This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mortgage rates continue to rise, serving as a bucket of cold water for lenders and consumers that were warming to lower borrowing costs just a few months ago. According to HousingWire ‘s Mortgage Rates Center , the average 30-year conforming rate was 6.61% on Tuesday. With mortgage rates back above 6.5%

That’s 12% more sellers than a year ago. It seems more sellers are coming out every week and that will keep inventory pushing upward. Mortgage rates pushed this week close to 7.25%. Its only two weeks into January and mortgage rates have hit the high end of the range we forecasted for the entire year.

New contracts for home purchases are coming in very low this month. Buyer activity has been dropping for several weeks and there are now fewer homes in contract than a year ago. Buyer activity has been dropping for several weeks and there are now fewer homes in contract than a year ago. When will that be? I have no idea.

However, there are two big trends that stand out as we launch into 2025 affordability and sellers in the market. Home prices finished 2024 up a few percent nationally and mortgage rates are at their highest level in seven months back over 7% as we head into January. Theres another set of sellers that we call immediate sales.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

As inventory builds and, as there are fewer offers from homebuyers , more sellers feel the need to reduce the asking price of the homes for sale. Sellers who dont get an offer may choose to cut their price. There are few offers being made right now, so more sellers are finding the need to reduce their asking price. There are 27.7%

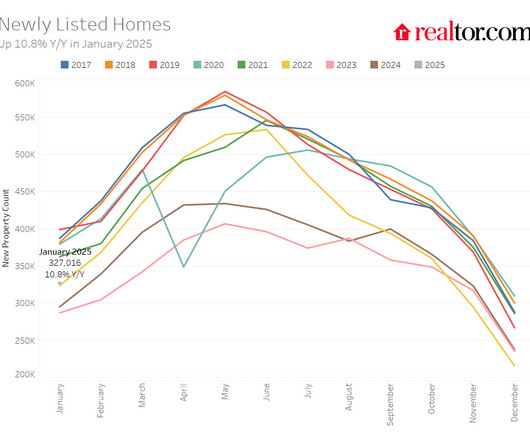

According to the Realtor.com January Monthly Housing Report, January saw a positive shift in seller activity despite recent hikes in mortgage rates, with the number of newly listed homes increasing 37.5% The uptick is likely due to some residual benefit from falls lower mortgage rates, which could fade. month-over-month.

Potential home sellers notice weak demand, fewer offers and price reductions, prompting them to back away from the market. If potential sellers avoid the market, this will keep a lid on supply growth. New listings are hitting the market Last year was an environment with 5% to 10% more sellers each week than a year prior.

There is constant movement in the mortgage industry with the desire for growth and expansion. Thus, it has never been more important to focus on due diligence in analyzing a mortgage industry acquisition target. Regulatory compliance The mortgage industry is heavily regulated and subject to scrutiny by both State and Federal agencies.

Mortgage rates are a big variable here. In 2024, we saw a notable increase in buyer demand when mortgage rates got close to 6%. However, mortgage rates were climbing to their highest level of the year at this time in 2024. Mortgage rates now are lower than they were a year ago. This year its 2%. There are 28.7%

Indiana-based lender Ruoff Mortgage is making a move designed to help more homeowners get into new homes with ease. Ruoff Mortgage is teaming up with fintech company Calque to offer two “buy before you sell“ programs to customers. The Trade-In Mortgage — Calque’s most popular program — functions similar to a vehicle trade-in.

Given the unrelenting mortgage costs, generally weak homebuyer demand, and the year’s rising supply of unsold homes, I’ve been expecting home prices to recede a bit in the second half of this year. Maybe next year, if mortgage rates stay in the high 6s, inventory will build closer to the old normal after five years of a severe shortage.

The Consumer Financial Protection Bureau (CFPB) on Tuesday released an advisory opinion stating that contracts for deed are under federal home lending rules and should provide consumer protections. According to a CFPB, sellers typically target low-income borrowers, particularly in Black, Hispanic, immigrant, and religious communities.

