This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Let’s talk about that today as well as dig into insurance. UPCOMING SPEAKING GIGS: 11/7/2024 Think Like an Appraiser (3 hours) TBA 11/19/24 Downtown […] The post Flat prices & the insurance mess first appeared on Sacramento Appraisal Blog. I have some encouragement to share too about mindset.

Its not just home prices that are expensive, as they hover at historically high levels; rising insurance premiums are contributing to the growing costs of homeownership and property management. Home, rental, and property-related insurance products are ubiquitous and foundational to the health of the U.S. housing market.

Property insurance costs for mortgaged single-family homes rose by a record $276 (+14%) to $2,290 in 2024 with average premiums now up 61% over the past five years. of borrowers switched insurance providers in 2024, up from 9.4% of borrowers switched insurance providers in 2024, up from 9.4%

and Anthony Carolei, Director of Risk Management for Professional Liability at Hanover, host Hal Humphreys explores the critical intersection of real estate appraisal and E&O insurance. Catch them at industry events like ACTS, Valuation Expo, or the Appraisal Summit this year. Want to connect with Susan or Anthony?

Property insurance costs for mortgaged single-family homes increased a record $276 or 14% to an average of $2,290 per year in 2024, according to ICE Mortgage Technologys latest Mortgage Monitor report. percent of borrowers switched insurance providers in 2024, up from 9.4 Among the major U.S. Among the major U.S. A record 11.4%

Natural disasters are reshaping the housing marketso what does that mean for appraisers, lenders, and homeowners? In this episode, we dive into the growing risks posed by wildfires, hurricanes, and floods, and how these extreme events are impacting property values and insurability. Will we see mass migration away from high-risk zones?

And yet, about that same amount failed to upgrade their insurance policies to protect their new investment. homeowners, 400 independent insurance agents, and 131 empty nesters, identified as married or partnered U.S. homeowners, 400 independent insurance agents, and 131 empty nesters, identified as married or partnered U.S.

We have amazing data scientists who are building out new models — from reducing premiums on wildfire insurance in California to using image analytics so that an appraiser can capture the appraisal in real time and use it for quality assurance. The insurance commissioner there declared 13 resiliency prerequisites.

It wasn’t on my housing market bingo card to be paying such close attention to insurance, but this is a huge deal for California (and some other states). I promise this won’t become an insurance crisis blog, but today I have some brand new stats to share for Sacramento and the Bay Area.

The home insurance marketplace has been facing a reckoning. With the death toll from Helene crossing the grim milestone of 230 this week — and with thousands of impacted homes without flood insurance wiped away — this could lead to a ripple effect that drives homeowners insurance premiums even higher.

Recent years have seen Oregon struggle with not only severe winter storms but also an increase in insurance premiums. Homeowners in the state have faced a 42% rise in insurance premiums from 2019 to 2024 due to repeated disasters, including fires, floods, and destructive winter storms like Winter Storm Indigo in 2024.

Insurance has been a glaring mess in California, and it’s really starting to affect the housing market. Today, I want to share some things I’m hearing from the real estate community after asking for feedback on my social channels about home and fire insurance.

But that benefit is beginning to be offset by a surge in insurance costs and HOA fees caused by intensifying natural disasters ,along with rising property taxes. This gives buyers leverage when theyre negotiating with other insurers. Buyers are also considering how much theyll have to pay for insurance when writing offers, he said.

A group of 2,769 West Virginian borrowers claimed in the lawsuit, which was originally filed on July 23, 2012, that Rocket Mortgage (known then as Quicken Loans ) and its insurance arm, Amrock (formerly Title Source ), were unfairly influencing home appraisal values. However, a 2021 Supreme Court decision, TransUnion LLC v.

First American Financial Corporation , a provider of title, settlement and risk solutions for real estate transactions, has published a data-driven analysis of the vital role that the title insurance industry plays in protecting the smooth functioning of the real estate economy in the United States.

These areas have seen increases in severe weather exposure and insurance costs, resulting in a steady increase in the overall cost of homeownership. Insurance cost acceleration relative to home appreciation: Insurance costs are rising dramatically faster than mortgage payments. million in 2025. million in 2025.

