This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Persistent economic trends that include inflation, a strong labor market and real gross domestic product (GDP) growth will continue to “dampen” mortgage origination activity through at least the end of 2026, according to the newest U.S. mortgage originations outlook from financial services forecasting and advisory company iEmergent.

According to Yun, in 2025 and 2026, the median price of an existing home will increase to $410,700 and $420,000, respectively. In 2025, the yearly 30-year fixed mortgage rate will drop to 5.9%, but in 2026, it will rise to 6.1%. million in 2025 and more than 5 million in 2026,” Yun said.

David Aach , the company’s chief operating officer, sat down with HousingWire s Sarah Wolak to talk about Blue Sage’s goals for full implementation by 2026 and the hurdles the platform has overcome as a newcomer to the servicing industry. This interview has been edited for length and clarity.

According to Fannie Maes Economic and Strategic Research (ESR) Group , mortgage rates are now expected to end 2025 and 2026 at 6.3% in 2026, modest downward revisions owing to weaker incoming data and greater clarity on trade policy. and 6.2%, respectively, downward revisions of three-tenths for each. in 2025 and 2.1%

NAR also updated its 2026 projections. It previously predicted home-price growth of 2% in 2025 and 2026, but it has revised these upward to 3% and 4%, respectively. These are downward revisions from the forecast they released in late 2024, which predicted existing-home sales in 2025 to hit 4.9

for 2026, as measured by the Fannie Mae Home Price Index (FNM-HPI). According to the Q4 2024 Fannie Mae Home Price Expectations Survey (HPES) , following an average expectation for national home price growth of 5.2% in 2024, a panel of more than 100 housing experts forecasts home price growth to decelerate to 3.8% in 2025 and 3.6%

The deal is projected to boost Rockets adjusted earnings per share by late 2026. .” Rocket expects the merger to generate over $200 million in run-rate synergies by 2027, including $140 million in cost savings from streamlining operations and $60 million in revenue gains by connecting financing clients with Redfin agents.

The largest financial institutions — banks holding at least $250 billion in total assets and nondepository institutions generating at least $10 billion in 2023 or 2024 — must comply with the rules by April 1, 2026. Meanwhile, smaller institutions — providers that hold more than $850 million and less than $1.5

The MBA still forecasts 2026 to end at $2.37 As for mortgage rates , the MBA still predicts that 2025 and 2026 will end at 6.5% Its updated forecast, released Feb. 19, put this year’s total origination volume at a projected $2.055 trillion, up slightly from January’s $2.052 trillion forecast. trillion in volume.

The rule goes into effect on March 1, 2026, according to the CFPB. The rule applies existing protections for residential mortgages to borrowers who seek PACE loans to upgrade or renovate their homes through clean energy technology.

Economists predict further slowing in 2025 and 2026 as elevated mortgage rates and four years of rapid appreciation curb demand. Slowing Price Growth Ahead Despite the rising expenses, home sales continued at a steady pace through 2024, sustaining moderate home price growth.

Looking ahead, MBA anticipates continued momentum in 2026, projecting $709 billion in total commercial real estate lending, with $419 billion dedicated to multifamily loans. Multifamily lending, which is included in the total figures, is also expected to rise by 16%, reaching $361 billion in 2025 compared to $312 billion the previous year.

The ESR Group predicts that the broader economy will remain stable and expand at an above-trend pace through 2026 as it navigates elevated core inflationary pressures and heightened policy uncertainty. As part of their newest outlook, Fannie Maes economists shared five predictions for the housing market in 2025.

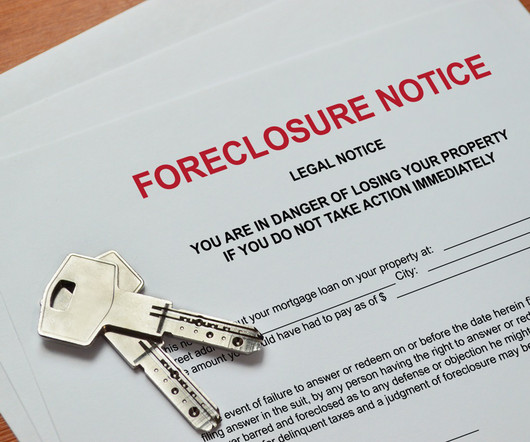

Some emerging risks in the economy and housing market are pushing delinquencies higher, but those higher delinquencies will not likely translate into higher foreclosure auction volume until at least early 2026, Daren Blomquist , the companys vice president of market economics, said in the report.

But I disagree and in the last decade, I made another controversial call, saying the homeownership rate can get back to 66.21% at some point between 2022-2026. How we grew homeownership Before this decade, some pundits said that expecting ownership to stay at 62.2% was too bullish and that the homeownership rates were destined to go lower.

The transaction is expected to be accretive to Rocket Companies adjusted earnings per share by the end of 2026. Rocket Companies will maintain its strong balance sheet and conservative leverage profile upon close of the transaction. The post Rocket to Acquire Mr. Cooper in $9.4B Transaction first appeared on The MortgagePoint.

The transaction is expected to be accretive to Rocket Companies adjusted earnings per share by the end of 2026. Rocket Companies will maintain its strong balance sheet and conservative leverage profile upon close of the transaction. The post Rocket to Purchase Redfin for $1.75B first appeared on The MortgagePoint.

He said he was aware that lawmakers were studying the issue to potentially place on the ballot in 2026, which would likely mean a revision to the states constitution. DeSantis equated the concept of property taxes to renting from the government just to live in your own property.

