This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s resulting in calls to reimagine the costs of homeowners insurance (Image generated by AI in Midjourney) As the planet warms and extreme weather intensifies, the rising cost of homeowners insurance is stopping real estate deals in their tracks. Some insurers say catastrophe risk is part of the business, part of the job.

Property insurance costs for mortgaged single-family homes rose by a record $276 (+14%) to $2,290 in 2024 with average premiums now up 61% over the past five years. Property insurance costs for mortgaged single-family homes rose by a record $276 (+14%) to $2,290 in 2024 with average premiums now up 61% over the past five years.

Real estate data company StreetWire has partnered with Northern California MLS MetroList to produce an insurance product called HomeValue Lock. It’s designed to protect homeowners from declining homevalues. HomeValue Lock is currently available only in California. “As

The Consumer Financial Protection Bureau (CFPB) this month published an issue spotlight that takes a closer look at home equity contracts, or what the industry refers to as home equity investments (HEIs) that offer a lump sum payment to clients in exchange for a stake in their home equity.

Rocket Mortgage scored a big win this week after the Fourth Circuit on Thursday vacated a $10 million judgment in a class action over a decade old. Rocket Mortgage has faced other legal activity over the last year. The latest ruling from the U.S

The homeinsurance marketplace has been facing a reckoning. And it raises questions about how more of these events could impact the mortgage industry. Rethinking the dynamic Taylor Stork, president of the Community Home Lenders of America (CHLA) and chief operating officer of Developer’s Mortgage Co.

Fueled by a surge in mortgage rates , owning a home has become increasingly expensive. According to a Freddie Ma c housing and mortgage market report released Monday, while mortgage payments remain the primary pressure point for homeowners, insurance costs are emerging as a growing burden. from 2022 and up 40.8%

For most real estate industry professionals, title insurance needs no introduction. A trusted product , title insurance has been used to protect real estate transactions and property rights for over a century. Title insurance is different than most other insurance products. Diane Tomb, ALTA CEO Contributor.

The mortgage servicing landscape has long been a crucible of change, where today’s decisions lay the groundwork for the industry’s future. Formed in 2023, the MSEA is a platform for nurturing the next generation of mortgage leaders. Here’s what our panel of mortgage servicing executives had to share.

In 2013, the Federal Housing Administration (FHA) began requiring borrowers to pay the MortgageInsurance Premium (MIP) for the life of an FHA loan. People have equated FHA insurance to that of private mortgageinsurance used by the government-sponsored enterprises (GSEs), which is not life-of-loan.

Mortgage servicers, regulators and economists are closely watching the delinquency rates for Federal Housing Administration (FHA) loans following a spike in the fourth quarter of 2023. The sources spoke about these issues during this week’s Mortgage Bankers Association (MBA) Servicing Solutions Conference & Expo in Orlando.

Passage allows Congress to fund the government for 45 days, provide $16 billion in disaster assistance, and temporarily extend the National Flood Insurance Program. Each disruption caused “immediate and widespread” impacts on property sales, homevalues and consumer confidence, the National Association of Home Builders noted in a statement.

Reverse mortgage lender and servicer Longbridge Financial , which offers both Federal Housing Administration (FHA)-backed Home Equity Conversion Mortgage ( HECM ) loans as well as proprietary reverse mortgage products, announced that it has lowered the minimum homevalue for its fixed-rate proprietary products.

The American Land Title Association saw a nearly 36% year-over-year increase in title insurance premium volume in 2021 for a staggering $7 billion spike, according to the trade group’s Market Share Analysis , published Friday. The title insurance industry generated $26.2 The title insurance industry generated $26.2

In late June, Susan Gregory received an estimate for a new homeowner’s insurance policy on her 120-year-old St. Augustine, Florida property, after her previous insurer, United Property and Casualty, went insolvent earlier in the year. “It can’t be my forever home if I can’t afford it.”

Despite rising interest rates , higher home prices and a drop in refinance volume , the American Land Title Association recorded $5.89 billion in title insurance premium volume during the first quarter of 2022, compared to $5.68 The title insurance industry had a record year in 2021 , generating $26.2 Doma Title Insurance Co.

