This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One reason that home prices have stayed elevated is that inventory nationally is still restricted. But if current trends continue, the inventory shortage will be effectively gone by next spring. In fact, while home prices are higher than a year ago, inventory has increased at the rate price appreciation has decreased.

Housing inventory, which saw an excellent pickup a few weeks ago, has been slowing down and last week we saw a slight decline. Has seasonality finally kicked in or did back-to-back hurricanes slow things enough to influence inventory data? Since then, inventory growth has been slowing down and even declined last week.

As mortgage rates rose, homebuyer demand slowed and inventory grew. In 2025, mortgage rates have stayed stubbornly high for yet another spring buying season. Our 2025 housing market predictions are based on the assumption that lower mortgage rates will spur demand and boost the number of homes sales transactions.

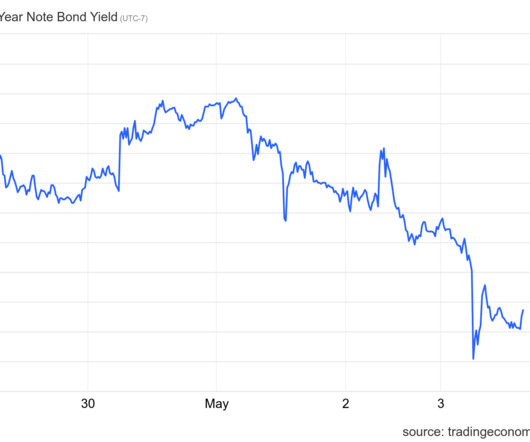

Earlier this year, when mortgage rates soared to 7.26%, a cloud of worry hung over the housing market many feared that home sales would tumble in 2025, fueled by concerns about inflation and tariffs. But when it seemed doom and gloom would prevail, the 10-year yield dropped, pulling mortgage rates lower in a lovely slow dance.

Mortgage rates recently hit a year-to-date low, coinciding with ongoing market disruptions from tariffs. In fact, if mortgage rates head toward 6%, we will have a positive year here. Last year, we saw mortgage rates increase from 6.63% to about 7.50%, leading to challenges in the purchase application data.

Rising housing inventory levels in 2024 may not be the positive sign of market health that they appear to be. High inventory levels contribute to another problem as active listings are remaining unsold for longer periods. Redfin refers to these listings as “stale inventory.” metro areas.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

Notably, we compared the data from 2022 and 2023 and noticed positive year-over-year data starting in October 2024, which you can see in the chart below. However, housing demand surged when mortgage rates fell in the early 1980s during a recession. For me, the highlight of 2024 was the growth in active inventory.

Despite rising mortgage rates through much of 2024, recent indications show growing boldness among homebuyers heading into the new year. These increases are persisting despite mortgage rates near 7%. Mortgage rates have averaged above 6% for the past 24 months. The South led the way with a PHSI reading of 94.5

And while the slower sales pace may not be great news for real estate professionals, it has resulted in an uptick in inventory , which is good news for homebuyers. For-sale inventory at the end of September was 1.39 month supply of unsold inventory, up from 4.2 million, up 1.5% from August and up 23% from one year ago.

Another jobs week has come to an end, and amid the chaotic headlines about job numbers, tariffs , and the leadership of the Treasury , mortgage rates remained calm. Better mortgage spreads are limiting how high rates can rise in 2025. Mortgage spreads refer to the difference between the 10-year yield and the 30-year mortgage rate.

Rising mortgage rates that are now above 7% have continued in January. But there may be some improvement on the horizon as newly listed home inventory grew 37.5% more homes were actively listed for sale on a given day in January, following a 15-month trend of higher annualized inventory levels. year over year.

Mortgage rates are declining, and recent purchase application data shows a promising 9% week-to-week increase and a 2% rise compared to the previous year. I’ve noticed that housing data tends to improve when mortgage rates drop from 6.64% to 6%, especially when I adjust for seasonal demand.

