This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Earlier this year, when mortgage rates soared to 7.26%, a cloud of worry hung over the housing market many feared that home sales would tumble in 2025, fueled by concerns about inflation and tariffs. But when it seemed doom and gloom would prevail, the 10-year yield dropped, pulling mortgage rates lower in a lovely slow dance.

If all economic factors, political factors and world events are fine, we just kind of flatline. In order to alleviate some of the pressure on buyers, agents like JD Gieson would love to see more inventory come on the market. They dont want to give up those low rates or even a small remaining mortgage for a 6% rate, Feinstein said.

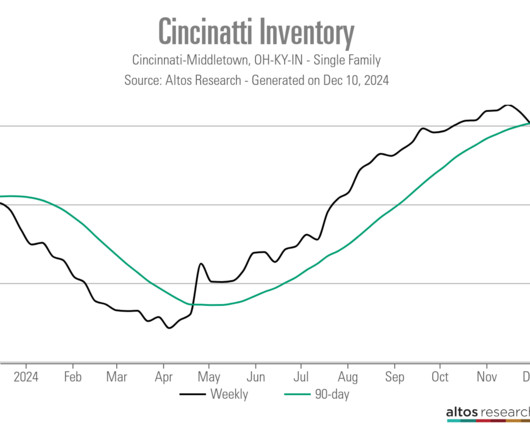

Have we seen the peak in housing inventory for 2024? The best part about 2024 has been that higher mortgage rates have created an inventory buffer, so if the economy gets softer and rates fall, we have many more homes to work with than we had in 2020-2023. Weekly inventory change (Aug.

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025. However, this year, mortgage rates rose during this timeframe.

The mortgage rate lockdown premise holds that very few people will list their homes when mortgage rates are this high, thus suppressing inventory. 2024 has had healthy inventory growth despite mortgage rates above 7%. Each time, inventory has squared right into the model as long as rates stay elevated.

Have lower mortgage rates already started to slow down housing inventory? I have a simple weekly growth model with the Altos inventory data: when rates are high, over 7.25%, inventory should grow between 11,000-17,000 weekly. Still, I would consider the last month of inventory growth healthy.

Department of Housing & Urban Development (HUD) will co-host the “Mortgage Market Resilience and Access to Credit Summit” on Tuesday, October 15 at HUD’s headquarters. Independent mortgage banks play a key role in making this a reality, and this summit will shine a spotlight on their essential contributions to our housing market.”

Active weekly housing inventory growth slowed slightly last week, but it’s still running at a healthier clip than in 2023. I have a simple model with mortgage rates being above 7.25%: weekly inventory data should grow between 11,000-17,000 per week. We have now seen it for two weeks as inventory grew by 13,247.

Communities across the country, particularly those that are popular among retirees, are seeing an influx of older residents as a “silver tsunami” — based on population rather than housing inventory — prepares to wash over them. AARP was also on hand at the event.

These events led to lower mortgage rates and increased purchase application data last week, but decreased housing inventory. Active inventory fell 1,109, and new listing data made a lovely comeback week to week but was still noticeably down year over year. In a regular market, they would be closer to 5.25%.

Total housing inventory growth has been slow in 2023, but with rising mortgage rates over the last few months, inventory has grown a bit faster than average. The question now is: Have we hit the seasonal peak in inventory for 2023? Last year, according to Altos Research , the seasonal peak for housing inventory was Oct.

When I notice a significant increase or decrease compared to estimates, I often suspect that revisions will be made or that a one-time event may have influenced the figures. Mortgage rates have been rising and the housing market is also experiencing the impacts of hurricanes. This represents a supply of 9.5

On Friday NAR reported that total housing inventory levels broke under 1 million in December, dropping to 970,00 units for a population of 330 million people. million in January down to about 4 million in December, We now have total inventory levels near all-time lows again. In one of the most historical years in the U.S.

We know inventory has been climbing all year. The MBAs mortgage applications data has been surprisingly strong. The northern cities have tight inventory and rising prices, some of the Sunbelt cities have the most inventory in many years, and some markets even have falling prices, too. When demand slows, inventory grows.

While weekly inventory is still falling, we have year-over-year growth in total active listing and new listings data. This calls into question a mortgage rate lockdown, as mortgage rates are also higher year over year. However, this data can move stronger in either direction when mortgage rates rise or fall aggressively.

Housing inventory increased by 1,339 homes nationwide. Mortgage rates fell along with bond yields, showing that mortgage rates peaked on Oct. The weekly inventory data, which had fallen faster than I had anticipated the last few weeks, has now seen a slight uptick. Weekly housing inventory.

The solid demographics for home purchasing and historically low mortgage rates — which have been in a downtrend for four decades — have created a housing market where prices are rising too fast. Exclusive access to the HW+ Slack community and virtual events. with the housing market leading the way. Become a member today.

Last week we saw a noticeable slowdown in housing inventory growth that I hope has more to do with a holiday week than a trend. Mortgage rates fell last week after the debt ceiling issues were resolved, but the damage from higher rates took its toll on purchase application data again.

Jessica Lautz, deputy chief economist and vice president of research at the National Association of Realtors and upcoming speaker at the Housing Economic Summit, sat down with HousingWires Senior Director of Events Brena Nath to answer a few questions on what she thinks is to come for real estate in 2025.

HousingWire’s fourth-annual Engage Marketing event will feature experts focused on the specifics of mortgage and real estate in a purchase market. The MBA is estimating record purchase volume for the rest of this year, but climbing mortgage rates and low inventory mean it won’t be easy to capture your share of business.

