This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

After completing countless Veterans Administration (VA) mortgage loan transactions over the years, Chris Pascoe, a Marine veteran turned RE/MAX agent, has developed something of a system. First, he has his clients lender call the listing agent. That never happens when a VA loan is involved.

Similarly to the way a reverse mortgage originator is more hands on with their clients than a forward mortgage counterpart, Atlas aims to deliver something similar with its services, Morin said. The most rewarding part of my career has been returning to the space and being welcomed by our former clients,” Morin said.

In the ultra-competitive Westchester market, the odds were stacked against Heather Harrison and her client. “The client went to highest and best on Monday at 5 p.m., and I counseled my client to bid accordingly, waive his mortgage contingency, then we bid $1.45 million and we got it.”

It’s been rejection after rejection for Isabel Williams’ client, a military veteran in Port St. Since the client began the search for her dream home earlier this year, her Veterans Affairs mortgage loan offers have been rejected over a dozen times. Lucie, Florida.

Challenging the results of the appraisal for mortgage financing. The first thing to remember as a consumer or real estate agent, is that the client is the lender, not the consumer. The lender obtains the appraisal to ensure that the collateral is adequate for the loan (remember the three C’s of credit, capacity, and collateral).

Embattled digital lender Better.com also launched a one-day mortgage program in January. Available in 50 states, clients who are salaried W2 employees and make a downpayment of at least 3% on a conforming Fannie Mae or Freddie Mac mortgage are eligible for Better.com’s One Day Mortgage program.

Prior to joining SettlementOne, Michelle served as National Sales and Business Development Manager at Class Valuation, one of the largest appraisal management companies in the country. Together, through commitment and dedication, I know we will help drive tremendous success for our clients. About SettlementOne Valuation .

Paul Charron, a Massachusetts-based appraiser who has done 50 orders through UWM’s program since signing up in October, said that he receives his fee within two to three days after uploading the report. That stands in sharp contrast to his other clients, where 99% of the time Charron said he gets paid within a month.

Fannie Mae and Freddie Mac are not designing the software for the future, but they have provided the specification for the Uniform Appraisal Data set (UAD) they want to receive. It is up to appraisal software companies to develop solutions to provide this specific data set. at the very beginning.

But Sean Pyle, president of appraisal management company Valutrust Solutions , says he’s already dealing with pressure from lenders who are expecting desktop appraisals to reduce their costs, too. “My My counsel to clients I speak with is, ‘Don’t think about this in any other terms than potential time savings,’” Pyle said.

When real estate agents and appraisers work together seamlessly, clients benefit from well-informed decisions, transactions become smoother, and professional relationships are strengthened. A mutually respectful partnership ensures that each of their clients receives informed advice, leading to confident decisions.

Specialized Services: Different situations require different types of appraisals. At Appraisal Hub Inc., we offer specialized services such as commercial appraisals , home and mortgageappraisals , estate settlement appraisals, divorce appraisals , and capital gain appraisals.

What is a MortgageAppraisal? A mortgageappraisal is an appraisal that is done for mortgage lending purposes. Lenders, including banks and mortgage companies, require an appraisal to justify the loan they are making. Who is the Appraisal for? This is called equity.

Fritz Appraisals Inc. we strive to make the process of purchasing or selling a home less stressful for our clients by providing timely and accurate appraisals that can assist with making sound real estate decisions. Fritz Appraisals Inc. Fritz Appraisals Inc.

But with a majority of the mortgageappraisal volume being engaged through appraisal management companies, as an appraiser, working with AMCs is almost a necessity today. Here are ten tips designed to help you improve your appraiser score, get more assignments close to home, and earn more money working with AMCs.

Appraisers can provide detailed property appraisals based on market conditions, comparable sales, and property-specific factors, aiding accountants in preparing reliable financial statements. Accountants often rely on appraisers to assess the potential profitability and risks associated with residential property investments.

Traut notes that the Federal Housing Finance Agency (FHFA) announced in late October 2021 at the Mortgage Banker Association’s annual conference that banks and mortgage lenders will be able to use desktop appraisals in place of traditional appraisals for qualifying Fannie Mae or Freddie Mac backed mortgages.

For this reason, if you are not the client, or employed by the client of the appraisal report, the appraiser will politely decline to discuss the appraisal with you. Before we dive into tips and tricks for disputing an appraisal, let’s level-set with a few foundational concepts and terms. A Few Basics.

For this reason, if you are not the client, or employed by the client of the appraisal report, the appraiser will politely decline to discuss the appraisal with you. Before we dive into tips and tricks for disputing an appraisal, let’s level-set with a few foundational concepts and terms. A Few Basics.

In this blog, we will delve into the world of relocation appraisals and explore their importance in the relocation industry. We will also discuss the key differences between relocation appraisals and mortgageappraisals to provide a comprehensive understanding of the appraisal process.

This article discusses what an appraisal requires, why it needs to be reviewed and the methods involved in arriving at both conclusions. What Is an Appraisal? An appraisal is the fair valuation of a property based on a professional’s opinion, mainly if the payment method includes a mortgage.

Regular Appraisal Reviews. Last but certainly not least, more AMCs could stand to get into the habit of performing reviews on every appraisal report before it is delivered to the client and/or lender. A thorough appraisal report will: determine if the original appraisal has been based on all the relative data.

Regular Appraisal Reviews. Last but certainly not least, more AMCs could stand to get into the habit of performing reviews on every appraisal report before it is delivered to the client and/or lender. A thorough appraisal report will: determine if the original appraisal has been based on all the relative data.

Regular Appraisal Reviews. Last but certainly not least, more AMCs could stand to get into the habit of performing reviews on every appraisal report before it is delivered to the client and/or lender. A thorough appraisal report will: determine if the original appraisal has been based on all the relative data.

My first appraisal job was updating data records for an assessor’s office, converting to computerized valuation in the mid-1970s. Some AMCs may use appraisers for data collection at a reasonable fee instead of Uber drivers with 3 weeks of training. I would love to have all my clients email me the appraisal order.

The AMC/client then performs a detailed review of your appraisal and adjustments. If the appraisal was completed properly and included sufficient information, this problem would go away. Chink in the Armor I just completed a review of an appraisal that had been turned into the state.

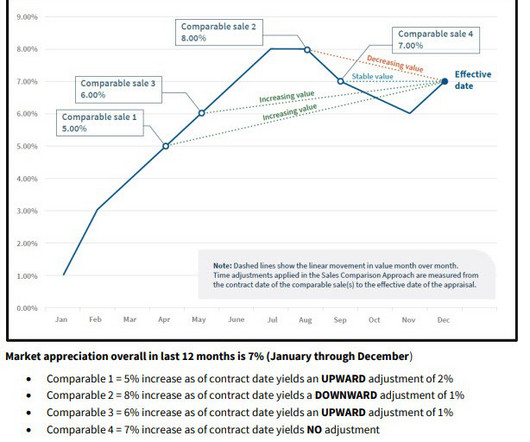

CDEI, MNAA Excerpts: Typically, this time starts when the comparable goes under contract, then ends on the effective date of the appraisal. To fail to reflect them truly and correctly in the final value opinion is to mislead the client. To guess at the time adjustment is to fail to reflect market trends truly and correctly.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content