This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A piece of legislation introduced in the Senate in mid-May could streamline the appraisalprocess for VA loans. The legislation would modernize the Department of Veteran Affairs ‘ appraisal requirements by allowing desktop appraisals, and in some circumstances, waving appraisals all together.

On a quarterly basis since 2014, the FHFA and the CFPB have sent surveys to borrowers who recently obtained mortgage financing. The purpose is to gather feedback on a series of ideas about the market, including consumer experiences of the mortgageprocess, future expectations and perceptions of the wider market.

Reforming the appraisal review process is essential to maintaining the integrity of the real estate market and protecting consumers and homeowners. In mortgage financing, the appraisalprocess is often seen as the foundation of accurate property valuation and market stability.

In a department memo, the VA explained that the move was a response to “high demand for appraisal services and limited availability of appraisers in certain local market areas.”. In order to have the alternative appraisal options, lenders must be approved to participate in the VA’s Lender AppraisalProcessing Program.

By now, most appraisers are aware that Fannie Mae and Freddie Mac (GSEs) have embarked on a complete overhaul of the Uniform Appraisal Dataset (UAD). These codes, or language, make sense to appraisers but confuse uninitiated readers of our reports. Most appraisers have diversity in their business channels.

After completing countless Veterans Administration (VA) mortgage loan transactions over the years, Chris Pascoe, a Marine veteran turned RE/MAX agent, has developed something of a system. Even under “normal” market conditions, VA buyers struggle to successfully purchase a home using their benefit.

Fannie Mae and Freddie Mac are not designing the software for the future, but they have provided the specification for the Uniform Appraisal Data set (UAD) they want to receive. It is up to appraisal software companies to develop solutions to provide this specific data set.

Loni Pincocki, a Michigan-based appraiser, said that if UWM continues to partner with the software company she won’t be using UWM’s appraisal program. I’m already nickel-and-dimed to death as an appraiser,” she said. Zitin noted that while this may be an operational investment for some lenders, there are advantages.

Desktop appraisals arrived in March of 2020, allowing the housing market to keep humming while many stayed indoors to prevent the spread of COVID-19. Allowing appraisals without a walk-through was one of several flexibilities the Federal Housing Finance Agency allowed in light of the pandemic.

What is a Reverse MortgageAppraisal? A reverse mortgageappraisal is an evaluation of a property’s value to determine how much money can be borrowed through a reverse mortgage. The appraisal is important because it helps lenders assess the risk associated with the reverse mortgage loan.

It is presented as part of the GSEs “Appraisal Modernization” initiative, which aims to streamline the mortgageappraisalprocess. However, a closer examination reveals potential drawbacks, raising questions about its efficacy and impact on the housing market. million armed robbery of a… Certified Appraisers vs.

The bill summary was: Relates to the registration of real estate appraisal management companies or an individual or business entity that provides appraisal management services to creditors or to secondary mortgagemarket participants including affiliates by the department of state.

There are many areas that appraisers and agents can inform and educate one another so that each of their jobs is done more successfully. Understanding the Roles: Agents and Appraisers: Real estate agents bring their expertise in marketing and negotiations, while appraisers provide impartial and accurate property valuations.

What is a MortgageAppraisal? A mortgageappraisal is an appraisal that is done for mortgage lending purposes. Lenders, including banks and mortgage companies, require an appraisal to justify the loan they are making. Who is the Appraisal for? Appraisal vs Home Inspection.

One important aspect of the reverse mortgageprocess is the appraisal, which determines the value of the property and plays a crucial role in determining the size of the loan. Understanding reverse mortgages can be complex, but it essentially involves converting a portion of the home’s equity into usable cash.

In the dynamic world of real estate, the role of a real estate appraiser is paramount. Whether you’re buying, selling, or refinancing a property, a precise and professional appraisal is essential to ensure fair market value. Appraisal Hub Inc., At Appraisal Hub Inc., At Appraisal Hub Inc., Appraisal Hub Inc.

Are you considering a reverse mortgage but unsure of what role appraisal plays? In this post, we will cover everything you need to know about reverse mortgageappraisal. We will start by discussing the basics of reverse mortgages and who can benefit from them. Why an Appraisal is Crucial for a Reverse Mortgage?

