This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Earlier this year, when mortgage rates soared to 7.26%, a cloud of worry hung over the housing market many feared that home sales would tumble in 2025, fueled by concerns about inflation and tariffs. But when it seemed doom and gloom would prevail, the 10-year yield dropped, pulling mortgage rates lower in a lovely slow dance.

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025. However, this year, mortgage rates rose during this timeframe.

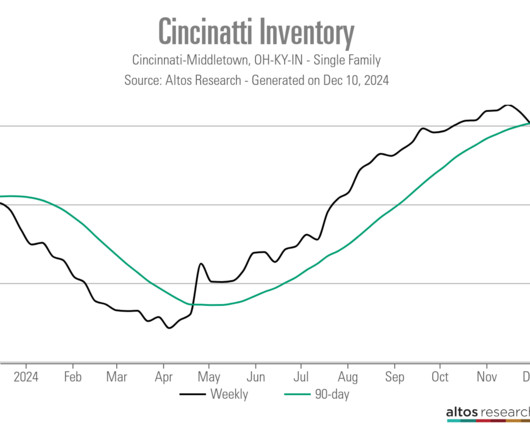

The housing market got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. Despite two interest rate cuts by the Federal Reserve, mortgage rates rose again and remain stubbornly high. A substantial drop in newlistings is a contributing factor.

The mortgage rate lockdown premise holds that very few people will list their homes when mortgage rates are this high, thus suppressing inventory. 2024 has had healthy inventory growth despite mortgage rates above 7%. When mortgage rates increase, demand falls, and the price-cut percentage grows.

Have lower mortgage rates already started to slow down housing inventory? Now, with mortgage rates dropping below that 7.25% level recently, inventory hasn’t been able to hit that growth model once. However, 2024 looks much healthier than 2023 data, as we desperately needed to get off those historically low levels of active listings.

Mortgage rates have made almost a 2% move lower from the highs of 2023. Now that the jobs week data is in, the question is: can mortgage rates go even lower? Mortgage spreads Another way for mortgage rates to drop to the lowest level of the forecast or below is to improve mortgage spreads.

The best part about 2024 has been that higher mortgage rates have created an inventory buffer, so if the economy gets softer and rates fall, we have many more homes to work with than we had in 2020-2023. However, as mortgage rates have fallen recently , I haven’t been able to hit my targets, which isn’t a surprise.

The MBAs mortgage applications data has been surprisingly strong. During that time, mortgage rates continually moved lower. Newlistings on trend Nationally, there were just 31,000 newlistings for single-family homes from the last week which included Thanksgiving weekend. We know sales are inching up, too.

Mortgage rates headed higher last week after the CPI inflation report , but now, with news of a wider war in the Middle East, should we expect even higher rates? 10-year yield and mortgage rates There is nothing good to report on mortgage rates from last week. The week ahead will answer some of those questions early on.

Despite a small spike in recent months, newlistings of homes for sale are still below pre-pandemic levels in parts of the country because the majority of homeowners say they will never sell. Additionally, a lot of people are taking their time to learn more about the new regulations regarding real estate agent fees.

We survived jobs week and Federal Reserve Chairman Jerome Powell talking to Congress, with mortgage rates ending the week below 7%. But will mortgage rates keep heading lower? Mortgage rates and the 10-year yield The 10-year yield is the key for all my housing work, so I focus on it religiously. We haven’t broken either yet.

These events led to lower mortgage rates and increased purchase application data last week, but decreased housing inventory. Here’s a quick rundown of the last week: The 10-year yield had a Lord of Rings battle at a critical technical level, pushing mortgage rates lower at the end of the week with no real break in the bond market.

The holiday season is here, and despite higher mortgage rates last week, housing demand is displaying some festive resilience. Mortgage rates picked up last week, though that hasnt significantly impacted our pending contract data, which is showing some positive year-over-year growth when we compare it to 2022 and 2023.

“The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. This means what we saw in 2005-2008 with the inventory spike was a historic event that hasn’t been replicated at any time in recent U.S. economic history. .

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? However, mortgage rates have fallen more than 1% since the recent highs, so it’s time to look at the data to explain how to interpret it.

While weekly inventory is still falling, we have year-over-year growth in total active listing and newlistings data. This calls into question a mortgage rate lockdown, as mortgage rates are also higher year over year. For the first time in a while, this was a good week for newlisting data.

I have a simple model with mortgage rates being above 7.25%: weekly inventory data should grow between 11,000-17,000 per week. This isn’t saying too much since 2023 had the lowest recorded level of newlistings ever, but it’s still a plus in my book. The mortgage spread data got worse last week. 2022: 19.2%

Mortgage rates fell last week after the debt ceiling issues were resolved, but the damage from higher rates took its toll on purchase application data again. Here’s a quick rundown of the last week: Active inventory grew 3,180 weekly , and newlisting data fell week to week and is still trending at an all-time low in 2023.

Total housing inventory growth has been slow in 2023, but with rising mortgage rates over the last few months, inventory has grown a bit faster than average. But even with mortgage rates getting as high as 8%, we’ve yet to hit within that range. Last week, mortgage rates rose toward 7.56%. Weekly inventory change (Nov.

Mortgage rates were near 7% last week but purchase applications were still able to pull out an 8% week-to-week gain. Active housing inventory grew while newlisting data fell. Mortgage rates hardly budged last week, even with the Federal Reserve ‘s announcement it was pausing rate hikes and CPI inflation reports.

