This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And while the slower sales pace may not be great news for real estate professionals, it has resulted in an uptick in inventory , which is good news for homebuyers. For-sale inventory at the end of September was 1.39 month supply of unsold inventory, up from 4.2 million, up 1.5% from August and up 23% from one year ago.

.” A combination of soaring insurance rates and new regulations on condo association reserves and building maintenance work has created a surge in condo inventory in Florida. Inventory has also been surging — it was up to nearly 10,000 units last week, a sharp rise from about 6,300 a year ago.

The difference is mortgage rates: even with inventory growing at a healthy clip this year, mortgage rates just heading down toward 6% for a brief period of time resulted in higher prices in a seasonally soft period. I discussed this on Yahoo Finance this morning. However, that didn’t happen. million in October.

This housing market is on hold until mortgage rates come down. We knew that mortgage rates over 7% were possible for the year, and here we are. I still expect well spend most of the year under 7% for the 30-year fixed rate mortgage , but until that happens, home sales are at a standstill. When will that be? I have no idea.

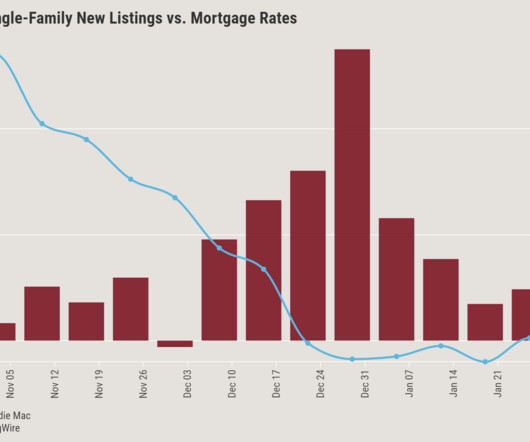

A 60 basis point increase in mortgage rates in October has strangled mortgage demand, particularly for refinancings , according to the latest survey data from the Mortgage Bankers Association. Mortgage applications overall decreased 0.1% The refinance share of mortgage activity decreased to 43.1% the previous week.

The mortgage rate lockdown premise holds that very few people will list their homes when mortgage rates are this high, thus suppressing inventory. 2024 has had healthy inventory growth despite mortgage rates above 7%. Each time, inventory has squared right into the model as long as rates stay elevated.

Stubbornly high rates have hindered mortgage demand , but at least it’s better than it was a year ago. Mortgage applications decreased 6.7% from one week earlier, according to data from the Mortgage Bankers Association ’s (MBA) weekly applications survey for the week ending Oct. Refinances comprised 45.7%

Mortgage applications decreased 17% from one week earlier as mortgage rates surged, according to data from the Mortgage Bankers Association ’s (MBA) weekly application survey for the week ending October 11, 2024. The refinance index decreased 26% from the previous week and was 111% higher than the same week one year ago.

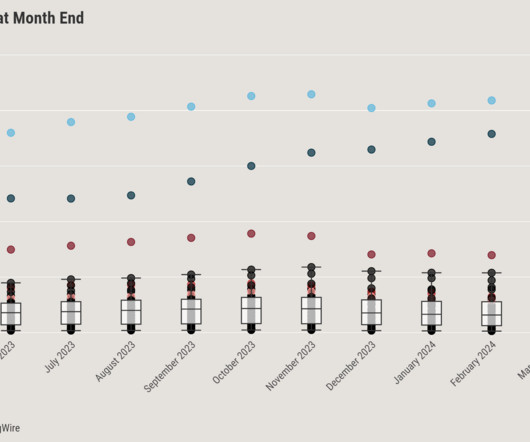

Have we seen the peak in housing inventory for 2024? The best part about 2024 has been that higher mortgage rates have created an inventory buffer, so if the economy gets softer and rates fall, we have many more homes to work with than we had in 2020-2023. Weekly inventory change (Aug.

Mortgage applications declined 0.7% 13, driven by slight decline in refinance activity, according to data released Wednesday by the Mortgage Bankers Association (MBA). The decline in applications broke a five-week streak of increases in mortgage demand. Adjustable-rate mortgage (ARM) activity remained steady at 5.3%

Mortgage applications increased 5.4% 6, stemming from a 27% jump in refinance activity, according to a report released Wednesday by the Mortgage Bankers Association (MBA). This is the latest weekly increase in mortgage applications, following a trend of steady demand increases over the past several weeks. share a week prior.

