market. Statewide, the housingmarket has a 90-day average Altos Market Action Index score of 44.18

Each mortgage payment serves as a form of forced savings, helping homeowners build wealth over time. A Growing Market Force With increasing education levels, rising incomes, and financial discipline, single women are proving to be a resilient and growing force in the housingmarket. housing trends.

What will the housingmarket look like in 2025? For a more comprehensive look, read our 2025 HousingMarket Forecast covering home prices, home sales volumes and more. Mortgage rates continue to move higher and that’s impacting buyers. Frankly, it feels like the housingmarket is contracting a bit now in November.

If youre thinking about buying or selling a house and wondering about the housingmarket, youre not the only one. The real estate market has seen a lot of unusual trends in the past couple of years, so it makes sense that youd want the latest market update before you make any major decisions!

ATTOM has released its latest Special HousingMarket Impact Risk Report , a study examining county-level housingmarkets around the U.S. The report shows that California, New Jersey, and Illinois once again had high concentrations of the most-at-risk markets in the country, with parts of Florida also joining that mix.

Homebuyers have become older and wealthier Young people are having a particularly hard time in the housingmarket. First-time homebuyers face higher barriers than ever before Affordability is near-record lows as mortgage payments for the median-priced home have reached historic highs.

Dramatic mortgage rate movements are destined to play a major role in the coming year, according to Zillow ‘s newest forecast , which also calls for declining mortgage rates to be a catalyst for home-sales growth and home-price appreciation in 2025. “There’s a strong sense of dj vu on tap for 2025. million in 2025.

Realtor.com has revealed its Top HousingMarkets for 2025 , highlighting the areas ready for growth in the year ahead. foreign-born residents, and is joined by other Florida and Texas markets, which also have shares above 20%. Nearly three in four mortgage loans were government loans in El Paso, with 29.3%

Weve now been in the post-pandemic housingmarket recession market as long as we were in the pandemic boom. Does the housingmarket start to get back to normal? The number of unsold homes on the market is finally getting closer to 2019 levels. The MBAs mortgage applications data has been surprisingly strong.

Weaker demand from the local community developers buying at auction suggests continued weakness in the retail housingmarket into early 2025 given that those local community developers are anticipating retail market conditions about six months into the future,” Daren Blomquist, vice president of market economics at Auction.com, said in a statement.

Despite 2025 housingmarket predictions changing fast , there are still key themes and trends for real estate leaders to watch to best serve their clients and business. HW: What housing trends do you think will continue in 2025 and why? If we start to see them enter the market, it will be encouraging.

Earlier this year, when mortgage rates soared to 7.26%, a cloud of worry hung over the housingmarket many feared that home sales would tumble in 2025, fueled by concerns about inflation and tariffs. But when it seemed doom and gloom would prevail, the 10-year yield dropped, pulling mortgage rates lower in a lovely slow dance.

The housingmarket got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. Despite two interest rate cuts by the Federal Reserve, mortgage rates rose again and remain stubbornly high. It’s just become a more common theme.

The stagnant 2024 housingmarket is one the real estate industry cant wait to get away from, but not so for the niche luxury market. Elevated mortgage rates have stymied the broader housingmarket in 2024, but the luxury segment is somewhat insulated from that because wealthy buyers are less likely to need a mortgage.

Zillow is predicting a more active housingmarket in 2025 , but those hoping to buy — or even refinance — should buckle up for a bumpy ride and be ready to move when conditions are right. Zillow is forecasting that housingmarket activity will pick up in 2025 – but the big wildcard is mortgage rates, which will remain unpredictable.

Mortgage rates decreased again today on weak economic data, following last Friday’s similar drop in the 10-year yield. Furthermore, the mortgage spreads in today’s pricing are favorable. According to the latest quote from Mortgage News Daily , mortgage rates are now around 6.89%.

Higher prices, higher mortgage rates and limited inventory are making for a slow market among buyers and sellers alike. Real estate investors tend to be more insulated from these dynamics, particularly from mortgage rates, as they are more likely to buy properties with cash.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

Todays housing starts data exceeded estimates; however, a closer examination of the report with the builder confidence reveals that the recent rise in mortgage rates , approaching 7.25%, has negatively affected builder sentiment. Since late 2022, our analysis indicates that mortgage rates in the 6%-6.5%

Home prices firmed up in today’s existing home sales report , but we caught on to this trend two months ago with our HousingMarket Tracker. Remember that we track housing data differently than the NAR, but these are the big four from their report. However, that didn’t happen. This is something to think about for 2025.

Consumer confidence in the housingmarket improved significantly in November, rising to a score of 75.0 And a higher percentage say they expect mortgage rates will decrease in the next 12 months. on the Fannie Mae Home Purchase Sentiment Index. Only 23% believe its a good time to buy a home.

housingmarket has shown signs of slowing, demand remains strong in key Midwest and Northeast cities, where homes are selling weeks faster than the national average, according to Realtor.com s Hottest Markets Report for February. There’s just so many people here that are still looking for houses, Bradford said.