The federally insured reverse mortgage known as a Home Equity Conversion Mortgage (HECM) is unique, as are the rates that impact the HECM product. Keep in mind that almost all HECMs are adjustable-rate mortgages (ARMs), and so each rate update will concentrate on ARMs.

Despite the potential for uncertainty ahead, reverse mortgages continue to be a positive addition to the overall portfolio of Ellington Financial. Multiple times over the course of the call, company leaders lauded the contributions of Longbridge Financial , its wholly owned reverse mortgage lending and servicing subsidiary.

The average 30-year fixed-rate mortgage was stagnant at 2.88% for the week ending Sept. 9, according to mortgage rates data released Thursday by Freddie Mac ‘s PMMS. The week prior , mortgage rates also held steady at 2.87%. A year ago at this time, the 30-year fixed-rate mortgage averaged 2.86%.

The Q3 patternsderived from gaps in affordability, underwater mortgages, foreclosures, and unemployment trendsrevealed that two-thirds of the 50 counties around the U.S. homevalue currently stands at $359,099, up 2.6% Less-vulnerable markets continued to be clustered in the Southern U.S. According to Zillow , the average U.S.

The increase reflects rising home prices, which went up 40% since the beginning of the COVID-19 pandemic , mainly due to a lack of inventory, according to the study. It’s also due to growing property taxes and homeowners insurance premiums as providers exited states where risks are elevated.

The Home Equity Conversion Mortgage ( HECM ) and the Home Equity Line of Credit ( HELOC ) remain as the primary options left for older homeowners who want to use their home equity to create more liquidity during retirement. It also allows the homeowner to draw a portion of the home’svalue, but only for a defined period.

However, the rising costs of insurance, property taxes, and housing have dampened local relocation rates. The lock-in effect of high mortgage rates also plays a role, as homeowners hesitate to leave lower-interest loans for costlier options. As a result, local movesoften spurred by desires to upgrade homeshave dropped significantly.

The roots of racial disparities in housing and mortgage markets run deep. Historic government institutionalized discrimination includes actions like “redlining,” where the Federal Housing Administration would refuse to insuremortgages in and around Black neighborhoods. Justice Department charges of fair-lending violations.

Building the future of mortgage servicing technology is about granular, nuanced innovation — knowing what changes must happen and when, and executing with no mistakes across scale operations where every tiny detail is highly regulated. and see the same data their customer is seeing.

Home equity continued to rise in the first quarter of 2024 as residential properties with mortgages collectively gained $1.5 homeowner with a mortgage added $28,000 in equity during the year ending in March 2024 — the highest year-over-year increase since late 2022. of those with mortgages underwater.” The average U.S.

Bankrate compiled the typical costs of property taxes, homeowners insurance, and home maintenance, which was estimated to be 2% of a home’svalue per year. states, the average single-family home, priced at $436,291, according to Redfin , costs $18,118 each year. Insurance prices are another burden for homeowners.

An historic home in Chicago ’s Austin neighborhood designed by architect Frank Lloyd Wright in 1903 is in serious need of repairs and renovations, but an existing reverse mortgage loan is complicating the process of initiating the work. Fannie Mae reportedly assigned the loan to PHH.

Using a 1-10 scale, the portal displays current risk factors for a property as well as the expected change for each risk in 15 and 30 years, the length of a typical mortgage. The cost of homeowners insurance policies has skyrocketed in the past two years as U.S. insurers have grappled with exponential growth in natural disaster claims.

Finance of America Reverse will soon debut a hybrid product that combines elements of a reverse mortgage with a forward mortgage. The lender says it’s an innovative approach to servicing borrowers who are in retirement age but don’t qualify or wish to refinance into a long-term mortgage. Presented by: MCT.

Good news: Mortgage rates will likely continue going down in 2025! The Federal Reserve (aka the Fed) lowered the federal funds rate in November, and mortgage rates should continue going down in response to that cut. 1 And lets not forget that mortgage rates have already fallen quite a bit. Will Interest Rates Go Down in 2025?