In 2024, more people moved out of Illinois than into the Prairie State. While the markets steady conditions certainly give sellers confidence when listing their homes and ensure buyers know what to expect when entering the market the current market conditions, including higher mortgage rates , are not what many buyers would define as ideal.

The mortgage rate lockdown premise holds that very few people will list their homes when mortgage rates are this high, thus suppressing inventory. But 2024 has proven that theory wrong. 2024 has had healthy inventory growth despite mortgage rates above 7%. This week, we saw inventory growth of 16,532.

Traditionally, home prices soften in the second half of the year and I had counted on this for my price forecast , which predicted 2.33% home-price growth for 2024. As part of our tracker, we focus on purchase application data, and I am always looking to see what level of mortgage rates gives us growth in purchase apps.

As more properties came ontothe market and overall inventory increased for the 17th consecutive month, the U.S. Recent improvements in mortgage rates bode well for the later spring and early-summer housing season, as long as economic concerns settle and dont knock buyers off course. 2024 Change over Mar. Key Highlights U.S.

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025. However, this year, mortgage rates rose during this timeframe.

If this happens, will we see lower mortgage rates this spring? However, last week saw a decline in mortgage rates due to softer economic data, which led to an influx of money into the bond market as stocks sold off on Friday. If we were experiencing the worst mortgage spreads of 2023, mortgage rates would be 0.77% higher today.

All the housing market data for 2024 is in, and its fair to say that the housing market surprised us again! Home prices finished 2024 up a few percent nationally and mortgage rates are at their highest level in seven months back over 7% as we head into January. The elephant in the room is affordability. fewer than a week prior.

Redfin cited a number of reasons for this increase in the nations housing inventory, including: The mortgage rate lock-in effect is fading: A number of homeowners who scored low mortgage rates during the pandemic have been staying put because moving would mean taking on a higher rate. month-over-month, and 4.7% year-over-year.

As low inventory levels, elevated mortgage rates and rising home prices keep the housing industry stagnant, short-term real estate investors — aka fix-and-flippers — faced market turmoil during the third quarter of 2024. The average interest rate for a fix-and-flip loan also rose in Q3 2024 to 10%, according to Kiavi.

The October 2024 results for the S&P CoreLogic Case-Shiller Indices were issued today by the S&P Dow Jones Indices (S&P DJI). In October 2024, the leading indicator of U.S. a modest decrease from the previous 2024 annual gains. home values had an annual growth of 3.6%a year-over-year growth (down from 5.2%

Will inventory levels skyrocket as federal workers leave? Weekly housing inventory ramps up What do we see in the data on housing inventory levels in the D.C. Weekly housing inventory ramps up What do we see in the data on housing inventory levels in the D.C. But inventory remains well below historical averages.

A 60 basis point increase in mortgage rates in October has strangled mortgage demand, particularly for refinancings , according to the latest survey data from the Mortgage Bankers Association. Mortgage applications overall decreased 0.1% The refinance share of mortgage activity decreased to 43.1% the previous week.

In the fourth quarter of 2024, sales were coming in at 5% to 10% more than the year prior. This housing market is on hold until mortgage rates come down. We knew that mortgage rates over 7% were possible for the year, and here we are. Sales are slow, so inventory of unsold homes is building. When will that be?

Mortgage applications decreased 17% from one week earlier as mortgage rates surged, according to data from the Mortgage Bankers Association ’s (MBA) weekly application survey for the week ending October 11, 2024. The refinance index decreased 26% from the previous week and was 111% higher than the same week one year ago.

Mortgage applications for new-home purchases increased 7.2% year over year in November, according to data from the Mortgage Bankers Association ‘s (MBA) builder application survey that was released Tuesday. Applications decreased by 12% from October 2024. That estimate is down 4.6% from the 56,000 sales in October.