March figures to be a crucial month for gauging consumer interest in the 2025 housingmarket. The pace of home sales remains near a 30-year low point as home prices and mortgage rates keep potential borrowers in wait-and-see mode. But mortgage rates have posted an unusually large decline in the past week.

Mortgage rates are declining, and recent purchase application data shows a promising 9% week-to-week increase and a 2% rise compared to the previous year. Does this indicate that the housingmarket is beginning to wake up just in time for spring? By early 2024, mortgage rates increased slightly to 6.63%.

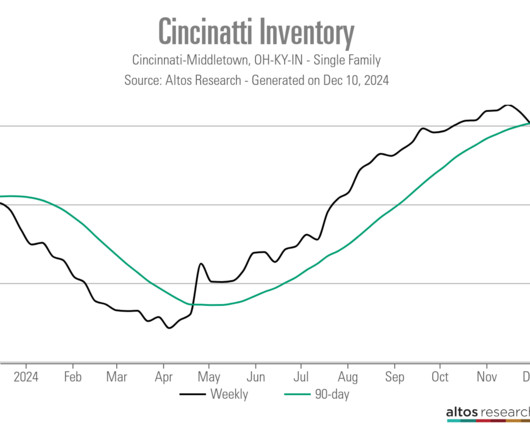

While the current focus is rightfully on containing the blazes and protecting residents, its worth taking stock of where housingmarkets stand in the affected parts of the Los Angeles metro area. Data from Altos Research shows an area with expensive housing, rising inventory and conditions that lean favorable to sellers.

Its late December so all the 2025 mortgage rate forecasts have been published. Most housingmarket analysts expect mortgage rates to spend the year with a 6 handle. The most optimistic predictions assume 2025 will see mostly low 6s for the 30-year fixed rate mortgage. Unfortunately, all of them are already wrong.

Another jobs week has come to an end, and amid the chaotic headlines about job numbers, tariffs , and the leadership of the Treasury , mortgage rates remained calm. Better mortgage spreads are limiting how high rates can rise in 2025. Mortgage spreads refer to the difference between the 10-year yield and the 30-year mortgage rate.

Today, the BLS jobs report showed that the labor market is getting softer, but it’s not breaking. This gives us a glimpse of what may happen over the next 10 months for mortgage rates, especially since, since Jan. Additionally, can mortgage rates decrease toward 6% to support builders? 14, we’ve seen them move lower.

A recent WalletHub report sheds light on mortgage delinquency rates across 100 U.S. Based on data collected between Q1 and Q2 of 2024, WalletHub’s study ranks cities according to the proportion of mortgage holders behind on payments, a critical metric in assessing financial strain within communities. The post Which U.S.

As 2024 comes to an end, mortgage rates are starting to ease, home purchase applications have hit their highest levels since January, and growing inventory is helping drive more transactions. The post Time to Get Away: The Most Desired Vacation HousingMarkets first appeared on The MortgagePoint.

Mortgage applications increased 11.2% on a seasonally adjusted basis from last week, according to data from the Mortgage Bankers Associations (MBA) weekly mortgage applications survey for the week ending March 7, 2025. The refinance share of mortgage activity increased to 45.6% of total applications from 43.8% from 16.7%

This Valentines weekend brought an unexpected gift to the housingmarket as a weaker-than-expected retail sales report sent the 10-year yield tumbling, bringing mortgage rates down to under 7%. Its been a rollercoaster week for the bond market, particularly after a relative calm in mortgage pricing.

Mortgage rates continued their ascent this week after Fridays jobs report showed that employers added more positions than expected in December, which is likely to cement a pause on interest rate cuts by the Federal Reserve later this month. when the Federal Open Market Committee (FOMC) wraps up its next meeting on Jan. in November.

A renewed interest in the senior housingmarket could also spur higher prices and waitlists, two things that lower-income older Americans can ill afford. Adding to the potential shortage in years ahead are stubbornly high mortgage rates and tariffs that could slow new construction.

Mortgage rates fell this week and they are now far from the levels widely discussed after the election. With the final jobs report for 2024, mortgage rates made a nice move lower today, and its been a positive story this week. Economic data has played a significant role in the market, unlike speculative theories.

If this happens, will we see lower mortgage rates this spring? Its an intriguing thought, especially considering how this aligns with White House officials’ strategy to boost labor supply, reduce aggregate demand, and potentially drive down the 10-year yield. Now lets look at the rest of the data impacting the housingmarket.

The 10-year yield and mortgage rates have been on a wild ride lately, even testing my top-end forecast at 7.25%, but today, the 10-year yield fell after remarks by Fed President Chris Waller about whether the Fed would do even more rate cuts than the market was anticipating. However, we know that this is unlikely to happen.

This housingmarket is on hold until mortgage rates come down. We knew that mortgage rates over 7% were possible for the year, and here we are. I still expect well spend most of the year under 7% for the 30-year fixed rate mortgage , but until that happens, home sales are at a standstill. When will that be?

The rule applies existing protections for residential mortgages to borrowers who seek PACE loans to upgrade or renovate their homes through clean energy technology. PACE borrowers were also more likely to fall behind on payments for their first mortgage compared to those who didnt use the program.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content