Compared to a month prior, contract signings fell 5.5% An index reading of 100 is equal to the level of contract signings in 2001. After four straight months of gains in contract signings, one step back is not welcome news, but it is not entirely surprising, Lawrence Yun, NARs chief economist, said in a statement. in the West.

increase in the Pending Home Sales Index (PHSI), a measure of future home sales based on contract signings, to 75.8, The amount of contract activity in 2001 is represented by an index of 100. Year-over-year, contract signings grew in the Northeast and West and were unchanged in the Midwest and South. September saw a 7.4%

It’s still April, so there could be as many as eight more weeks of seller growth in the spring housing market. And seller growth is happening pretty much everywhere across the country, with Florida and Texas leading the way. The bearish take is that there are many more sellers than buyers and inventory is rising. orate further?

While inventory of unsold homes in the housing market in each of the last two years headed higher during September and October due to mortgage rate spikes, we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year.

The 30-year fixed mortgage has followed suit, recently falling as low as 6.75%, the lowest level since mid-December. Its quite obvious that stubbornly high mortgage rates slowed down early season homebuyers in the first quarter of 2025. So, mortgage rates have been declining for several weeks now. Thats a pretty notable swing.

Although higher home prices , rising mortgage rates and other expenses are obvious factors, there may be more to the story. The homes that went under contract took 43 days to do so the slowest pace since 2019. “I explain to sellers that their house will sit on the market if its not fairly priced.

This week, we count 14% more homes in the contract pending stage now than a year ago. Last year was weak as mortgage rates were hitting 8%. Mortgage rates were super high and inventory was building. That difference can be attributed to mortgage rates staying higher for longer through September. It’s really just one week.

Mortgage rates continue to move higher and that’s impacting buyers. New listings One way reason it will be hard for inventory to grow more than 17% next year is that there are still not enough sellers to get there. Frankly, it feels like the housing market is contracting a bit now in November. of the homes on the market.

The mortgage professional of the future goes beyond the transaction. Our mortgage industry is experiencing a fundamental shift. Traditional loan officers who focus solely on transactions are being replaced by mortgage professionals who act as financial strategists, long-term advisors, and educators.

In recent weeks, home sales also faltered in the face of 7% mortgage rates. Now some of them are sliding below the year prior, which is driven by relentlessly high mortgage rates. This market is at a standstill as long as mortgage rates are above 7%. Home sellers and listing agents know where demand is for homes.

The defining characteristic of the 2023 housing market has been dramatically fewer home sellers than any recent year. In this week’s Altos Research video, I look at how home sellers and sales are up, but that doesn’t mean prices will climb in 2024. Housing inventory climbed late in the year as mortgage rates rose.

At the same time, mortgage rates jumped back over 7%. What were trying to track are what the real-time signals are telling us about homebuyers and 7% mortgage rates. In those times, we just had far more buyers than sellers. Since were entering the year with mortgage rates over 7%, that may put a damper on purchase demand.

While the industry is no stranger to predatory and/or unfair lending practices, new advisory opinion and research study on a type of home seller financing known as a “contract for deed” has been released by the Consumer Financial Protection Bureau (CFPB). The CFPB is had a field hearing in St.

Sellers can just wait it out, and it looks like the U.S. I think it’s worth examining if sellers will indeed just wait it out now. If mortgage rates jump in late summer, we would see another boost in unsold inventory. That is 13% more sellers than last year at this time, but it’s not expanding any more this summer.

The MBAs mortgage applications data has been surprisingly strong. During that time, mortgage rates continually moved lower. Supply growth could also come from more sellers, such as investors or distressed borrowers unloading. However, in most of the country, we have no growth from the seller side. That’s normal.

According to a recent Redfin study, housing prices and mortgage rates are still high, and home sales are at their weakest pace since the pandemic began. Now its pretty clear that sellers arent slashing asking prices and mortgage rates arent plummeting, so mindsets are shifting. The market had 5.2 Median asking price $407,225 5.2%

There are still notably not a lot of sellers. But home sellers are gradually easing back into this housing market. There were 66,000 new listings this week, of which 14,000 are already in contract. Sellers are coming back to this housing market. 14,000 of those new listings are already in contract.

