This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, there are two big trends that stand out as we launch into 2025 affordability and sellers in the market. Home prices finished 2024 up a few percent nationally and mortgage rates are at their highest level in seven months back over 7% as we head into January. In 2025, housing affordability in the U.S.

Another jobs week has come to an end, and amid the chaotic headlines about job numbers, tariffs , and the leadership of the Treasury , mortgage rates remained calm. Better mortgage spreads are limiting how high rates can rise in 2025. Today, I want to explain why this topic is essential as we look ahead to the rest of 2025.

Home prices in 2025 are a couple percentage points above where they were last year at this time. Mortgage rates are a big variable here. In 2024, we saw a notable increase in buyer demand when mortgage rates got close to 6%. However, mortgage rates were climbing to their highest level of the year at this time in 2024.

Mortgage applications increased 11.2% on a seasonally adjusted basis from last week, according to data from the Mortgage Bankers Associations (MBA) weekly mortgage applications survey for the week ending March 7, 2025. The refinance share of mortgage activity increased to 45.6% of total applications from 43.8%

What will the housing market look like in 2025? For a more comprehensive look, read our 2025 Housing Market Forecast covering home prices, home sales volumes and more. Mortgage rates continue to move higher and that’s impacting buyers. Frankly, it feels like the housing market is contracting a bit now in November.

March figures to be a crucial month for gauging consumer interest in the 2025 housing market. The pace of home sales remains near a 30-year low point as home prices and mortgage rates keep potential borrowers in wait-and-see mode. But mortgage rates have posted an unusually large decline in the past week.

Mortgage applications increased 20.4% from one week earlier on a seasonally adjusted basis as buyers pounced on lower rates , according to data from the Mortgage Bankers Associations (MBA) weekly mortgage applications survey for the week ending Feb. ” The refinance share of mortgage activity increased to 43.8%

Mortgage rates are declining, and recent purchase application data shows a promising 9% week-to-week increase and a 2% rise compared to the previous year. I’ve noticed that housing data tends to improve when mortgage rates drop from 6.64% to 6%, especially when I adjust for seasonal demand.

As we look into 2025, the question everyone is asking is: Do we have a new era starting? The MBAs mortgage applications data has been surprisingly strong. During that time, mortgage rates continually moved lower. We expect that growth to continue in 2025. Two and a half years. We know sales are inching up, too.

In recent weeks, home sales also faltered in the face of 7% mortgage rates. Now some of them are sliding below the year prior, which is driven by relentlessly high mortgage rates. Lets take a look at the data for the third week of January 2025. This market is at a standstill as long as mortgage rates are above 7%.

If this happens, will we see lower mortgage rates this spring? However, last week saw a decline in mortgage rates due to softer economic data, which led to an influx of money into the bond market as stocks sold off on Friday. We need to be more mindful of the labor data as we go further into 2025.

The difference is mortgage rates: even with inventory growing at a healthy clip this year, mortgage rates just heading down toward 6% for a brief period of time resulted in higher prices in a seasonally soft period. This is something to think about for 2025. However, that didn’t happen. million in October.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

New contracts for home purchases are coming in very low this month. Buyer activity has been dropping for several weeks and there are now fewer homes in contract than a year ago. Buyer activity has been dropping for several weeks and there are now fewer homes in contract than a year ago. When will that be? I have no idea.

Mortgage applications increased 5.4% 6, stemming from a 27% jump in refinance activity, according to a report released Wednesday by the Mortgage Bankers Association (MBA). This is the latest weekly increase in mortgage applications, following a trend of steady demand increases over the past several weeks. share a week prior.

increase in the Pending Home Sales Index (PHSI), a measure of future home sales based on contract signings, to 75.8, The amount of contract activity in 2001 is represented by an index of 100. Year-over-year, contract signings grew in the Northeast and West and were unchanged in the Midwest and South. September saw a 7.4%

With an adjustment for the New Year’s holiday, mortgage applications increased 33.3% from one week earlier, according to the Mortgage Bankers Association s (MBA) weekly mortgage applications survey, released today. The share of refinance mortgage activity increased to 42.7% Bond yields in the U.S. from 16.2%

Compared to a month prior, contract signings fell 5.5% An index reading of 100 is equal to the level of contract signings in 2001. After four straight months of gains in contract signings, one step back is not welcome news, but it is not entirely surprising, Lawrence Yun, NARs chief economist, said in a statement. in the West.

