This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mortgage rates recently hit a year-to-date low, coinciding with ongoing market disruptions from tariffs. In fact, if mortgage rates head toward 6%, we will have a positive year here. Last year, we saw mortgage rates increase from 6.63% to about 7.50%, leading to challenges in the purchase application data.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

Earlier this year, when mortgage rates soared to 7.26%, a cloud of worry hung over the housing market many feared that home sales would tumble in 2025, fueled by concerns about inflation and tariffs. But when it seemed doom and gloom would prevail, the 10-year yield dropped, pulling mortgage rates lower in a lovely slow dance.

Todays housing starts data exceeded estimates; however, a closer examination of the report with the builder confidence reveals that the recent rise in mortgage rates , approaching 7.25%, has negatively affected builder sentiment. Since late 2022, our analysis indicates that mortgage rates in the 6%-6.5% This is 15.8 percent (14.4

Another jobs week has come to an end, and amid the chaotic headlines about job numbers, tariffs , and the leadership of the Treasury , mortgage rates remained calm. Better mortgage spreads are limiting how high rates can rise in 2025. Mortgage spreads refer to the difference between the 10-year yield and the 30-year mortgage rate.

Mortgage demand decreased 8.5% for the week ending April 11, according to the Mortgage Bankers Association (MBA)’s weekly applications survey a stark contrast to the 20% increase seen a week earlier. But this week’s data revealed that the adjustable-rate mortgage (ARM) share of activity increased to 9.6%

Mortgage rates continue to rise, serving as a bucket of cold water for lenders and consumers that were warming to lower borrowing costs just a few months ago. According to HousingWire ‘s Mortgage Rates Center , the average 30-year conforming rate was 6.61% on Tuesday. in 2023, but starts for attached properties rose by 3.2%

Lower mortgage rates in September had a measurable impact on home sales. Pending home sales data is the latest sign that falling mortgage rates in August and September boosted home sales. According to data released Wednesday by the National Association of Realtors (NAR), pending home sales in September jumped 7.4% year over year.

Mortgage rates are declining, and recent purchase application data shows a promising 9% week-to-week increase and a 2% rise compared to the previous year. I’ve noticed that housing data tends to improve when mortgage rates drop from 6.64% to 6%, especially when I adjust for seasonal demand.

House of Representatives proposes to relieve Federal Housing Administration (FHA) borrowers of mortgage insurance premiums (MIPs) once they reach a certain level of home equity , aligning FHA policies with those of conventional loans. Mortgage insurance exists as protection from foreclosure on low equity loans. Introduced by Reps.

By at least one measurement, affordability is improving for prospective homebuyers, even as home prices continue to rise and mortgage credit availability remains relatively low. According to data released Thursday by the Mortgage Bankers Association (MBA), the median payment for purchase loan applicants declined by 0.8%

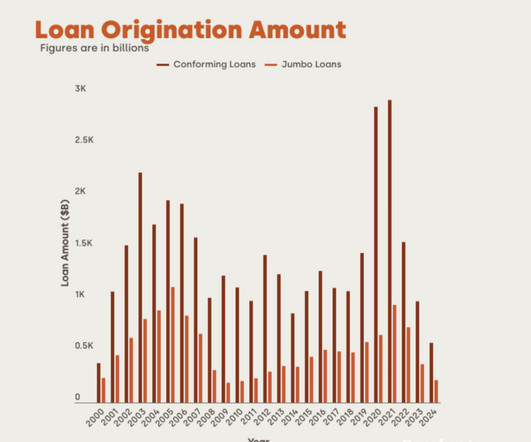

An examination of CoreLogic data indicates that, in comparison to prior years, jumbo mortgage originations saw a discernible drop in both dollar quantities and market share in 2023 and 2024. Jumbo loan volumes plummeted 61% and conforming loan volumes fell 67% from their peak in 2021 to 2023.

The difference is mortgage rates: even with inventory growing at a healthy clip this year, mortgage rates just heading down toward 6% for a brief period of time resulted in higher prices in a seasonally soft period. million in October 2023). However, that didn’t happen. from September to a seasonally adjusted annual rate of 3.96

Its late December so all the 2025 mortgage rate forecasts have been published. Most housing market analysts expect mortgage rates to spend the year with a 6 handle. The most optimistic predictions assume 2025 will see mostly low 6s for the 30-year fixed rate mortgage. Unfortunately, all of them are already wrong.

Reverse mortgage industry leader Finance of America (FOA) announced updates on Thursday to the interest rate for HomeSafe Second, its proprietary second-lien reverse mortgage product. It will also be available in four new states, bringing the total to 10 with more planned for 2025. The new states are Arizona, Nevada, Oregon and Utah.

A jump in mortgage rates led to mortgage application volume falling 8.5% during the week ended April 11, according to the Mortgage Bankers Associations (MBA) Weekly Applications Survey. percent was the highest since November 2023, and this reflects the share of units. The ARM share at 9.6

Mortgage rates fell this week and they are now far from the levels widely discussed after the election. With the final jobs report for 2024, mortgage rates made a nice move lower today, and its been a positive story this week. The mortgage spreads did improve a lot on Friday, too, which helped with rates, so start spreading the news.

