This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Appraisal management software company Reggora announced this week the launch of its Appraisal Marketplace, which leverages data managed by the company in an effort to improve appraisal performance. By leveraging Reggora’s own data, its marketplace is aiming to improve the performance of the appraisal industry, the company said.

But in another stroke of luck, I have a cousin who is a loanofficer at Guild Mortgage. In writing both offers, Angela and I made sure to fully disclose how I was expecting her to get paid , as well as all of my requests, including a home inspection contingency clause.

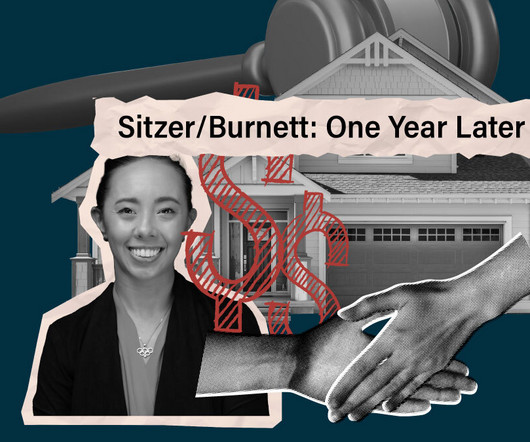

However, a year after the GSEs announced new appraisal modernization solutions, as they’re more widely adopted, questions arise. And as a loanofficer (LO), why should I care? A look into GSE appraisal modernization efforts The GSEs have each offered appraisal waivers on eligible loans for several years.

Appraisers have been accused of being “speed bumps” in the lending process. We frustrate buyers, sellers, loanofficers and, sometimes, real estate agents. In some ways, I can understand their. Read More.

Editor in Chief Sarah Wheeler sat down with Scot Rose , CIO at Class Valuation , to talk about innovation in the appraisal space and how the technology being deployed for appraisal modernization can actually protect appraisers. Everybody is affected by the appraisal process. SW: How is technology changing appraisals?

Loanofficers and listing agents are familiar with homeowner anxiety about real estate appraisals. Questions arise, such as: Does the appraiser penalize me if my house isn’t spotless? Will the appraiser look in my closets? Should I follow the appraiser and point things out? Will worn carpeting hurt my value?

Local real estate agents, loanofficers and appraisers share what characteristics are currently defining their housing markets. Buyers “are waiving inspections, an appraisal contingency, and the latest trend is to pay closing costs usually done by the seller.” Kansas City, Missouri.

Rapidly accelerating home prices come with a variety of challenges for lenders and real estate agents, including one of the biggest pain points right now — the appraisal gap. If they get a higher offer that has financing, then when appraisal comes back, the buyer is going to renegotiate the sales price to be closer to appraised value.”.

The Ernst Fee Service is used by lenders to minimize fee cures by providing recording fees, transfer taxes, property tax, title, settlement, inspection data, and lender and appraisal fees. .

Tips To Ensure a Successful Appraisal When it comes to the home appraisal process, providing complete and accurate information is critical for a successful appraisal. Real estate agents and loanofficers play an important role in ensuring appraisers have the necessary data to deliver reliable valuations.

The industry is buzzing with conversations around appraisal modernization — for good reason. Appraisal modernization reduces origination cycle time, bolsters appraiser capacity and helps lenders deliver a more seamless and transparent borrower experience.

Welcome to the very first post in our all-new series The LoanOfficer’s Guide to Appraisals. Well – not really the end, but one of the last parts of some appraisals – namely the final inspection. We’ll briefly look at what a final inspection […].

It’s the price you pay the loanofficer or broker for completing the loan, and it includes underwriting, originating, and processing the costs of buying a home. The origination fee is a small percentage of the total loan. Home inspection : This is critical for home buyers. Pest inspections : Roaches are one thing.

Because Fairway gets most of its reverse mortgage business from referral partnerships, extending to the purchase market made sense for Fairway because of the partnerships that its loanofficer corps has spent so much time developing, according to Hultquist. Harlan Accola. Real estate agents hate dealing with call centers,” he says.

Loanofficers and listing agents are familiar with homeowner anxiety about real estate appraisals. Questions arise, such as: Does the appraiser penalize me if my house isn’t spotless? Will the appraiser look in my closets? Should I follow the appraiser and point things out? Will worn carpeting hurt my value?

Enact’s David Foster recently spoke with MortgageOrb about how the COVID-19 pandemic impacted inspections and appraisals, the changes we see today, and other appraisal factors to consider. Q: How have inspections and appraisals been impacted since the beginning of the COVID-19 pandemic?

For the past six months, I’ve been blogging with the purpose of assisting loanofficers to better understand the appraisal process. So far, we’ve covered final inspections, lending on unique homes, communication with the appraiser, reconsiderations of value, bracketing and FHA appraisals.

Welcome to the September edition of our blog series, The LoanOfficer’s Guide to Appraisals. This entire year, I’ve been blogging once a month with the purpose of assisting loanofficers to better understand the appraisal process. This month’s blog post will be all about new construction appraisals.

At each stage of the buying process, there are multiple siloed transactions, from appraisals, inspections and settlements to mortgage payments and homeowners’ insurance. No Need to Reinvent the Wheel – Put Your Customer First.

Right now on our Appraisal Blog, we’re all about helping LoanOfficers. This post is part six of a 12-part series we’re calling The LoanOfficer’s Guide to Appraisals. The post The LoanOfficer’s Guide to Appraisals Part 6: How are FHA Appraisals Different From Others?

What New Homebuyers Need To Know About Appraisals. In this new homebuyer’s guide to appraisals, I’ll help you understand the process during your first home purchase. I would like to do my part by informing and educating you on the appraisal part of the transaction. What is a Mortgage Appraisal?