The 2023 housing market faced one of the same roadblocks we saw in 2022: mortgage rates were too high for home sales growth. Here’s my forecast for 2024: 10-year yield and mortgage rates For 2024, the 10-year yield range will be similar to 2023, but with a few different variables to watch. Instead, they closed 2023 at 6.67%.

housing market , we just experienced an event that most people never thought could happen. From NAR : “December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates ,” said NAR Chief Economist Lawrence Yun. During that period, we saw newlisting data decline.

Mortgage rates were again in a small range, hanging near 7%. However, the real positive story here is that even with newlisting data trending at an all-time low, we are getting the growth in active listings we traditionally see in the spring and summer. Purchase apps had a small week-to-week gain.

After the series wraps, join us on February 6 for the HW+ Virtual 2023 Forecast Event. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the top predictions for this year, along with a roundtable discussion on how these insights apply to your business. months nationally.

Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the data for this year, along with a roundtable discussion on how these insights apply to your business. The event is exclusively for HW+ members , and you can go here to register.

Some popular real estate newsletter content includes: Market updates Featured listings Industry news Local news Community events Agent profiles Investment opportunities No matter what content you choose to include, your real estate newsletter should serve as a meaningful touchpoint that continuously builds your client relationships.

Even though this was a beat of estimates, the sales decline trend due to higher mortgage rates and home prices continues. The savagely unhealthy housing market theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . million in August.” million in August.”

On the one hand, elevated mortgage rates continue to erode buyers’ purchasing power, and in some markets, home prices are falling. The number of newlistings coming on the market this spring is lower than it has been in more than a decade. After this series wraps, join us on May 30 for the next Housing Market Update Event.

Inflation has hit younger households hardest, and stubbornly high rates have pushed a mortgage out of reach for many first-time buyers. The largest drops were in New Orleans (-5.9%), Austin (-4.1%), and San Antonio (-2.2%). The typical mortgage payment is up 11.3% more newlistings compared to last year.

The housing market madness persisted last week as inventory fell and higher mortgage rates took a bigger bite out of purchase application data. Weekly housing inventory decreased by 6,801, while newlisting data is still negative year-over-year. Then rates went up almost 1% over several weeks, completely reversing the gains.

When I came up with the “ savagely unhealthy housing market ” label in February of this year, it was based on the premise that the housing inflation story that we have had to deal with since 2020 was a historical event. And we aren’t talking about your grandfather’s mortgage rates rising; we went from 2.5%

To give you an idea how different this year is from last year, last week in 2022, active listings grew 30,940 while this year they only grew 5,848. Mortgage rates rose last week after the better-than-anticipated jobless claims data but even with higher rates, we also had a third week of positive purchase application data.

The price of newlistings continues to rise, which is a very bullish indicator for sales prices in the coming months. From September 2017 through November 2018, the 30-year mortgage rate rose from 3.8% If interest rates climb above 4.5%, we’re likely to see this pattern repeat, which would add some more listings to inventory.

Mortgage rates fell as the banking crisis got worse and purchase application data grew for the second week in a row, but the big question is: Did we hit the seasonal bottom in housing inventory? Newlisting data collapsed, but we are putting an asterisk on that data line for this week. Weekly inventory increased by 1,734.

metropolitan areas in February 2022, based on year-over-year growth in median listing price according to the residential real estate listing website, Realtor.com. The table also reports the year-over-year percent change in newlistings for each market. Table 1, below, reports the 10 hottest U.S. Bellingham, WA 51.7% -8.3%

Summary Planning your open house Marketing your open house Hosting your open house Open house follow-up ideas The full picture Open house ideas: Planning your next event Not every one of your clients wants or needs to hold an open house, but you can certainly play up your open house events to help you reach your real estate career goals.

He also makes note of a common interest rate system in which negative economic events would cause interest rates to drop, but now a positive global picture would lower rates instead. Unemployment, job losses and foreclosures are going to drive newlistings, more listings, lower prices, and more buyers come to bat.”

This is why we brought HousingWire Lead Analyst Logan Mohtashami, Kate Amor, senior vice president and head of enterprise products at Guaranteed Rate , and Arjun Dhingra, who lead sales and business development at All Western Mortgage , together for a preview of the information you can expect to hear at HousingWire Annual in Austin Texas, from Oct.

Two weeks after Helene hit, Movement Mortgage loan officer Mitch Davidson still has no power or running water at his Asheville home — and he says it could be months before they return. Newlistings and pending home sales data from Altos Research captured the housing markets around Asheville coming to a screeching halt.

Similar to past experiences, Hurricane Helene may lead to 5% of mortgage borrowers in affected areas becoming delinquent but eventually self-curing over the next 12 months, according to a Bank of America (BofA) analysis. Just days later, Hurricane Milton struck Florida, making landfall in Sarasota County with winds reaching 120 mph.

70 towns, 90 newlistings Local agents say the county’s tight inventory situation is largely to blame. “We We have been complaining about the lack of inventory for as long as I can remember, but then we at least had more listings,” Danny Yoon , an Edgewater, New Jersey-based Sotheby’s International Realty agent, said.

Mortgage rates fell along with bond yields, showing that mortgage rates peaked on Oct. The weekly data shows some good news for the housing market ! With mortgage rates also falling, I am hopeful that more people will list their homes and buy another, so we can get back to a more functional housing market.

Bringing together some of the top economists and researchers in housing, this event will provide an in-depth look at their latest insights on the housing market, along with a roundtable discussion on how this information applies to your business. To register for the HW+ event, go here. The impact on housing markets.

It’s packed with stylish templates for social media, events and more. Forming partnerships with mortgage brokers can be mutually beneficial. These events are platforms to connect with potential buyers, showcase your expertise and raise visibility throughout your local community (and online, if you stream them via webinar!).

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content