This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A piece of legislation introduced in the Senate in mid-May could streamline the appraisalprocess for VA loans. The legislation would modernize the Department of Veteran Affairs ‘ appraisal requirements by allowing desktop appraisals, and in some circumstances, waving appraisals all together.

“The data released today will provide insights into consumer behavior and borrowers’ experiences, leading to better analysis of how mortgageprocesses could be improved for future borrowers.”

At the end of the day, Pascoe says the process is not all that different than purchasing a home with a conventional mortgage. Even under “normal” market conditions, VA buyers struggle to successfully purchase a home using their benefit.

Desktop appraisals arrived in March of 2020, allowing the housingmarket to keep humming while many stayed indoors to prevent the spread of COVID-19. Allowing appraisals without a walk-through was one of several flexibilities the Federal Housing Finance Agency allowed in light of the pandemic.

Fannie Mae and Freddie Mac are not designing the software for the future, but they have provided the specification for the Uniform Appraisal Data set (UAD) they want to receive. It is up to appraisal software companies to develop solutions to provide this specific data set.

By now, most appraisers are aware that Fannie Mae and Freddie Mac (GSEs) have embarked on a complete overhaul of the Uniform Appraisal Dataset (UAD). These codes, or language, make sense to appraisers but confuse uninitiated readers of our reports. Most appraisers have diversity in their business channels.

It is presented as part of the GSEs “Appraisal Modernization” initiative, which aims to streamline the mortgageappraisalprocess. However, a closer examination reveals potential drawbacks, raising questions about its efficacy and impact on the housingmarket.

The 2022 real estate appraisal term of the year will be “standardization”—of data specifications and measurement standards. Desktop appraisals, with information provided by third-party hirelings, may increase. Housingmarket trends for 2022. Related reading: Check out our roundup of HousingMarket Predictions for 2022.

In this blog, we will delve into the world of relocation appraisals and explore their importance in the relocation industry. We will also discuss the key differences between relocation appraisals and mortgageappraisals to provide a comprehensive understanding of the appraisalprocess.

It plays a crucial role in today’s real estate market, especially for employees and employers involved in workforce mobility. This blog post will explore the importance of relocation appraisal and its purpose and approach. How is a Relocation Appraisal Different from a MortgageAppraisal?

It is presented as part of the GSEs “Appraisal Modernization” initiative, which aims to streamline the mortgageappraisalprocess. However, a closer examination reveals potential drawbacks, raising questions about its efficacy and impact on the housingmarket.

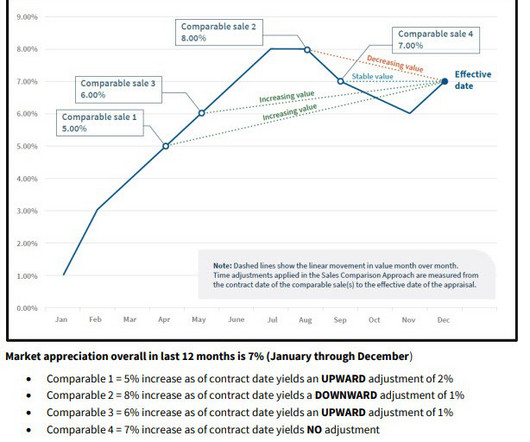

Below is a detailed explanation of each technique to ensure the adjustments are well-supported and align with market trends. The goal is to make sure every adjustment is defensible, based on empirical evidence, and can withstand scrutiny from all stakeholders involved in the appraisalprocess.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content