This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Last April, Erik Morin made a return to the reverse mortgage valuation space by joining appraisal and valuation company Atlas VMS. Morin founded Landmark Network in 2007, a company that quickly became a key player on the valuation side of the reverse mortgage space before being acquired by Class Valuation in 2018.

A policy designed for lenders to review and respond to borrower-initiated reconsideration of value (ROV) requests for appraisals — originally scheduled to be implemented between Aug. These include “improvements to the process by which borrowers may request an ROV if they identify a problem with the appraisal,” the original ML said.

By now, most appraisers are aware that Fannie Mae and Freddie Mac (GSEs) have embarked on a complete overhaul of the Uniform Appraisal Dataset (UAD). These codes, or language, make sense to appraisers but confuse uninitiated readers of our reports. It all starts with the standard appraisal forms used in the mortgage process.

Starting March 14, 2022, the Federal Housing Administration (FHA) will require all lenders to use FHA Catalyst for appraisals. The module can also accept appraisals for Home Equity Conversion Mortgages (HECMs), the administration announced last week. How increased regulation presents a huge opportunity for lenders.

The Department of Veterans Affairs will raise appraisal fees and lengthen allowable turnaround times in select markets across the country in response to high demand for appraisals. The VA designated markets as high-demand based on increased demand for appraisal services and a shortage of appraisers.

There has been a lot of talk about the Uniform Appraisal Dataset (UAD) and Uniform Residential Appraisal Report (URAR) redesign initiative, and how it will make life easier for appraisers. The mortgageappraisal forms we use today were designed in 2005 using technology and mortgage processes in place at the time.

Fannie Mae and Freddie Mac are not designing the software for the future, but they have provided the specification for the Uniform Appraisal Data set (UAD) they want to receive. It is up to appraisal software companies to develop solutions to provide this specific data set.

After years of AMCs chipping away at the public trust, the New York AMC law was designed to protect the consumer. Seriously, the value-add provided by AMCs to the appraisal process in the delivery of actual appraisals might be 5%, but no chance in hell it is 75%. This is why we need consumer protection in the mortgage business.

United Wholesale Mortgage (UWM) announced late last year that it would turn the appraisal space on its head by launching an in-house appraisal program. Even if it has not made quite the outsized impact UWM said it would, appraisers mostly like the wholesaler’s new program.

Mass Appraisal tend to exhibit a regressive nature… In the intricate landscape of real estate mortgage financing, the notion of appraisal waivers recently dubbed “Value Acceptance”, by the Government Sponsored Enterprises (GSEs), has stirred considerable debate. million armed robbery of a… Certified Appraisers vs.

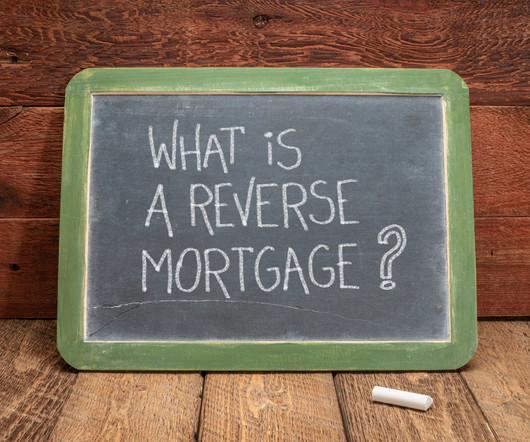

Reverse mortgages are becoming an increasingly popular financial tool for homeowners over the age of 62 who want to access equity in their homes. One important aspect of the reverse mortgage process is the appraisal, which determines the value of the property and plays a crucial role in determining the size of the loan.

There has been a lot of talk about the Uniform Appraisal Dataset (UAD) and Uniform Residential Appraisal Report (URAR) redesign initiative, and how it will make life easier for appraisers. The mortgageappraisal forms we use today were designed in 2005 using technology and mortgage processes in place at the time.

This article first appeared in the June issue of National Mortgage Professional Magazine. . The home appraisal has been requested…the waiting begins. Will the appraiser give credit for all the upgrades in the home? Is the appraiser familiar with the neighborhood? Will the appraised value be sufficient for the loan?”.

This article first appeared in the June issue of National Mortgage Professional Magazine. . The home appraisal has been requested…the waiting begins. Will the appraiser give credit for all the upgrades in the home? Is the appraiser familiar with the neighborhood? Will the appraised value be sufficient for the loan?”.

But with a majority of the mortgageappraisal volume being engaged through appraisal management companies, as an appraiser, working with AMCs is almost a necessity today. Here are ten tips designed to help you improve your appraiser score, get more assignments close to home, and earn more money working with AMCs.

The technology has been drifting into mortgage lending reliance for more than a decade because it has been marketed as having the ease of “pushing a button.” During my career, I have observed that valuation accuracy has become weaker as technology has expanded in the mortgage process. Private Island on New York’s St. million), and 5.27

The uniquely designed roof needs immediate replacement. There is virtually no way to get a mortgage on the property in its present condition, so it takes a cash buyer. CE Course: Learn about the differences between traditional mortgageappraisal assignments and foreclosure assignments in our course, Appraising REO Properties.

In this blog, we will delve into the world of relocation appraisals and explore their importance in the relocation industry. We will also discuss the key differences between relocation appraisals and mortgageappraisals to provide a comprehensive understanding of the appraisal process.

Relocation appraisals are used to get an estimate of what a home will sell for. The appraisal professional who does the appraisal will look at many factors of the home. These include the overall design of it, what comparable sales have been, the current housing market, and the general appeal of the home.

This blog post will explore the importance of relocation appraisal and its purpose and approach. We’ll also discuss how it differs from mortgageappraisal, specifically designed to facilitate mortgage lending. How is a Relocation Appraisal Different from a MortgageAppraisal?

NOTE: Please scroll down to read the other topics in this long blog post on USPAP and Personal Inspection, GSE Appraisal Modernization, Transaction costs and values including real estate commissions, unusual homes, mortgage origination stats, etc. = Mortgage rates were 18%+. Many appraisers are not busy.

Typically, this area comprises homes that are similar in terms of age, quality, design, appeal, price range, school system, and transportation access points, among other factors. Appraisers will use the most recent sales available so it stands to reason that agents should do this as well.

Relocation appraisals play a vital role in the relocation industry by determining a property’s fair market value. These aren’t your everyday mortgageappraisals; they look into many details that matter when companies move their employees around.

NOTE: Please scroll down to read the other topics in this long blog post on hybrid appraisals, business tips, UAD info from Freddie, Fannie modernization, non-lender appraisals, unusual homes, mortgage origination stats, etc. = Built in 2014, the six-bedroom estate was designed to resemble an English manor.

CDEI, MNAA Excerpts: Typically, this time starts when the comparable goes under contract, then ends on the effective date of the appraisal. Remember what it was like during the crash after 2008, when there were very few loans and appraisal volume severely declined? Mortgage lending is very, very cyclical.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content