This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Zillow Home Loans — the platform’s affiliate mortgage lender — pushes the future of financing. Users can enter a potential home price, down payment, interest rate, loan terms, propertytaxes, insurance costs, and homeowners association (HOA) fees. Click Here

Health care information and caregiving marketplace website Care.com published an article that examines several practical ways that someone could choose to finance their long-term care (LTC) goals. The reverse mortgage industry has aimed in recent years to position itself as a potential avenue to fund LTC directly or pay for LTC insurance.

While some homeowners prioritize their mortgage payments, those who are not financially prepared may face significant challenges due to other essential and frequent expenses such as homeowners insurance, propertytaxes, utilities, repairs, and maintenance. Census Bureau. However, their dollars are not the only thing at stake.

Among homeowners who have a mortgage escrow account, only 52% fully understand how the account works, according to survey results released Thursday by propertytax services provider LERETA. In 2023, 60% of the calls were related to escrow accounts, specifically shortages due to rising propertytaxes or insurance costs.”

The home insurance marketplace has been facing a reckoning. With the death toll from Helene crossing the grim milestone of 230 this week — and with thousands of impacted homes without flood insurance wiped away — this could lead to a ripple effect that drives homeowners insurance premiums even higher.

It’s also due to growing propertytaxes and homeowners insurance premiums as providers exited states where risks are elevated. Bankrate calculated the average annual cost of owning a single-family home based on items such as propertytaxes, homeowners insurance and maintenance costs, as well as energy, internet and cable bills.

What’s more, operating costs for apartment and SFR (single-family rental) operators are up significantly since 2019 due to higher propertytaxes, insurance, and payroll costs. We believe rates (including financing rates) staying higher for longer will delay any rebound in construction activity in the near term,” he wrote.

Yet ‘renting by choice’ is also on the rise as it offers flexibility, less financial commitment, and freedom from the burdens of propertytaxes, maintenance, and insurance. In Florida, rising insurance premiums tied to natural disasters like hurricanes can make homeownership more of a liability than an asset.

Duffy has 15-plus years of senior-level experience in housing finance. Incenter’s business channels include capital markets, loan diligence, student lending, insurance, propertytax, accounting and marketing solutions.

This is according to experts who spoke to personal finance website Bankrate about the concept of taking on a new mortgage in retirement. Even if one owns a property with no further mortgage payments due, propertytaxes and upkeep will be a consideration,” Bankrate senior economic analyst Mark Hamrick said. “As

To boot, one of the first financing transactions on record was made in January 2022 by technology firm TerraZero. Section F: While there is no need for homeowners insurance, “mortgage” insurance and prepaid interest may still make sense in this scenario. As for propertytaxes, well, you can kiss that goodbye.

There’s a growing sense that affordable housing is a stable investment class for banks and insurance companies; even in the 2008 – 2009 recession, it held up well.”. For instance, it’s possible that housing tax credits and other supports for affordable housing could be sacrificed or functionally negated by propertytax increases.

For example, recently, Fannie Mae has focused on expanding alternatives to title insurance as a way to supposedly increase homeownership affordability. However, Fannie Mae’s own research from 2022 found that title insurance is not a significant component of the overall closing costs when buying a home.

Other holding costs for real estate include taxes and insurance. According to S&P Global, insurance premiums increased nationally by 34% between 2017 and 2023, with even more increases hitting homeowners in 2024. In particular, insurance can be a significant portion of monthly payments.

While the researchers cite a number of outside experts it consulted, including the American Enterprise Institute and economists from both the Federal Housing Finance Agency and Fannie Mae, it did not consult with any fair lending experts. Private mortgage insurance makes up about one to three percent of total costs, the report found.

The CFPB advises that upfront fees can be “as much as $6,000 plus closing costs in an initial mortgage insurance premium,” in addition to an annual mortgage insurance premium and obligations related to propertytaxes and homeowners insurance. So, as the loan balance increases, your home equity decreases.”

In a blog post published Thursday, Mortgage Bankers Association (MBA) President and CEO Bob Broeksmit made the case that the Federal Housing Finance Agency ‘s (FHFA) loan level price adjustments (LLPA) related to a mortgage borrower’s debt-to-income (DTI) ratio is unworkable and should be scrapped entirely.

As long as you retain ownership of the home and pay the propertytaxes, the loan will not become due.” “It can be used to make home repairs, pay for medical expenses, or to supplement retirement income. A lender makes monthly payments to you based on the equity in your home, using your home as collateral.

At the end of August, the District of Columbia Housing Finance Agency (DCHFA) announced that it had relaunched its Reverse Mortgage Insurance & Tax Payment Program (ReMIT), which originally began in 2019 and expanded in 2020 before being halted at the end of 2021.

As home prices rise and propertytaxes and insurance bills soar, it’s become ever more difficult to age in place,” the article stated. “As This is according to a column published this week by NextAvenue. “As

They’ll need a small amount of information about your income and finances, and if all looks good, they’ll give you a preapproval letter stating how much money you can likely borrow. Most lenders require you to pay for home insurance and propertytaxes as part of your monthly payment.

Longbridge Financial, LLC, (NMLS #957935) believes that the answer to this dilemma is the HECM/Reverse for Purchase financing option. Most real estate agents, builders and potential customers have no idea that this financing option exists to purchase homes,” he said.

Homeownership-related costs also grew, with insurance premiums rising an average of 21% from May 2022 to May 2023, and propertytaxes on the rise as well. nationwide average increase in owners’ insurance premiums. Almost 25% of homeowner households are stretched dangerously thin, including 27.4% of elderly homeowners.

