This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

“For our seller-clients, we were counseling them on how the buyers waive appraisals or waive mortgage contingencies,” Cordano said. “With the influx of New York City buyers bidding these houses up, oftentimes waiving the financing/mortgage/appraisal contingencies was not a difficult thing to ask for and most of them did that.”.

By now, most appraisers are aware that Fannie Mae and Freddie Mac (GSEs) have embarked on a complete overhaul of the Uniform Appraisal Dataset (UAD). These codes, or language, make sense to appraisers but confuse uninitiated readers of our reports. No longer will appraisers find the right field and check the right box.

Even though the lender is the client, the borrower is by regulation, required to be given a copy of the appraisal report. When a sale is involved, the valuation may be lower than contracted price. Sometimes there are sales that were showing as under contract as of the effective date of the appraisal that had closed.

When selecting an appraiser, it’s important to choose someone who is licensed and qualified to perform the type of appraisal you need. Many appraisers’ professional experiences are limited to mortgageappraisals. They may not be familiar with reporting requirement for other appraisal purposes.

This can come in the form of a pre-listing appraisal to help establish a market-supported asking price for the seller. The appraisal can also give potential buyers peace of mind that the home is accurately priced and will most likely not have any value issues when the mortgageappraisal is performed.

What is a MortgageAppraisal? A mortgageappraisal is an appraisal that is done for mortgage lending purposes. Lenders, including banks and mortgage companies, require an appraisal to justify the loan they are making. Who is the Appraisal for? This is called equity.

There has been a lot of talk about the Uniform Appraisal Dataset (UAD) and Uniform Residential Appraisal Report (URAR) redesign initiative, and how it will make life easier for appraisers. The mortgageappraisal forms we use today were designed in 2005 using technology and mortgage processes in place at the time.

Kiedrowski The most recent statistics show Value Acceptance accounts for up to 40% of all mortgage approvals. It is presented as part of the GSEs “Appraisal Modernization” initiative, which aims to streamline the mortgageappraisal process. The average contract interest rate for 5/1 ARMs was unchanged at 6.38

. == == Appraisal Business Tips Humor for Appraisers Click here to subscribe to our FREE weekly appraiser email newsletter and get the latest appraisal news!! To read the listing with 44 photos, Click Here = The Illogical Reality of MortgageAppraisal Reviews By Dallas T. Private Island on New York’s St.

Today I’m going to share my top tips for choosing comps from an appraiser’s perspective. If agents can use the same techniques an appraiser uses the likelihood of there being a big discrepancy between the contract price and appraisal is reduced.

Withholding or threatening to withhold timely payment for an appraisal report or appraisal services rendered when the appraisal report or services are provided in accordance with the contract between the parties. A Few Basics. Market value has some key elements that we must understand.

Withholding or threatening to withhold timely payment for an appraisal report or appraisal services rendered when the appraisal report or services are provided in accordance with the contract between the parties. A Few Basics. Market value has some key elements that we must understand.

This article discusses what an appraisal requires, why it needs to be reviewed and the methods involved in arriving at both conclusions. What Is an Appraisal? An appraisal is the fair valuation of a property based on a professional’s opinion, mainly if the payment method includes a mortgage.

However, the couple was “shocked” when they were informed by loanDepot’s loan officer that Lanham, who conducted the appraisal, valued their home for only $472,000. loanDepot contracted 20/20 Valuations and after the appraisal, the lender said it would not extend the loan.

One example is that mortgageappraisal work allows an appraiser to say: “I’m appraising it as repaired,” which is acceptable in some mortgage assignments. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) increased to 6.57

CDEI, MNAA Excerpts: Typically, this time starts when the comparable goes under contract, then ends on the effective date of the appraisal. CDEI, MNAA Excerpts: Typically, this time starts when the comparable goes under contract, then ends on the effective date of the appraisal. times 42-days or $5,523. percent from 6.72

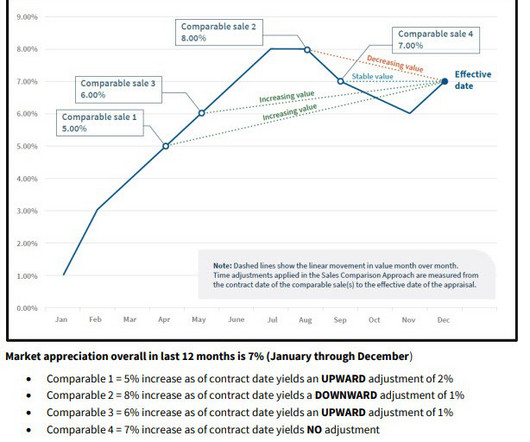

This is shorthand that every experienced appraiser knows and understands please dont @ me Market Condition Adjustments Illustration Fannie Mae guidelines emphasize that adjustments made to comparable sales are based on market changes between the contract date of the comparable sales and the effective date of the appraisal.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) remained unchanged at 6.52 The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $766,550) decreased to 6.73 percent, with points decreasing to 0.64

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content