Matic announced that it has published its annual year-end trends and predictions report, which examines significant developments in the house insurance market and their effects on mortgage lenders and homeowners. In the second half of 2024, premium growth slowed considerably, with average rate increases for new plans being 6.6%

In a recent report, Sarah Frano, vice president and real estate fraud expert at First American Title Insurance Company , explains that scammers are increasingly harnessing AI to generate deepfake videos and fraudulently pose as legitimate borrowers. But AI can be a double-edged sword, as there is also a rising risk of AI-driven fraud.

The post Costs Mounting for Homebuyers appeared first on Appraisal Buzz. home ($501,500) adding $75,255, the upfront cost totals a staggering $107,230. Click here to access Clever Real Estate’s report, “ The True Cost of Buying a Home in 2024.” The post Costs Mounting for Homebuyers first appeared on The MortgagePoint.

Department of Housing & Urban Development (HUD) have released new appraisal data from loan applications on single-family mortgages submitted to HUD’s Federal Housing Administration (FHA). The data previously included only appraisals of properties where the loan would be acquired by Fannie Mae or Freddie Mac (GSEs).

These factors, along with an increase in the population in high-risk areas, have made the market unstable and made it difficult for insurers to make ends meet. The average number of house insurance quotations accessible per person nationwide decreased by 27% between June 2023 and June 2024, partly due to regulatory obstacles.

Mortgage tech startup Staircase says it has launched a tool that enables mortgage insurers to automate the underwriting of non-delegated mortgage insurance (MI) policies for lenders at about half of the typical cost. In the delegated channel, the lender underwrites the loan for mortgage insurance and submits it to the mortgage insurer.

A policy designed for lenders to review and respond to borrower-initiated reconsideration of value (ROV) requests for appraisals — originally scheduled to be implemented between Aug. These include “improvements to the process by which borrowers may request an ROV if they identify a problem with the appraisal,” the original ML said.

The title insurance industry mitigates more than $600 billion in estimated risk exposure annually for home buyers, according to a report from First American. The curative work conducted by the U.S.

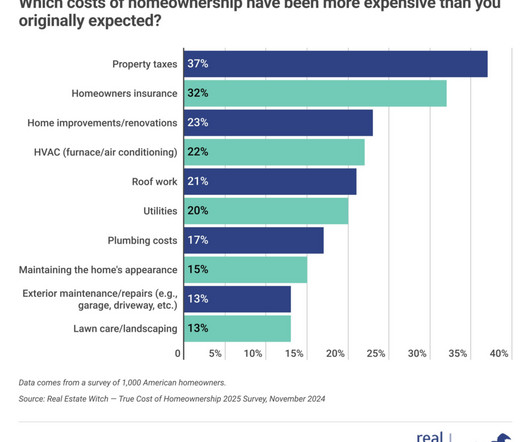

The findings suggest that rising costs of property taxes, insurance, utilities, and home maintenancerather than just mortgage paymentsare driving increased financial pressure, even for those who secured historically low mortgage rates in recent years.

Life insurance companies will see $64 billion (9%) of their outstanding mortgage balances mature in 2025. appeared first on Appraisal Buzz. Just $31 billion (3%) of the outstanding balance of multifamily and health care mortgages held or guaranteed by Fannie Mae, Freddie Mac, FHA and Ginnie Mae will mature in 2025.

Cooper Group mrcoopergroup.com/ Servicing Coppell, TX Mortgage Machine Services, Inc. Cooper Group mrcoopergroup.com/ Servicing Coppell, TX Mortgage Machine Services, Inc. Cooper Group mrcoopergroup.com/ Servicing Coppell, TX Mortgage Machine Services, Inc. Cooper Group mrcoopergroup.com/ Servicing Coppell, TX Mortgage Machine Services, Inc.

According to a survey of 783 title insurance entities nationwide conducted by ALTA and NDP Analytics, 28% of title insurance companies reported at least one SIF attempt in 2023, and 19% reported an attempt during the month of April 2024 alone. Fortunately, most SIF cases are identified and addressed before closing.

