This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is a continuation of the April 15, 2024 article “ From Forms to Reports: A Look at the UAD Overhaul ” I am named after my father, who passed away in 2000. I had just returned from college, and back then, there was no appraisal software available. That’s how I first got involved in valuation technology.

Once the HVCC, Home Valuation Code of Conduct, is enacted the majority of lender and mortgageappraisal requests will be diverted through Appraisal Management Companies (AMCs). Although this may curb the evils of “lender pressure” on us appraisers, it will also take up to 50% of our fee!!

Traut notes that the Federal Housing Finance Agency (FHFA) announced in late October 2021 at the Mortgage Banker Association’s annual conference that banks and mortgage lenders will be able to use desktop appraisals in place of traditional appraisals for qualifying Fannie Mae or Freddie Mac backed mortgages.

There has been a lot of talk about the Uniform Appraisal Dataset (UAD) and Uniform Residential Appraisal Report (URAR) redesign initiative, and how it will make life easier for appraisers. The mortgageappraisal forms we use today were designed in 2005 using technology and mortgage processes in place at the time.

Once the HVCC, Home Valuation Code of Conduct, is enacted the majority of lender and mortgageappraisal requests will be diverted through Appraisal Management Companies (AMCs). Although this may curb the evils of “lender pressure” on us appraisers, it will also take up to 50% of our fee!!

What is a MortgageAppraisal? A mortgageappraisal is an appraisal that is done for mortgage lending purposes. Lenders, including banks and mortgage companies, require an appraisal to justify the loan they are making. Who is the Appraisal for? Appraisal vs Home Inspection.

The technology has been drifting into mortgage lending reliance for more than a decade because it has been marketed as having the ease of “pushing a button.” The driver behind this final rule was to eliminate potential bias in valuations by replacing appraisers with AVMS. To read more, Click Here My comments: Worth reading.

How To Appraise Rural Properties Excerpts: Appraising residential properties in rural areas can be both challenging and rewarding. Unlike the standardized expectations of urban and suburban properties, rural properties often present unique characteristics that require a nuanced approach to valuation. I hate this time change.

This article first appeared in the June issue of National Mortgage Professional Magazine. . The home appraisal has been requested…the waiting begins. Will the appraiser give credit for all the upgrades in the home? Is the appraiser familiar with the neighborhood? Will repairs be needed? A Few Basics.

This article first appeared in the June issue of National Mortgage Professional Magazine. . The home appraisal has been requested…the waiting begins. Will the appraiser give credit for all the upgrades in the home? Is the appraiser familiar with the neighborhood? Will repairs be needed? A Few Basics.

Still, with appraisal being as much of an art as it is an objective science, it is also true that the same property could receive two very different valuations from different appraisers. Unfortunately, a lack of appraisal quality control is one of many factors that contributed to the real estate crisis of 2008.

Still, with appraisal being as much of an art as it is an objective science, it is also true that the same property could receive two very different valuations from different appraisers. Unfortunately, a lack of appraisal quality control is one of many factors that contributed to the real estate crisis of 2008.

Still, with appraisal being as much of an art as it is an objective science, it is also true that the same property could receive two very different valuations from different appraisers. Unfortunately, a lack of appraisal quality control is one of many factors that contributed to the real estate crisis of 2008.

Home negotiations can be deadlocked because of the valuation differences of a property by both prospects and homeowners. This is why home appraisals are advised to ensure property costing is as fair as possible. This is why home appraisals are advised to ensure property costing is as fair as possible. What Is an Appraisal?

In this day and age where borrowers put speed and efficiency over anything, a slow appraisal process could reflect negatively on the lender and cause strain with the borrower. This article explores how appraisal tech can streamline the appraisal process and ensure repeat customers. Presented by: Reggora.

Some appraisers may want to become data collectors or do desktops. My first appraisal job was updating data records for an assessor’s office, converting to computerized valuation in the mid-1970s. Some AMCs may use appraisers for data collection at a reasonable fee instead of Uber drivers with 3 weeks of training.

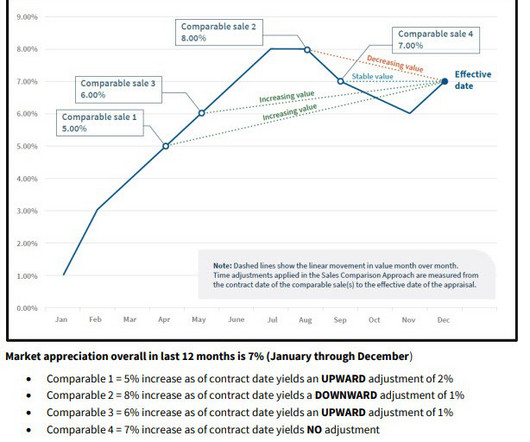

The goal is to make sure every adjustment is defensible, based on empirical evidence, and can withstand scrutiny from all stakeholders involved in the appraisal process. By applying these methods, appraisers can provide reliable, accurate valuations that reflect current market conditions and ensure the appraisals credibility and acceptance.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content