As low inventory levels, elevated mortgage rates and rising home prices keep the housing industry stagnant, short-term real estate investors — aka fix-and-flippers — faced market turmoil during the third quarter of 2024. An index score above 50 indicates market expansion, while a score below 50 indicates contraction. ”

Although higher home prices , rising mortgage rates and other expenses are obvious factors, there may be more to the story. More inventory should be a sign of the market’s return to normalcy, according to Mohtashami, as the market enters 2025 with 27% more inventory compared to early 2024. ” According to the report, 54.5%

Despite rising mortgage rates through much of 2024, recent indications show growing boldness among homebuyers heading into the new year. NAR’s Pending Homes Sales Index (PHSI) report is a forward-looking source that predicts home sales based on contract signings. These increases are persisting despite mortgage rates near 7%.

This is the trend that will be the theme for 2025. Mortgage rates pushed this week close to 7.25%. Its only two weeks into January and mortgage rates have hit the high end of the range we forecasted for the entire year. Bond markets have driven mortgage rates back to the highs, and home sales are suffering. That means 4.2

The 30-year fixed mortgage has followed suit, recently falling as low as 6.75%, the lowest level since mid-December. Its quite obvious that stubbornly high mortgage rates slowed down early season homebuyers in the first quarter of 2025. So, mortgage rates have been declining for several weeks now.

At the same time, mortgage rates jumped back over 7%. What were trying to track are what the real-time signals are telling us about homebuyers and 7% mortgage rates. Thats not true now, so we should expect inventory to begin building for the year in February 2025. In 2018, mortgage rates and inventory rose all year.

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. Despite this, we had positive data on existing home sales , purchase applications, and our weekly pending contract figures.

Mortgage applications increased 2.2% on a seasonally adjusted basis from last week, according to data from the Mortgage Bankers Association s (MBA) weekly mortgage applications survey for the week ending January 31, 2025. The refinance share of mortgage activity increased to 39.0% the previous week.

More buyers have entered the market as the economy continues to add jobs, housing inventory grows compared to a year ago, and consumers get used to a new normal of mortgage rates between 6% and 7%. As of December 12, the 30-year fixed-rate mortgage averaged 6.6%, according to Freddie Mac. At the end of November, there were 1.33

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.0% on a seasonally adjusted basis from one week earlier, according to data from the Mortgage Bankers Associations (MBA) latest weekly mortgage applications survey. 24, 2025, include an adjustment for the Martin Luther King holiday.

Lets take a look at the data for the final week of January 2025. That trend is likely to continue until mortgage prices come back down. Home prices contract The median price for home sales contracts entered this week was at $389,700. This might reverse the trend and push home prices higher in 2025. A shrinking U.S.

Given the unrelenting mortgage costs, generally weak homebuyer demand, and the year’s rising supply of unsold homes, I’ve been expecting home prices to recede a bit in the second half of this year. With just a few local market exceptions, home prices nationally will finish the year up again and will go into 2025 with some upward momentum.

After hitting a two-year high in September 2024, mortgage refinance activity is once again slowing as interest rates remain elevated. While refinancing demand surged briefly when rates dipped, it quickly contracted again following another rate spike in October 2024. in October 2024, the average 30-year fixed mortgage rate fell to 6.1%

Redfin cited a number of reasons for this increase in the nations housing inventory, including: The mortgage rate lock-in effect is fading: A number of homeowners who scored low mortgage rates during the pandemic have been staying put because moving would mean taking on a higher rate. of homes that went under contract last month.