Home prices finished 2024 up a few percent nationally and mortgage rates are at their highest level in seven months back over 7% as we head into January. In fact, at $2,290, the typical mortgage payment for homebuyers is starting this next year at the highest level ever. The elephant in the room is affordability.

Department of Housing & Urban Development (HUD) will co-host the “Mortgage Market Resilience and Access to Credit Summit” on Tuesday, October 15 at HUD’s headquarters. Independent mortgage banks play a key role in making this a reality, and this summit will shine a spotlight on their essential contributions to our housing market.”

We track inventory and home sales very closely, so the biggest surprise this year has been the resiliency of home prices. Given the unrelenting mortgage costs, generally weak homebuyer demand, and the year’s rising supply of unsold homes, I’ve been expecting home prices to recede a bit in the second half of this year. They have not.

Housing inventory finally hit my target level of growth last week with mortgage rates now over 7.25% , something I couldn’t get all last year. This is something I talked about last week on Yahoo Finance. This is something I talked about last week on Yahoo Finance. This sent the 10-year yield and mortgage rates higher.

Housing credit channels directly impact housing inventory channels. Home prices escalated out of control after 2020 and when we look at why that happened, we can see that housing credit mattered more to inventory data than most people realize. This matters because inventory was already heading toward all-time lows before COVID-19.

After tumbling over the past few months, existing-home sales are giving real estate and mortgage professionals a reason to smile. The worst of the downturn in home sales could be over, with increasing inventory leading to more transactions,” NAR chief economist Lawrence Yun said in a statement. Inventory was up 19.1%

At the same time, mortgage rates jumped back over 7%. What were trying to track are what the real-time signals are telling us about homebuyers and 7% mortgage rates. Inventory fell There are 635,000 single-family homes unsold on the market now. Inventory falls quickly over the holidays, so this week has 2.4%

It seems more sellers are coming out every week and that will keep inventory pushing upward. Mortgage rates pushed this week close to 7.25%. Its only two weeks into January and mortgage rates have hit the high end of the range we forecasted for the entire year. This week inventory dipped though, so well see what happens next.

Unsold inventory in the two biggest housing markets in the country, Texas and Florida, declined this week. Inventory seems to have peaked for the season and is slowly inching down. First, mortgage rates are falling, whereas last year they were rising. Inventory growth is slowing as mortgage rates fall.

As high mortgage rates reshape the housing market, existing homes are making up a larger percentage of for-sale inventory, and homebuyers are taking notice. The available inventory of existing homes rose by 22% year over year in Q3 2034. New construction inventory has grown in recent months. year over year in September.

Last fall when people were still expecting mortgage rates to be falling this year, it was common to assume rates would be in the low 6s or 5s this year and people asked me if lower rates would bring a flood of inventory. The only way inventory would grow in 2024 is if mortgage rates climbed.

Last year was weak as mortgage rates were hitting 8%. Inventory is past peak for the year, so the momentum looks to keep the trends in a positive direction for now. Inventory drops again There are 736,000 single-family homes unsold on the market in the U.S. The inventory peak came a month earlier than in 2023.

We know inventory has been climbing all year. The MBAs mortgage applications data has been surprisingly strong. The northern cities have tight inventory and rising prices, some of the Sunbelt cities have the most inventory in many years, and some markets even have falling prices, too. When demand slows, inventory grows.

Unsold inventory of homes for sale has been on the rise all year. It hasn’t turned the corner yet — inventory rose across the country this week — but at less than 1% rate. There are some signs that inventory growth is slowing with newly lower mortgage rates and the end of the summer. Texas inventory grew by 1.5%

The pricing surge comes despite a marginal dip in weekly average mortgage rates , which fell from a five-month high of 7.22% to 7.02% at the beginning of May, according to Freddie Mac. The market continues to grapple with insufficient inventory , Redfin reported. The median U.S.

Homebuilders are still getting squeezed by high mortgage rates. The drop in sales is causing a rapid rise in unsold inventory. Though new home inventory in June remained elevated at a 9.3-month Though new home inventory in June remained elevated at a 9.3-month That’s according to the U.S. That represents a decline of 7.4%

However, mortgage applications for new home purchases increased 4% between July and August, the strongest pace of sales in three months. Homebuilders are still benefiting from very low inventory of existing homes for sale, which has driven more buyers to consider new construction,” Bright MLS Chief Economist Lisa Sturtevant said.

Describing the modern-day mortgage market as challenging would be an understatement, to say the least. Mortgage interest rates have steadily ramped up throughout 2024. The average rate throughout 2024 for 30-year fixed mortgages was 6.72% higher than it was during the 2008 market crash. Finance a loan, and you may lose money.