The Federal Financial Institutions Examination Council (FFIEC) on Monday issued a statement outlining examination principles related to valuation and appraisal discrimination or bias in residential lending. FFIEC is a federal interagency coalition consisting of the Federal Reserve Board of Governors (FRB), the Federal Deposit Insurance Corp.

appeared first on Appraisal Buzz. A high-level look at the 10 most expensive and least expensive cities among the 50 largest U.S. cities are outlined below. The post Where Are the Nation’s Most Expensive and Most Affordable Cities? first appeared on The MortgagePoint. The post Where Are the Nation’s Most Expensive and Most Affordable Cities?

These include mortgage/rent, auto loan, utilities, cable/internet, cell phone, alarm/security, and three types of insurance (auto, life, and the consumer-paid part of health insurance). appeared first on Appraisal Buzz. Not surprisingly, Hawaii holds the top spot as the most expensive state in the union.

The Federal Housing Administration on Thursday said it would pause the mandatory effective date for its electronic appraisal delivery module because it is “reassessing aspects of [its] development and implementation.”. FHA will provide further updates on its plans for electronic appraisal delivery as they become available.”.

A proper home appraisal is essential whether purchasing or selling a property. This appraisal is used by mortgage lenders to calculate the maximum amount they will lend on a property. Many even watch the worth of their own homes, which are produced by these algorithmic appraisal techniques, on well-known real estate websites.

Luke Tomaszewski, an appraiser doing home inspections in the aftermath of the housing bust, was traveling as much as an hour across Chicago just to snap exterior photos of bank-owned properties. At $50 to $100 per inspection, according to ProxyPics, it’s certainly less expensive than sending an appraiser. Made to order.

Congress hopes to supplant the appraisal governing body at the center of the industry’s self-regulated framework and make public the trove of appraisal data held by the government-sponsored enterprises. The registry would also track whether an appraiser had completed the minimum required fair housing training.

While some homeowners prioritize their mortgage payments, those who are not financially prepared may face significant challenges due to other essential and frequent expenses such as homeowners insurance, property taxes, utilities, repairs, and maintenance.

His senior executive management positions include nine years as president and COO of the nation’s largest title insurance company, Chairman and Co-CEO of a software company, and CEO of a real estate data and information company. The post The Week Ahead: Preparing for 2025 appeared first on Appraisal Buzz.

The importance of home appraisals to the homebuying and selling processes necessitate a stronger eye toward the use of burgeoning AI across a wide swath of U.S. The bureau expressed concern that the use of such tech could impact the equitable application of home appraisals. businesses.

With climate risks, the reason people move is not necessarily solely related to physical safety, but also because of the potential financial impact of high insurance premiums and other home protection measures.” The post More House Hunters Factoring in Climate Risks appeared first on Appraisal Buzz.

Business delinquency rates for five of the biggest investor groupscommercial banks and thrifts, commercial mortgage-backed securities (CMBS), life insurance companies, and Fannie Mae and Freddie Macare examined in MBAs quarterly analysis. The post Q3 Commercial Mortgage Delinquency Rates Ramp Up appeared first on Appraisal Buzz.

There are several factors to cite but I want to highlight a key area that may be taken for granted — that not everyone receives a fair home appraisal. Stifled The Fair Housing Center of Metropolitan Detroit shared that loan denial rates in Detroit, due to the appraised value of a home (a.k.a. I hope you will join me.

Most appraisers are experiencing a significant slowdown in mortgage lending work due to rapidly increasing mortgage rates which are slowing down the housing market. Mortgage lending work is only one type of business where appraisals are needed. Mortgage lending work is only one type of business where appraisals are needed.

FinRegLab analyzed this situation in a new report to see how automating and updating federal insurance programs to make them home only might ease some of the strain of the affordable housing crisis. Increasing access to affordable home-only loans is an important strategy for addressing the housing crisis, said FinRegLab CEO Melissa Koide.

What’s the difference between a home inspection and an appraisal? Before you get overwhelmed, take comfort that critical milestones of home inspection, appraisal and closing processes are all great ways to get more acquainted with your prospective new home. An appraisal is a valuation of a property by a third party.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content