Have we seen the peak in housing inventory for 2024? The best part about 2024 has been that higher mortgage rates have created an inventory buffer, so if the economy gets softer and rates fall, we have many more homes to work with than we had in 2020-2023. Weekly inventory change (Aug.

homebuyers continued making historically large down payments in late 2024, responding to a year of record-high upfront housing costs , according to a Realtor.com report. For all of 2024, buyers put down an average of $29,900, or 14.4% in 2024, while transactions below that threshold fell 9.3%. Down payments were 3.4

Have lower mortgage rates already started to slow down housing inventory? I have a simple weekly growth model with the Altos inventory data: when rates are high, over 7.25%, inventory should grow between 11,000-17,000 weekly. Still, I would consider the last month of inventory growth healthy.

At the same time, mortgage rates jumped back over 7%. For the four December weeks in 2024, there were just 44,000 new pending home sales on average for single-family homes. What were trying to track are what the real-time signals are telling us about homebuyers and 7% mortgage rates. fewer homes on the market that a week ago.

The Mortgage Bankers Association (MBA) Builder Application Survey (BAS) data for October 2024 shows mortgage applications for new home purchases increased 8.2 Compared to September 2024, applications increased by 3 percent. The post New Home Purchase Mortgage Apps Jumped Recently first appeared on The MortgagePoint.

As 2025 draws near, mortgage rates are once again in the news. Buying a home in 2024 was surprisingly competitive given how high the affordability hurdle became,” said Skylar Olsen, Zillow Chief Economist. More inventory should shake loose in 2025, giving buyers a bit more room to breathe.” increase in property values in 2025.

Mortgage affordability remained flat in February as the national median monthly payment for purchase loan applicants remained unchanged at $2,205. By product type, the median mortgage payment for conventional loan applicants was $2,226, up from $2,225 in January and up from $2,194 in February 2024. The national PAPI increased 0.1%

Even better, new home sales for the calendar year 2024 are estimated at 683,000, which is 2.5% Still, higher new home sales doesnt begin to offset the gap left by existing-home sales, which were at an almost 30-year low in 2024 at 4.06 Available new-home inventory is on a firm upward trajectory. gain compared to November.

percent)* below the February 2024 rate of 1,546,000. percent below the February 2024 rate of 1,563,000. However, after that decline and when mortgage rates started to fall late in 2022 home sales rebounded all the way back to 741,0000. Then, in late 2022, mortgage rates fell, and the builders started selling homes again.

This is measurable in both the total unsold inventory and the number of new listings each week. Because each week we have 815% more sellers than last year, the total inventory will continue to build unless and until demand shifts dramatically, which would require notably lower mortgage rates. Those do not seem imminent.

My model for inventory growth with higher mortgage rates came crashing down last week. After two weeks of significant increases , inventory growth slowed dramatically and is far from my 11,000-17,000 growth model with mortgage rates over 7.25%. When mortgage rates increase, demand falls and the price-cut percentage grows.

Despite the recent rise in mortgage rates, early indicators suggest that the housing market is pointed in the right direction. The October pending sales data is a sign that fourth-quarter sales will be strong enough so that 2024 sales end up higher than 2023,” Bright MLS chief economist Lisa Sturtevant said in a statement.

We track inventory and home sales very closely, so the biggest surprise this year has been the resiliency of home prices. Given the unrelenting mortgage costs, generally weak homebuyer demand, and the year’s rising supply of unsold homes, I’ve been expecting home prices to recede a bit in the second half of this year. They have not.

The mortgage rate lockdown premise says that if rates rise, inventory can’t grow meaningfully. The idea is that nobody will trade their low mortgage rates to buy another home — even though this happened every week last year. With mortgage rates higher, will this stop inventory from growing year over year?

Have we seen the bottom in mortgage rates for 2024 after a crazy roller coaster ride so far this year? My 2024 forecast had a mortgage rate range of 7.25%-5.75%. To get to the lower end of this range, we needed to see two things: the labor market getting softer and the mortgage spreads improving. year over year.

Housing inventory, new listing data and mortgage rates are all rising, but the price cut data percentages are falling. I will watch for rising mortgage rates to see if they change the weekly data. I will watch for rising mortgage rates to see if they change the weekly data. So far, so good in 2024.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content