Price reductions ticked up this week for the first time since November in the face of rising mortgage rates. We can see the impact of higher mortgage rates slowing homebuyer demand. Now, mortgage rates are 100 basis points higher. We still see more sellers than last year. The pace of sales inched down, too.

Economic uncertainty : Concerns about tariffs , layoffs, and federal policy changes are making buyers and sometimes sellers hesitate. High mortgage rates and Home Prices : The average 30-year fixed mortgage rate hit 6.96% in January, an eight-month high. home-sale price rising 4.1% year-over-year. 5.9%), Nassau County, N.Y.

Mortgage rates continue to climb. It’s not uncommon to hear rates quoted over 8% for a 30-year fixed mortgage. 8% mortgage rates are a new reality We’ve been talking about the impact of 8% mortgage rates for months. The path to finally having more selection for homebuyers is through higher mortgage rates.

The number of homes under contract across the country has risen for the last few weeks. Purchase mortgage applications are up for five weeks in a row. It seems like mortgage rates are getting closer to 6% are shaking loose a few transactions. Pending home sales climb There are 362,000 single-family homes under contract.

More buyers have entered the market as the economy continues to add jobs, housing inventory grows compared to a year ago, and consumers get used to a new normal of mortgage rates between 6% and 7%. As of December 12, the 30-year fixed-rate mortgage averaged 6.6%, according to Freddie Mac. At the end of November, there were 1.33

Mortgage butterflies As confident and comfortable as I was in the home search process and the paperwork involved in signing on with an agent, I was not feeling great about the mortgage preapproval and application process. But in another stroke of luck, I have a cousin who is a loan officer at Guild Mortgage.

The index includes sales of properties that went under contract in October, so it doesn’t quite capture what’s currently happening in the housing market. “Mortgage rates nearing 7% in January seem to have affected buyers more than sellers,” Zillow senior economist Kara Ng said. year over year in December.

Home sellers are returning to the market, but buyers are hesitant, according to a recent Zillow market report. Inflation has hit younger households hardest, and stubbornly high rates have pushed a mortgage out of reach for many first-time buyers. The typical mortgage payment is up 11.3% That has cooled competition for houses.

Redfin cited a number of reasons for this increase in the nations housing inventory, including: The mortgage rate lock-in effect is fading: A number of homeowners who scored low mortgage rates during the pandemic have been staying put because moving would mean taking on a higher rate. of homes that went under contract last month.

Lease-purchase arrangements are receiving renewed attention from legislators looking for ways to make homeownership more accessible, and theyre a great way to help buyers who cant qualify for a traditional mortgage or pony up the money needed for a down payment. But that doesnt mean there arent risks involved for potential purchasers.

In 2023, following the collapse of Silicon Valley Bank , the spreads between the 30-year mortgage and 10-year yield were at their worst, leading to new cycle highs. This meant mortgage rates were significantly higher than average. Mortgage spreads Last year, the 10-year yield hit 5% and mortgage rates got above 8%.

Mortgage rates are back over 7%. Even as money is more expensive and there are more sellers than a year ago, we can also see slight home sales growth over 2023. The economy has continued to be strong, so mortgage rates have defied expectations and remained very high. And as demand slows, inventory grows.

Mortgage rates are back up over 7% this morning on the back of strong economic growth data. The 10-year bond yield jumped back over 4% and that pushes mortgage rates higher too. Mortgage rates are 40 basis points higher than a month ago, and 100 basis points higher than a year ago. There are more buyers than sellers.

We saw a big jump in mortgage rates last week. The 30-year fixed rate mortgage, according to the HousingWire Mortgage Rates Center , is now over 7.2% — that’s 50 basis points above where we were at the start of the year. At that time, most of the voices in the media assumed that mortgage rates had peaked and would fall by now.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content