By foregoing contingencies such as home inspections and appraisals altogether, mortgage lenders risk violating their fiduciary duty – which is supposed to prioritize the interests of the borrower above all else. appeared on Appraisers Blogs. After all, who doesn’t want to close more deals in less time?

This post is part three of a 12-part series we recently launched called The LoanOfficer’s Guide to Appraisals. In case you missed part one on the Final Inspection process, go back and read it here. And last time, we discussed all kinds of unique homes, and gave tips on how to make lending on […].

By foregoing contingencies such as home inspections and appraisals altogether, mortgage lenders risk violating their fiduciary duty – which is… The post HUD’s Use of Convicted Felons to Ramp Up ‘Discrimination Testing’ appeared on Appraisers Blogs. But What About Fiduciary Duty?

The mortgage process involves diligence and timeliness to ensure that borrowers can meet their closing date – that diligence is also required to master the appraisal review process. Ensuring you know the ins and outs of the appraisal review is imperative to help your borrowers meet that end goal on time.

Right now on our Appraisal Blog, we’re all about helping LoanOfficers. This post is part five of a 12-part series we’re calling The LoanOfficer’s Guide to Appraisals. The post The LoanOfficer’s Guide to Appraisals Part 5: What is bracketing and why do we do it?

Prospective borrowers, especially first-time homebuyers, need to be ready for what they’ll encounter during the homebuying process, including home appraisals. This is true for appraisals, too. Recent trends are surfacing, and more instances of hybrid appraisals are changing how appraisals are conducted.

Time management challenges are a big issue for many property appraisers. Your income depends on how many appraisal assignments you can complete each month and each year—and you need time to produce each report. Last month we asked appraisers, “What’s one thing you wish you could STOP doing to save time in your workday?”

All Appraisals Are Not The Same All appraisals are the same, right? Not really, and today I’m going to explain the differences between several different types of appraisals that could mean the difference between a home appraising for contract price or not.

Remember when loanofficers avoided underwriting loans for manufactured housing for fear of low commissions, foreclosure risks, and the added complexities of underwriting those types of “unreliable” homes? For some, these myths still flood our thoughts when a potential borrower approaches us about a loan for a manufactured home.

But these government-backed loans also aim to help veterans buy homes that are safe, structurally sound and sanitary. Every VA purchase loan requires an appraisal, which includes the valuation of the property along with a high-level check of the home’s condition. What if the home I love doesn’t meet these standards?

So how do you find best Orange County Home Appraiser? You might be a home owner, a mortgage loanofficer or even an appraisal management company. If you Google Orange County Home Appraiser and look at some of the listings, you’ll not find a lot of appraisers in Orange County, CA that do non-lender work.

Another important first-time home buyer step is seeking pre-approval from a lender for a home loan. This is when you will meet a loanofficer from various mortgage companies. Step 6: Get a home inspection. Step 7: Get a home appraisal. Step 3: Get pre-approved for a mortgage.

But these government-backed loans also aim to help veterans buy homes that are safe, structurally sound and sanitary. Every VA purchase loan requires an appraisal, which includes the valuation of the property along with a high-level check of the home’s condition. What if the home I love doesn’t meet these standards?

For example, time matters when an independent appraisal review is required on a correspondent loan, and speed of service is essential to a great experience for homeowners making a home equity finance decision. Residential Broker Price Opinion (BPO) is the ultimate alternative to an appraisal for servicing, origination, and investments.

Certified Appraisers vs. Unlicensed Data Collectors By Jonathan Miller (13-minute video) Here’s a great take on the difference between Certified Appraisers vs. Unlicensed Data Collectors by Leigh Brown, President of the NC Association of REALTORS. Fannie Mae has been working hard to get rid of appraisers for years.

A full pre-approval is when a mortgage loanofficer pulls your credit, verifies your employment and income, has your complete application and has all the required documents from you. Your loanofficer may even put your file through an initial underwriting. Then comes the issue of the appraisal.

Your agent should also be able to tell you if you need to hire anyone else, such as an attorney or an inspection service, depending on your state and situation. Step 5: Get an Appraisal on Your Ideal Property. During the appraisal, a licensed appraiser will take inventory of major systems (i.e.,

What is a Reverse Mortgage Appraisal? A reverse mortgage appraisal is an evaluation of a property’s value to determine how much money can be borrowed through a reverse mortgage. The appraisal is important because it helps lenders assess the risk associated with the reverse mortgage loan.

They ask you at the inspection “So, how much do you need this to come in at?” An appraiser’s data, reasoning and final opinion should be credible, reliable, independent, impartial and objective. If you ever experience this from a loanofficer, feel free to report this behavior to the CFPB here. No, that’s fraud.

Remember when loanofficers avoided underwriting loans for manufactured housing for fear of low commissions, foreclosure risks, and the added complexities of underwriting those types of “unreliable” homes? For some, these myths still flood our thoughts when a potential borrower approaches us about a loan for a manufactured home.

Before you buy a home or refinance a mortgage, your property will most likely need to go through the appraisal process. During an appraisal, a professional will evaluate your home’s condition, how much similar homes have sold for recently and the overall market to determine the value of your home. Home Inspection.

Encompass enables loanofficers to close loans faster, originate more loans, reduce time to close, and create improved borrower experiences. We test ClearAVM against closed sale and refinance appraisal benchmarks. Access comprehensive appraisal review and analysis for any time period.

Home Inspection The home inspection helps identify any potential property issues. Many mortgage companies mandate a home inspection before approving a loan. The inspection report, shared with both buyer and seller, can lead to further negotiations, particularly if repairs or updates are necessary.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content