By providing precise and impartial evaluations, residential appraisals in Toronto also safeguard the interests of all parties involved. Keep reading to find out more about its significance and understand the appraisalprocess. How Do Banks And Other Lenders Use Appraisals? Where Can I Find An Appraiser In Toronto?

Appraisers recently contacted by McKissock tend to agree that the profession will go generally well in 2022, with no major changes to the real estate market and no events on the horizon that could seriously upset appraisers’ business. Desktop appraisals, with information provided by third-party hirelings, may increase.

There has been a lot of talk about the Uniform Appraisal Dataset (UAD) and Uniform Residential Appraisal Report (URAR) redesign initiative, and how it will make life easier for appraisers. The mortgageappraisal forms we use today were designed in 2005 using technology and mortgageprocesses in place at the time.

But with a majority of the mortgageappraisal volume being engaged through appraisal management companies, as an appraiser, working with AMCs is almost a necessity today. Here are ten tips designed to help you improve your appraiser score, get more assignments close to home, and earn more money working with AMCs.

Appraisals play a significant role in determining the fair market value of a property and ensuring a successful relocation. In this blog, we will delve into the world of relocation appraisals and explore their importance in the relocation industry. Why Are They Crucial for Successful Relocation?

Relocation appraisal is the process of evaluating a property’s value in the real estate market. It plays a crucial role in today’s real estate market, especially for employees and employers involved in workforce mobility. It considers supply, demand, market trends, and sales price forecasts.

11 Helpful Tips For Choosing Comps Whenever I speak to agents about the real estate market and the appraisalprocess the one topic that the discussion always leads to is about choosing comps. If you choose the wrong comps the home can stay on the market for an extended period of time. However, this is not always the case.

Relocation appraisals play a vital role in the relocation industry by determining a property’s fair market value. These aren’t your everyday mortgageappraisals; they look into many details that matter when companies move their employees around. That’s where relocation appraisals come in.

Defining rural properties – USDA and GSEs Challenges of appraising rural properties Appraising rural properties presents unique challenges due to their diverse characteristics and market dynamics. We’ve found five glorious examples of glass houses on the market right now.

The technology has been drifting into mortgage lending reliance for more than a decade because it has been marketed as having the ease of “pushing a button.” To read the listing with 44 photos, Click Here = The Illogical Reality of MortgageAppraisal Reviews By Dallas T. Private Island on New York’s St. million), and 5.27

The seller wants to max out the estimate based on the growing inflation and number of renovations made, while the buyer wants the best deal in the market even as home affordability worsens. This is why home appraisals are advised to ensure property costing is as fair as possible. Income Capitalization Approach.

That’s why HousingWire invited Rachel Robinson, director, collateral policy and product development at Rocket Mortgage , to HW Annual to discuss how technology can play an important role in the appraisalprocess and help eliminate discriminatory practices. .

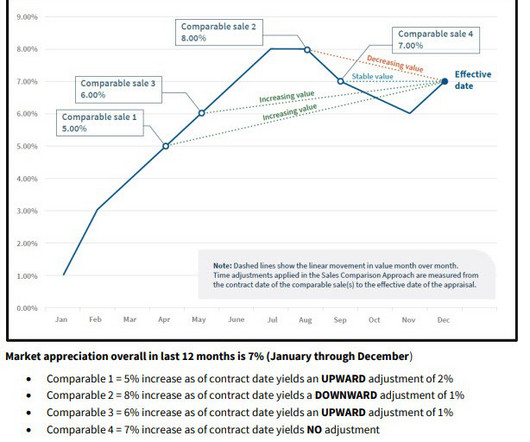

These methods provide a solid foundation for demonstrating how changing market conditions affect property values over time. Below is a detailed explanation of each technique to ensure the adjustments are well-supported and align with market trends. SEE GRAPH BELOW. FANNIE DOES NOT REQUIRE THiS TYPE OF GRAPH.

CDEI, MNAA Excerpts: Typically, this time starts when the comparable goes under contract, then ends on the effective date of the appraisal. CDEI, MNAA Excerpts: Typically, this time starts when the comparable goes under contract, then ends on the effective date of the appraisal. This analysis reveals yet another dilemma.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content