This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For the past six months, I’ve been blogging with the purpose of assisting loan officers to better understand the appraisalprocess. So far, we’ve covered final inspections, lending on unique homes, communication with the appraiser, reconsiderations of value, bracketing and FHA appraisals.

Right now on our AppraisalBlog, we’re all about helping Loan Officers. This post is part five of a 12-part series we’re calling The Loan Officer’s Guide to Appraisals. So far in our series, we’ve looked at final inspections, lending on unique homes, communication with the appraiser, and reconsiderations of value.

The goal is to make sure every adjustment is defensible, based on empirical evidence, and can withstand scrutiny from all stakeholders involved in the appraisalprocess. Released on the first Tuesday of each month, it features a press release, a full report, and a blog post from the economists.

Following a hosted group lunch, our Certified Real Estate Appraisers will walk the class through the sales grid portion of an appraisal report based on the earlier inspection highlighting insightful topics, including; Adjustment discussions. Bracketing requirements and consideration. Lot, view, and location considerations.

How Agents Can Use The Law of Diminishing Return When Pricing a Listing As a real estate appraiser with over 30 years of experience, I have witnessed firsthand the critical role that accurate pricing plays in the success of real estate transactions. Related posts: What is bracketing and why should Realtors do it?

Right now on our AppraisalBlog, we’re all about helping Loan Officers. This post is part six of a 12-part series we’re calling The Loan Officer’s Guide to Appraisals. The post The Loan Officer’s Guide to Appraisals Part 6: How are FHA Appraisals Different From Others? We’re halfway there!

Price like a Real Estate Appraiser! Are you a real estate professional or mortgage lender looking to learn more about the home appraisalprocess? Let our experienced certified Virginia appraisal experts be the premier source of home appraisal knowledge for your market. Bracketing requirements and consideration.

11 Helpful Tips For Choosing Comps Whenever I speak to agents about the real estate market and the appraisalprocess the one topic that the discussion always leads to is about choosing comps. Using sales that are inferior, similar, and superior to the subject in some aspect constitutes bracketing.

AppraisalProcess To answer this it’s important to understand the appraisalprocess. When we appraise a house, we’re figuring out how much it’s worth. appeared first on Birmingham AppraisalBlog. What is bracketing and why should Realtors do it?

Benefits of Sharing the CMA with the Appraiser During the appraisalprocess, the appraiser will conduct their own market research to locate the most recent and similar comparables to the property they are appraising. I discussed this process in a previous blog post which you can read HERE.

AppraisalProcess To answer this it’s important to understand the appraisalprocess. When we appraise a house, we’re figuring out how much it’s worth. The post Can New Construction Sales be Used in an Appraisal of an Older Home? appeared first on Birmingham AppraisalBlog.

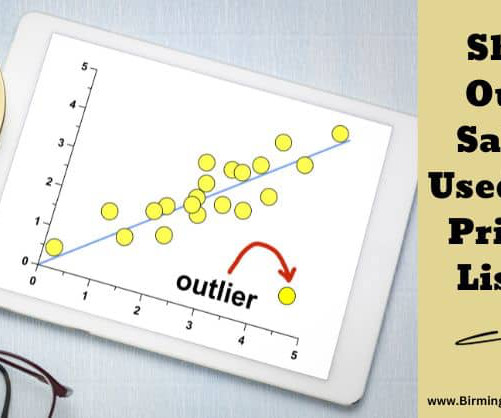

On the other hand, the value that is reflected in most appraisals is a value that reflects what the majority of other market participants are willing to pay. In this blog post, I’ll dive deep into what outlier sales are, why they should not be used in pricing other properties, and the potential consequences of relying on them.

Luckily, we have seven fool-proof ways to reduce revision requests for appraisal orders. In this blog, we will explain the impact of appraisal revisions, methods to prevent common errors, and tips for ultimately reducing the occurrence of appraisal corrections. What are the impacts of appraisal revision requests?

If agents utilize the same methods appraisers use in their appraisals there should not be a vast difference between the two values and the likelihood of a deal falling through will be minimized. I’ve listed below the top search criteria I look at when searching for comps during the appraisalprocess.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content