Only your personal situation and finances should do that! Housing inventory will likely still be low in 2025, and demand could increase. Good news: Mortgage rates will likely continue going down in 2025! 1 And lets not forget that mortgage rates have already fallen quite a bit. Will Interest Rates Go Down in 2025?

An often misguided premise I see on social media is that lower mortgage rates are doing nothing for housing demand. Purchase application data First, purchase apps is the fastest way to look for positive or negative data at higher or lower mortgage rates. Weekly housing inventory data Higher rates lead to more inventory.

With mortgage rates briefly topping 8% and home prices breaking records throughout the year, many would-be sellers simply decided not to bother listing their homes, exacerbating already tight inventories. Mortgage rates followed suit, walloping buyers’ purchasing power. New data from the U.S.

Mortgage rates headed higher last week after the CPI inflation report , but now, with news of a wider war in the Middle East, should we expect even higher rates? 10-year yield and mortgage rates There is nothing good to report on mortgage rates from last week. The week ahead will answer some of those questions early on.

That puts the national inventory up 31.9% Brokers and agents , mortgage officers and other housing professionals continue to compete for their share of tight volumes and would need major industry growth to get back to 2019 levels. year-over-year, extending a 24-week streak of year-over-year increases.

“The housing market remains structurally underbuilt, and homeowners with locked-in low mortgage rates are keeping existing-home inventory limited. And that “lock-in” rate may continue as Freddie Mac reports that the 30-year fixed-rate mortgage (FRM) averaged 6.44% as of October 17, 2024, up from last week when it averaged 6.32%.

Mortgage rates moved massively lower last week without any Federal Reserve rate cuts, primarily because the labor market is getting softer. Can mortgage rates go even lower? We don’t have that variable this year and spreads have improved earlier than I thought, which has helped mortgage pricing.

But for first-time and other cash-strapped buyers—those who are not relying on the proceeds of a home sale, who may be using a 100% financed VA loan, whose agents may be layering forms of assistance to put together enough cash for closing—knowing in advance about the seller’s contribution to their agent costs may be essential.

Elevated mortgage rates sank builder confidence again in November, but recent economic data suggests housing conditions will pick up in the coming months. On the construction side, homebuilders as well as land developers found it hard to finance projects because of high short-term interest rates.

Agency loans have limitations such as loan amounts, only allowing up to ten financed properties and they don’t accept five to nine units. Ground-up construction growth will be high to meet the population growth and meet the demand due to limited inventory. Rehabs will be invaluable to reopen inventory.

This is an excerpt of a HousingWire Research report titled: What Everyone Needs to Know about Mortgage Rate Lock-in, by Altos President Mike Simonsen. housing market saw dramatic changes in affordability as mortgage rates skyrocketed 500 basis points. million in January 2021 (when mortgage rates were 2.7%) fell to 3.9

Nationwide equity on mortgaged homes soared to a record $16.9 The recent trend of rising interest rates has dampened homebuyer demand and allowed the inventory of homes for sale to improve,” Andy Walden, ICE’s vice president of enterprise research strategy, said in a statement. homeowners with mortgages have tappable equity.

“A national secondary market for construction financing could allow lenders, like state housing finance agencies and banks, to provide the investment capital needed to get multifamily housing projects built and keys in families’ hands.” There are many policy levers that must be pulled to get there,” the report reads. “A

Mortgage rate lock-in happens because even small changes in mortgage rates can make a big difference in costs. in April 2024 — with a 10% down payment, a typical mortgage would be approximately $350,000. For every 50 basis point change in mortgage rates, the monthly payment for this house would change by $112.In

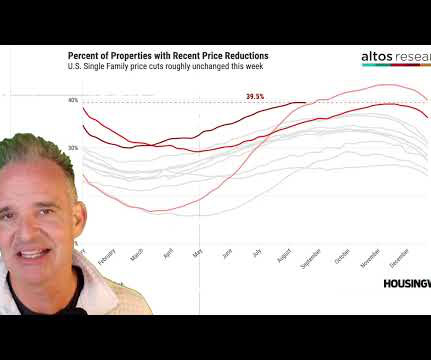

Even with demand buoyed by a sparse housing inventory, growing financial challenges for buyers are forcing home sellers to cut prices to close deals, a new Redfin research report found. And because mortgage rates have been above 7% for about two months consecutively, the cost of financing is extreme. the month prior.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content