This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Below is a detailed explanation of each technique to ensure the adjustments are well-supported and align with market trends. The goal is to make sure every adjustment is defensible, based on empirical evidence, and can withstand scrutiny from all stakeholders involved in the appraisalprocess.

Having worked with many different lending institutions completing new construction and planned renovation assignments, think of this article as a “best practices” reference to be shared with new lenders, credit analyst team members and borrowers navigating the commercial appraisalprocess for the first time.

The appraiser will determine which of the values is most appropriate and reflective of demonstrating the marketvalue of the property being appraised. Once this happens, the appraiser will explain which approach to value was given the most weight, or consideration, and why. Have a great weekend!

The power itself is referred to as the eminent domain power. Related Posts: Eminent Domain Attorney Review How Does an Eminent Domain Attorney Critique and Review An Appraisal Upon Which His Client’s Just Compensation Is Based? Appraisers always had the power to end the appraisal management pyramid scheme. Attorneys….

Introduction Appraising historical properties involves a complex interplay of factors, making it a specialized field within real estate valuation. Leveraging Market Data The appraisalprocess begins with a thorough analysis of market data, focusing on sales of properties that share historical or antique characteristics.

As such, our experts at The Robert Weiler Company have put together this business valuation ‘questions and answers’ overview to offer more clarity behind the business appraisalprocess. They are: (1) the asset-based approach; (2) the earning value approach; and (3) the marketvalue approach.

Understanding Confidentiality in Real Estate Appraisal The confidentiality of an appraisal report is a cornerstone of professional appraisal practice. According to the USPAP, appraisers are required to uphold confidentiality to protect the interests of their clients and maintain the integrity of the appraisalprocess.

As a land buyer, owner, or seller, understanding the true marketvalue of the real estate in question is important. But first, it’s important to understand what is a land appraisal, how it is appraised, the real estate appraisalprocess, and what to expect. How is Land Appraised?

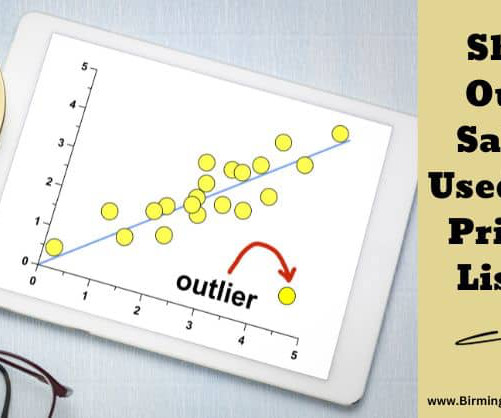

The market area that the property is located in can definatley support the price but does the price truely reflect the marketvalue of that specific property or does it reflect what a super motivated buyer with available funds is willing to pay? There is a difference. If you liked this post subscribe by email (or RSS feed ).

At its core, real estate appraising involves the due diligence necessary to form a credible opinion of the marketvalue of a particular property.This requires a deep understanding of the appraisers local real estate market, as well as of the physical, legal, and economic factors that influence property values in it.

A retrospective appraisal is an appraisal that is performed on a property with an effective date that has occurred before the actual date of the inspection. This type of appraisal is often used for estate and tax purposes, as it can help establish the marketvalue of a property at a prior point in time.

Evaluate the appraiser’s experience. Ask them for their resume and a list of two or three references. The resume may be on the appraiser’s website. The references should be current or previous clients, and at least one should be from the community. Follow up with the references for your selected candidate.

The process can be daunting, especially if you’ve never engaged in an appraisal for commercial real estate before. To simplify and demystify the commercial appraisalprocess for you, we have addressed 17 of the most important questions asked. Question 6: What is the overall commercial real estate appraisalprocess?

All Advisory Opinions, Frequently Asked Questions and the recently launched Reference Manual will now be part of a standalone publication called the 2024 USPAP Guidance and Reference Manual. You can also purchase a linked digital version of the eUSPAP and Guidance and Reference Manual and get seamless access across both documents.

Whether you’re selling your home to begin a new adventure or refinancing your existing home, getting an appraisal with the value you want is an important hurdle to clear. You may feel that the appraisalprocess is out of your control, but there are many easy and inexpensive ways to get both yourself and your home ready.