Housing inventory finally broke under 2022 levels last week. Mortgage rates rose last week after the better-than-anticipated jobless claims data but even with higher rates, we also had a third week of positive purchase application data. In March of 2022 we had the lowest inventory levels ever recorded in history.

During this period, household formation will create the mortgage demand needed to push applications to that level, and purchase applications did get to this level right before COVID-19 hit in February of 2020. Exclusive access to the HW+ Slack community and virtual events. HousingWire Magazine delivered to your home or office.

26 in Dallas, provided valuable insights into the forces shaping the mortgage and housing markets in 2025. With economists, analysts and industry leaders in the room, discussions revolved around key economic indicators, inventory shifts, technology advancements and what lenders should be doing right now to prepare for the next cycle.

The housing market got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. Despite two interest rate cuts by the Federal Reserve, mortgage rates rose again and remain stubbornly high. But on a comparable home, another of her clients had an offer below the asking price accepted.

Among those with mortgages, 47% reported having locked in an interest rate below 4%. Economic uncertainty also plays a role in sellers’ hesitation, with 29% saying they would delay selling in the event of a major downturn. months of inventory at the current sales pace compared to the national median of 2.8

2 million , we could be at risk of housing inventory falling to such low levels that I would have to categorize this housing market as unhealthy. We can see that inventory falling to such low levels has created unhealthy home-price growth in both 2020 and 2021. Inventory fades in the fall and winter and picks up in summer and spring.

Summer is here, and housing inventory is finally growing! The spring housing inventory was like a zombie rising from the grave, very slow, but the summer is showing some promise and let’s hope it continues. Mortgage rates were again in a small range, hanging near 7%. Purchase apps had a small week-to-week gain.

Mortgage rates have made almost a 2% move lower from the highs of 2023. Now that the jobs week data is in, the question is: can mortgage rates go even lower? Mortgage spreads Another way for mortgage rates to drop to the lowest level of the forecast or below is to improve mortgage spreads.

Big picture 2025, our view is that it will be slightly better than 2024 in terms of originations and sales , but unfortunately it probably wont feel much better, McKeveny, the managing director of mortgage and real estate at Zelman & Associates , told attendees of HousingWires Housing Economic Summit on Wednesday.

Mortgage rates headed higher last week after the CPI inflation report , but now, with news of a wider war in the Middle East, should we expect even higher rates? 10-year yield and mortgage rates There is nothing good to report on mortgage rates from last week. The week ahead will answer some of those questions early on.

Tune in for our next event with Mohtashami happening March 23rd at 12 CT in the #articlediscussion channel. HousingWire: Let’s start with a bang Logan, will the inventory crisis end this year? The goal for inventory is to get back to 1.52-1.93 Inventory is about to increase as it always does during this year.

We survived jobs week and Federal Reserve Chairman Jerome Powell talking to Congress, with mortgage rates ending the week below 7%. But will mortgage rates keep heading lower? If so, what will this do to inventory levels? Given our current economic data and without a new critical global event, this range should stick.

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? However, mortgage rates have fallen more than 1% since the recent highs, so it’s time to look at the data to explain how to interpret it.

With Q4 in full swing, many realtors are seeing buyers and sellers paralyzed by high interest rates and stagnant inventories. Whether it’s infrastructure developments, seasonal shifts, or political events like the upcoming election, these micro-shifts create opportunities for educated buyers and sellers.

Mortgage applications decreased for the fourth straight week – this time down 2.2%, according to the latest report from the Mortgage Bankers Association. Record-low inventory is pushing home-price growth at double the rate from a year ago, and even above the 10% growth rates seen in 2005,” Kan said. from the week prior.

Illustration of a mortgage loan officer struggling with rate volatility. Image created with ChatGPT 4o While the trade war initiated last week by the Trump administration has brought volatility to mortgage rates, some loan officers have seen an uptick in home loan applications as some borrowers are staying on course. a week prior.

The holiday season is here, and despite higher mortgage rates last week, housing demand is displaying some festive resilience. Mortgage rates picked up last week, though that hasnt significantly impacted our pending contract data, which is showing some positive year-over-year growth when we compare it to 2022 and 2023.

Lack of inventory is an issue builders and mortgage loan originators alike are dealing with across the nation. It’s also what keeps Andrew Marquis, regional vice president at CrossCountry Mortgage and Scotsman Guide ’s seventh top LO, up at night, especially as he sees more buyers entering the market.

We’ve all been wondering what 5% plus mortgage rates would do to the hot housing market, and now we’ve got that and a bag of chips. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housing market. Inventory is still showing negative year-over-year data.

In addition, this is the fourth straight month of inventory declining, while days on the market are growingl! “The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. Plus, available housing inventory remains near historic lows.”

Mortgage relief is on the horizon for U.S. The report predicts a year-end rise in both for-sale inventory and the median sales price of existing homes, projecting increases of 14.5% and 4.6%, respectively, despite ongoing challenges from elevated mortgage rates. The forecast anticipates a 14.5% decline in home prices to a 4.6%

As we think about coming out of this first month of the year, we’ve quickly realized this year is going to be anything but planned or what we in the mortgage lending industry are used to. But for others, low mortgage rates gave way to pre-approved borrowers struggling in a very competitive seller’s market.

As existing home inventory continues to fall, builder confidence is on the rise, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) report, released Monday. Builders note that additional declines in mortgage rates, to below 6%, will price-in further demand for housing.

After the series wraps in January, join us on February 8 for the HW+ Virtual 2022 Forecast Event. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the predictions for this year, along with a roundtable discussion on how these insights apply to your business.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content