Builders feel more confident in the market, housing inventory data is positive and buyer demand for mortgages has increased — but don’t be fooled. In addition, the credit rating agency expects mortgage rates to move even higher in 2023 and home prices to decline by up to 5%. “We

The fate of Federal Housing Administration (FHA)-backed mortgages in the ongoing downcycle housing market is being compared with a canary in the coal mine by several industry experts who track the sector and are seeing early warning signs of distress. Over the past 14 years, FHA has insured 9.1 million in mortgagesvalued at $1.7

Reverse mortgage educators Dan Hultquist and Jim McMinn brought their “Rules of the Game” presentation back to this year’s National Reverse Mortgage Lenders Association (NRMLA) Annual Meeting and Expo in San Diego. Wilson,” began McMinn to a hypothetical reverse mortgage customer. The whistle blew immediately.

trillion mortgage servicing sector shouldn’t be “disrupted” by financial technology, it should be reimagined with fintech. Most new-to-mortgage fintech folks who overuse the word “disruptor” will start by asking, “What are your requirements?” In mortgage servicing, it’s not about “disruption” for the sake of sounding innovative.

in October—fueled by rising housing and insurance costs—and mortgage rates having edged back above 7%, homeownership remains a distant goal for many living in the U.S. Yet each of these states faces unique real estate hurdles that shape the prospects for both home sales and rentals. inflation climbing to 2.6%

“As Americans continue to amass record levels of equity in their homes, they need tools that increase access and reduce stress, particularly as they struggle to manage high interest rates , inflation , personal debt, and other obstacles to reach their long-term financial goals.”

According to a new Zillow Home Loans analysis , monthly mortgage payments have grown less expensive than rent prices in 22 of the 50 largest U.S. Recent dips in mortgage rates, which have fallen to the lowest level since early 2023, have significantly reduced monthly payments. homevalue currently stands at $361,282, up 2.9%

They own the home with their name on the title, as with any mortgage, traditional or reverse. They own the home with their name on the title, as with any mortgage, traditional or reverse. The HECM for Purchase is not a refinancing tool; it is not akin to a Home Equity Line of Credit ( HELOC ).

VeroFORECAST evaluates home prices in over three hundred of the nation’s largest housing markets, and the company is committed to the data science of predicting homevalue based on rigorous analysis of the fundamentals and interrelationships of numerous economic, housing, and geographic variables pertaining to homevalues.

Top wholesale lender United Wholesale Mortgage (UWM) is the latest originator to join the resurgent home-equity lines of credit (HELOC) market. Meanwhile, the piggyback HELOC, which provides an additional loan taken out on property alongside a first mortgage, is ideal for borrowers with less available for a down payment.

Does the cost of homeowners insurance affect the price of a home? In recent years, insurance companies have pulled out of some markets altogether after sustaining massive losses due to wildfires, flooding, and other climate-related disasters. In some markets, the answer is increasingly yes.

A proper home appraisal is essential whether purchasing or selling a property. This appraisal is used by mortgage lenders to calculate the maximum amount they will lend on a property. Computer models have been used by participants in the mortgage and real estate industries over the years to determine the worth of a property.

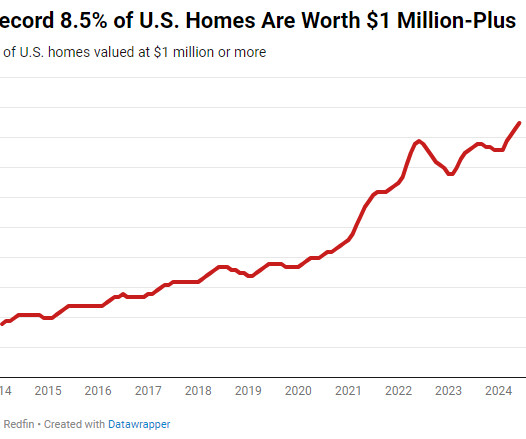

The record high in home prices—the median sale price nationally increased by 4% in June—has led to a record high in the percentage of American homesvalued at $1 million or more. Recent declines in mortgage rates have given buyers a small respite, increasing their purchasing power by tens of thousands of dollars.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content