This week, we count 14% more homes in the contract pending stage now than a year ago. Last year was weak as mortgage rates were hitting 8%. Mortgage rates were super high and inventory was building. That difference can be attributed to mortgage rates staying higher for longer through September.

Mortgage applications decreased by 1.2% from last week on a seasonally adjusted basis, according to data from the Mortgage Bankers Associations (MBA) weekly mortgage applications survey for the week ending Feb. The refinance share of mortgage activity increased to 38.9% of total applications from 38.7% the previous week.

Are there any signs of sales growing for 2025? See the purple line for 2025 keeps coming in just below 2024. Last year at this time, mortgage rates were heading higher to peak in May at 7.5%. This year, if current trends hold, we could already be past that point in 2025. in 2025 over the previous year.

Homebuyer demand dipped at the end of the year as mortgage rates continued to climb. After inching downward at the beginning of the month, mortgage rates reversed course halfway through December and have been rising sincein part because the Federal Reserve projected fewer 2025 interest-rate cuts than anticipated. a year earlier.

Union Home Mortgage (UHM) is suing nine former employees on claims they breached several agreements, including non-compete agreements. National Mortgage News , which first reported the lawsuit, noted that APM is not listed as a defendant in the complaint.

Denver-based brokerage franchise Motto Mortgage , owned by RE/MAX , has accused broker shop UMortgage of “tortious interference” in its contract with a former franchisee called TRB Solutions, whose controlling member was Breon Price, the top-producing loan officer. According to a lawsuit filed in March in a U.S

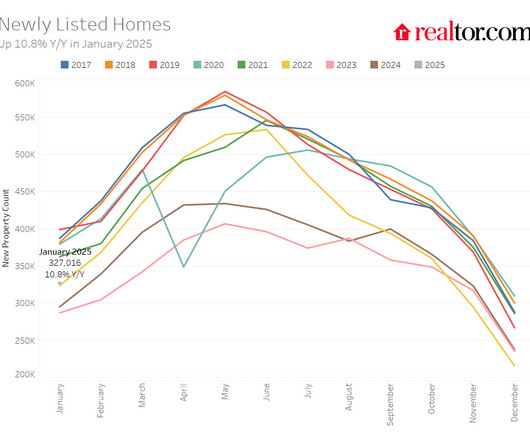

According to the Realtor.com January Monthly Housing Report, January saw a positive shift in seller activity despite recent hikes in mortgage rates, with the number of newly listed homes increasing 37.5% The uptick is likely due to some residual benefit from falls lower mortgage rates, which could fade. month-over-month. 10.7% -0.7%

This indicates slow market stabilization and continued inventory growth throughout 2025. Every year, we have fewer people “locked in” with ultra-cheap mortgage rates , meaning that sellers are slowly returning to the market. If you are assuming that inventory will surge in 2025, this trend may prompt you to think twice.

Mortgage rates continue to move lower this week even as higher borrowing costs have kept activity subdued across many areas of the housing market. Lower mortgage rates are having a positive impact on application levels, with the Mortgage Bankers Association (MBA) reporting last week that applications were up 3.9%

The index includes sales of properties that went under contract in October, so it doesn’t quite capture what’s currently happening in the housing market. “It is expected that we will see slower price growth in early 2025 as inventory increases and affordability continues to be a constraint.”

According to a recent Redfin study, housing prices and mortgage rates are still high, and home sales are at their weakest pace since the pandemic began. Now its pretty clear that sellers arent slashing asking prices and mortgage rates arent plummeting, so mindsets are shifting. Median asking price $407,225 5.2%

ICE Mortgage Technology will be sunsetting legacy integrations for its flagship Encompass platform by Oct. 31, 2025, which will modernize the mortgage market even if some vendors have to go kicking and screaming. and Mortgage Automation Technologies (which is not SDK-based). ” he said.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content