Like any other investment, you want to know its value with some reliable degree of accuracy. A home appraisal is an unbiased opinion of a home or property’s value. Real estate professionals or other appraisal experts can help you determine the marketvalue of your home. What Is the Home AppraisalProcess?

Tailored to help borrowers of all kinds, in order to gain an FHA loan, your desired property needs to go through an appraisal. In this way, FHA can determine the selected properties’ marketvalue, thus finding out whether the house is worth financing or not. Here we discuss all of that in detail: What is an FHA Appraisal?

Tailored to help borrowers of all kinds, in order to gain an FHA loan, your desired property needs to go through an appraisal. In this way, FHA can determine the selected properties’ marketvalue, thus finding out whether the house is worth financing or not. Here we discuss all of that in detail: What is an FHA Appraisal?

The world of real estate is full of a plethora of professional activities including appraisals. An appraisalrefers to an in-depth and precise evaluation of the current marketvalue of your property. Initially, buyers, sellers and lenders would request expert appraisers to manually appraise their property.

The world of real estate is full of a plethora of professional activities including appraisals. An appraisalrefers to an in-depth and precise evaluation of the current marketvalue of your property. Initially, buyers, sellers and lenders would request expert appraisers to manually appraise their property.

Understanding the role of a home appraiser, the importance of a home appraisal, and the factors to consider when choosing an appraiser are key to making an informed decision. So, let’s dive in and discover how to find the best local home appraiser. Why is a Home Appraisal Important?

After the introductory period ends, the rate adjusts based on the market rate on a set schedule. The first number refers to the length of the introductory period, while the second is how often the rate can adjust. Amortization is the process of paying off a loan over a set period. Fair MarketValue. Amortization.

These appraisals provide an unbiased estimation of a property’s value, taking into account various factors such as location, condition, size, and recent sales of similar properties in the area. This report serves as a reference for buyers, sellers, lenders, and investors to make informed decisions regarding the property.

Tailored to help borrowers of all kinds, in order to gain an FHA loan, your desired property needs to go through an appraisal. In this way, FHA can determine the selected properties’ marketvalue, thus finding out whether the house is worth financing or not. Here we discuss all of that in detail: What is an FHA Appraisal?

The world of real estate is full of a plethora of professional activities including appraisals. An appraisalrefers to an in-depth and precise evaluation of the current marketvalue of your property. Initially, buyers, sellers and lenders would request expert appraisers to manually appraise their property.

The report cited from CSS, analyzed appraisal data across 10 states in the East Coast and Midwest, finding that only around 40% of home sales included an appraisal that was within $2,500 of the final sale price. The appraisal report is shared with the lender, who is the client in this scenario.

Regardless, this process sees an objective third-party make an assessment of the fair marketvalue of the home based on its current status and other conditions, all to make sure that everyone is on the same page about what is about to happen.

Click here Appraising Over 3,000 Years Ago Book of Moses – Donation to a Priest Excerpt: There is a biblical reference in the Bible to appraising in the five books of Moses, written about 1400-1500 BC. Therefore, a neutral appraiser was needed to estimate its marketvalue, so as to determine the price and penalty.

Therefore, the appraisalprocess becomes a key way to prevent that from happening. The key part of the process is that an objective third-party comes in, assesses the value of a property and gives their input. They prevent buyers from significantly overpaying – something that they nor their lender want.

Therefore, the appraisalprocess becomes a key way to prevent that from happening. The key part of the process is that an objective third-party comes in, assesses the value of a property and gives their input. They prevent buyers from significantly overpaying – something that they nor their lender want.

With the plethora of data available today, could an appraiser living hundreds or even thousands of miles away gain sufficient knowledge of local market conditions, trends, and regulations to produce accurate and reliable appraisals? And could it actually be a benefit to not live in the immediate geographic area?

This book is very useful for all residential appraisers, especially those who work for lenders, with many references to Fannie guidelines, USPAP, etc. The new book explores all aspects of homeownership, value, and economics and details all the appraisalprocess steps. The book is still relevant in 2024.

One of the most nerve wracking parts of a real estate transaction can be the appraisalprocess for both buyers and sellers. What is an appraisal? Why is an appraisal necessary? What if the home doesn’t appraise for the contract value? How much does it cost?

Read on to find out why appraisals are important, who pays for them and how much you are likely to pay in British Columbia. What is an Appraisal, and Who Pays for it? A home appraisal is a legal document that determines fair marketvalue for a property.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content