The requirement would go into place in 2026, and it would ensure NAR leaders and staff “understand” how to properly handle and process sexual harassment complaints, among other things. The Board approved the rule 858 to 47.

Mandatory implementation will occur on November 2, 2026. I look forward to November 2, 2026, when all these changes are behind us. Open the menu and select Module 10. These changes, effective in the new report, will commence limited production in September 2025. Heres a link to the timeline. The transition will be challenging.

The Federal Housing Finance Agency (FHFA) has released a draft of its strategic plan for 2022-2026 and is requesting input on the plan from the general public. The post FHFA Releases Strategic Plan for 2022-2026 appeared first on Appraisal Buzz. The post FHFA Releases Strategic Plan for 2022-2026 appeared first on Appraisal Buzz.

Due to this, McKeveny and the folks at Zelman are expecting meaningful growth in home sales and origination volumes in 2026. That may not make sense, but it is the bounce off the bottom effect and it can be significant. There’s really no shortage of demand, Hale said.

We’re raising the fiscal year 2025 and 2026 estimated revenue growth to 22% and 18% (from 17% and 16%), baking in an increase in FICO’s mortgage score price to $5 in 2025 and $6.50 in 2026, alongside additional pricing actions in auto and card,” the analysts wrote in the report.

Fannie Mae’s Expanded Housing Choice , which the company launched in April 2022 and has extended through April 2026, was established to expand housing opportunities for HCV holders by incentivizing multifamily borrowers to accept vouchers as a valid source of income. Currently in the U.S.,

The largest institutions will have to comply by April 1, 2026, while the smallest covered institutions will have until April 1, 2030. Compliance with the rule will be implemented in phases, with larger providers subject to the rule sooner than smaller ones. Financial firms will be required to comply based on their size.

If a big recession hits in 2025, it would typically take nine to 12 months for that to create inventory, so that would be 2026 before wed see a surge of homes for sale from a recession. By the end of next year we should be basically back to the old normal levels of inventory.

It cannot be revisited until the 2026 session at the earliest. In Hawaii , a bill seeking to establish what would effectively be a state-based clone of the federal HECM program was introduced in the Legislature before being submitted to multiple committees for further deliberation.

For Universal Studios employees, the owners of the park are seeking to construct a 1,000-unit mixed-use development slated to open in 2026 that would promise a short commute to the Universal Orlando Resort, which is also aiming to open a full-scale third theme park called “Epic Universe” next year. “To

trillion in 2026. in 2026, according to Fratantoni’s forecast. Fratantoni expects a major rebound for the mortgage market over the next two years. His forecast calls for $2 trillion in origination volume in 2025 and $2.28 Mortgage rates should fall to 5.9% in 2025 and 5.7%

JBREC is not forecasting meaningful rent growth until 2026 and beyond, which will make it harder for new project developments to pencil.” We believe rates (including financing rates) staying higher for longer will delay any rebound in construction activity in the near term,” he wrote.

The broader economy is expected to remain on solid footing and expand at an above-trend pace through 2026 as it navigates elevated core inflationary pressures and heightened policy uncertainty, the ESR Group writes in its report. Because mortgage rates are unlikely to drop below 6%, those homeowners with mortgages in the 2.5%-5%

To reach a key financial goal in 2026, Blend Labs plans to diversify far beyond mortgage. Achieving positive free cash flow by 2026 would represent a financial landmark for Blend. ”We are guiding to a free cash flow margin of 8% for our conservative case, 18% for the market norm, with our base case at 12%.

It is unclear as to how Wood’s decision will impact the future of the two Batton suits, which were slated to head to trial in late 2026 or early 2027. A hearing for the Batton I suit that was scheduled for Thursday has been cancelled.

Kevin Brown, who will lead NAR in 2026, says he’s seen “the transformative power of homeownership” to move people out of poverty. That’s why I do this.”

I think that mortgage rates will persist to stay high through at least 2026, and while we think that it’s going to slightly affect sales and refinancing, I think developers have incorporated those higher rates in their models. We still see a more modest advance for new single-family home construction.

Per the settlement, Fathom will pay $500,000 into a settlement fund within five days of the settlement gaining final approval from the court and an additionally $500,000 on or before October 1, 2025. Fathom will then pay a final installment of $1.950 million on or before Oct.

2025 Foreclosure Outlook Some emerging risks in the economy and housing market are pushing delinquencies higher, but those higher delinquencies will not likely translate into higher foreclosure auction volume until at least early 2026, added Daren Blomquist, Auction.com VP of Market Economics.

For 2026, Fed officials projected rates to fall below 3% by the end of 2026 through three more quarter percentage point reductions. Instead, fresh economic projections from central bank officials showed rates would be slashed to a median 4.6% by the end of 2024, suggesting three 25 basis points (bps) cuts from current levels.

Additionally, it entitles members to $20 off their 2026 renewal and 20% off all events the fledgling trade group hosts through the end of next year. The association is offering two membership tiers: a basic membership and a founding membership. Basic membership costs $20 for the remainder of 2024 and all of 2025.

Given all of this, cybersecurity experts acknowledge that it is easy for housing industry professionals to feel overwhelmed by the threats posed by fraudsters and their newly honed AI capabilities, but they believe it is not all doom and gloom.

Compass’s market share stands at roughly 5% and the company is targeting 30% market share in its top 30 MSAs by the end of 2026. Compass has also been acquisitive , which could drive accelerated share gains, the KBW analysts wrote.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content