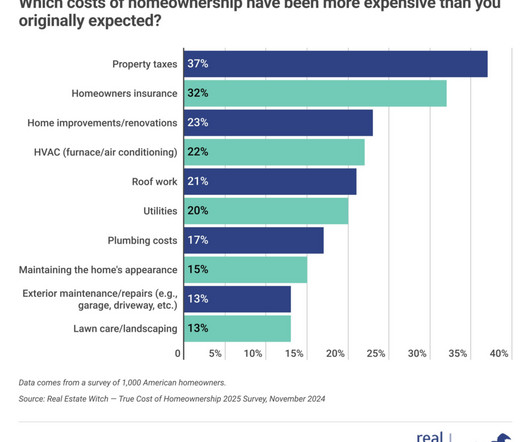

Increasing Costs are Taking a Toll on Homeowners’ Personal Finances Many home seekers have revised their budgets and savings goals in light of decreased inventory levels in a number of cities. Cost hikes for utilities (83%), house insurance (81%), propertytaxes (81%) and repairs (74%), according to homeowners, have been experienced.

former Federal Housing Financing Agency (FHFA) director Mark Calabria made the argument that a larger credit box has caused the government-sponsored enterprises (GSEs) to take on far more risk than they should be. . At policy panels held by the Community Home Lenders of America (CHLA) on Monday in Washington, D.C., It sure as hell does.

Insurance premiums are up 27.7% Labor costs for property management have increased nearly 50% in some markets, and security needs and costs have risen, too. High interest rates and inflation mean the cost of reinvesting in properties is expensive. Rising operating costs add to the pressure. The capital markets can help too.

home price increase translated into a monthly mortgage payment of $1,179 on a median-priced home — not including propertytaxes and insurance. On average, the price of the renovated properties was 3.5 Even with an average 30-year fixed rate mortgage of 2.84% in August , the 14.9% for all existing home sales nationwide.

It assumed a 10% down payment and did not factor in propertytaxes or homeowners insurance. “In contrast, millennials on average faced the lowest mortgage burdens, thanks to a decade of ultralow interest rates following the Great Recession.“ For millennials turning 30, the typical mortgage payment has averaged only 22.5%

That requirement is important to protect reverse mortgage borrowers, who remain responsible for propertytaxes, insurance, and other applicable fees and assessments,” the CFPB stated. However, many borrowers could not get in contact with anyone at the loan servicing operation.

If a person passes away without an end-of-life document, a property often becomes heirs’ property, meaning that it is passed informally to the next generation without a proper title documenting ownership. Besides not having the ability to monetize the property, heirs’ property holders can also lose economic value in other ways.

For buyers of a median-priced home, the monthly mortgage payment—assuming a 20% down payment—amounts to about $2,300, not including propertytaxes and insurance,“ said Ratiu. The cost of financing a median-priced U.S. home, assuming a 20% downpayment, rose 12.4% million.

That policy required a 30-day “first look” auction during which only qualified nonprofits, government entities and owner-occupant buyers could bid on foreclosed properties with loans insured by the Federal Housing Administration (FHA). of all properties available for the first-look auctions during the quarter.

There are several reasons why someone may want to get a real estate appraisal: Buying or selling a property: If you are buying or selling a property, an appraisal can help determine its fair market value, which can be useful in negotiations and setting a listing price.

Even though rents are high here, the insurance rates and propertytaxes are also high, making it difficult for the numbers to make sense for investors,” Bob Benson, a Redfin Premier agent in Fort Lauderdale, said in the report.

If not, you should first spend some time shoring up your finances. Qualifying for financing is a critical part of the home-buying journey. When considering the overall cost of homeownership, the price of insurance and propertytaxes will vary based on community and location,” Ross says. based in Troy, MI.

He said in addition to SFR operators starting to see rental growth rates slow, or even decline in some areas, as leases turn over, they also have “seen propertytaxes and cost structures increase materially.”. “So,

The monthly house payment to buy a renovated foreclosure — assuming a 5% down payment, the going 30-year fixed mortgage rate at the time of sale and including propertytaxes and insurance — represented just 20% of the median family income in the surrounding Census tract.

There are pros and cons that will be different for everyone based on finances, the type of home you dream of being your forever home, and the availability of the homes in your market. Propertytaxes are less on a smaller home with a lower appraised value. 3 advantages of purchasing a starter home are: Price. Less maintenance.

To Dana Dillard, principal advisor at Housing Finance Strategies and a 25-year mortgage industry veteran, the ghosting problem happens, among other reasons, because homeowners deny the reality or feel overwhelmed with their debts — especially if they lost a relative or friend due to COVID-19 or are unemployed for a while.

Here’s what you need to qualify for a loan, plus the rundown on five financing choices. How First-Time Homeowners Can Utilize Financing Options Buying a house involves saving considerable cash and borrowing the remaining funds necessary to make a purchase is the norm. They can be conforming or nonconforming. Conforming

Meanwhile, several looming threats could potentially pull out the cushion completely, including rising “hidden” homeownership costs of insurance and propertytaxes in many markets, rising delinquency rates for consumer debt such as credit cards and auto loans, and falling values and rising defaults in segments of the commercial real estate market.

What contingencies impact sellers before closing on a house While the burden is on the buyer to finalize financing for the home purchase and to obtain homeowners insurance , some contract contingencies will impact you, too, especially if you’re living in the home.

Taxes and Assessments. Indemnity and Insurance. The lease agreement is not automatically extended at the end of the period, and it is necessary to change the lease agreement for further use of the property. And the landlord pays for all operating expenses, such as maintenance, propertytaxes, and insurance.

For some of us, owning a home might seem like it is impossible without two incomes for financing purposes. Financing Options for Single Parents Perhaps one of the biggest decisions of homeownership for single parents is how much house you can conceivably afford, and deciding out what financing options are most advantageous to you.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content