Economists pointed to lower mortgage rates as the reason for slower growth. gain compared to August 2023. Despite the Federal Reserve’s half-point interest rate cut in September, rates for 30-year conforming loans have climbed back up to 6.7%, according to HousingWire ’s Mortgage Rates Center. gain from July. That’s down from 5.9%

This is in line with the Mortgage Bankers Association ‘s (MBA) Purchase Applications Payment Index (PAPI), which uses information from the MBA Weekly Applications Survey (WAS) to calculate how new monthly mortgage payments change over time in relation to income. It is down by $114 from one year ago, equal to a 5.3% The PAPI is down 9.1%

Mortgage technology company Gateless is offering its flagship automated underwriting platform to a new lender. The artificial intelligence-based platform, the latest addition to the Gateless AI mortgage tool suite, aims to enhance The Loan Store’s underwriting capabilities.

CrossCountry Mortgage , a top-10 U.S. mortgage lender, has hired a team of former Pennymac Financial Services executives to lead its capital markets and investment-related activities. Fartaj stepped down as Pennymac’s senior managing director and chief investment officer in March 2023 , after 15 years at the company.

The rule applies existing protections for residential mortgages to borrowers who seek PACE loans to upgrade or renovate their homes through clean energy technology. The concept of bolstering consumer protections for these loans was first announced in May 2023. The rule goes into effect on March 1, 2026, according to the CFPB.

mortgage delinquency rate increased significantly in November, rising 8.38% compared with October, according to ICE Mortgage Technologys First Look report. The foreclosure pre-sale inventory rate was about 0.34%, down about 2.09% compared with October and down nearly 16% compared with November 2023.

As low inventory levels, elevated mortgage rates and rising home prices keep the housing industry stagnant, short-term real estate investors — aka fix-and-flippers — faced market turmoil during the third quarter of 2024. But the share of flipped homes sold for less than $300,000 increased from Q3 2023.

If this happens, will we see lower mortgage rates this spring? However, last week saw a decline in mortgage rates due to softer economic data, which led to an influx of money into the bond market as stocks sold off on Friday. If we were experiencing the worst mortgage spreads of 2023, mortgage rates would be 0.77% higher today.

There were a total of 298 consumer complaints submitted to the Consumer Financial Protection Bureau (CFPB) in 2024 that were related to the reverse mortgage industry, according to a database maintained by the bureau. This was 63 fewer complaints than in 2023. Among the nation’s top 10 reverse mortgage lenders, Onity Group Inc.

a figure substantially higher than year-ago levels due to ongoing mortgage rate optimism. The index reported that consumers continue to expect mortgage rates to decline over the next 12 months. In December 2024, the share of consumers that expected mortgage rate shrinkage held steady at 42%, lower than November’s 45%.

Mortgage applications declined 0.7% 13, driven by slight decline in refinance activity, according to data released Wednesday by the Mortgage Bankers Association (MBA). The decline in applications broke a five-week streak of increases in mortgage demand. Adjustable-rate mortgage (ARM) activity remained steady at 5.3%

Over the past year, members of the reverse mortgage industry have been making a more concerted effort to connect with their counterparts in the forward mortgage space. And some reverse-only companies have aimed to establish firmer ties with the much larger forward mortgage industry.

billion profit in 2023. In 2024, Fannie Mae provided $381 billion of liquidity to the single-family and multifamily mortgage markets. billion, relatively flat to 2023. billion in net income in 2024, a decrease of $425 million compared to 2023. .” billion in net income in 2024, consistent with 2023.

Reverse mortgage professionals have long sought financial advisors as referral sources, but might find that those professionals are not particularly willing to entertain the notion that the product would be right for their clients.

Employment data for October is set to be released Friday, and it will go a long way in determining the path for mortgage rates, which have surged upward in the past month. At HousingWire’s Mortgage Rates Center on Tuesday, the average rate for 30-year conforming loans was 6.72%. This equated to homes being 9.2%

The labor market is showing signs of softness but is not breaking down yet, which has kept mortgage rates higher for longer. Since 2022, my guiding principle has been that the labor market is more important than inflation in determining mortgage rates. This is the reason mortgage rates are around 7% and not around 6% today.

Mortgage applications for new-home purchases increased 7.2% year over year in November, according to data from the Mortgage Bankers Association ‘s (MBA) builder application survey that was released Tuesday. Applications decreased by 12% from October 2024.

Mortgage applications increased 5.4% 6, stemming from a 27% jump in refinance activity, according to a report released Wednesday by the Mortgage Bankers Association (MBA). This is the latest weekly increase in mortgage applications, following a trend of steady demand increases over the past several weeks. share a week prior.

As 2025 draws near, mortgage rates are once again in the news. million existing home sales in 2024, a little increase over 2023’s 4.1 In September, mortgage rates dropped, momentarily raising the proportion of affordable properties to a 19-month high. Zillow predicts 4.3 million and 2024’s anticipated 4 million.

Mortgage rates continued their ascent this week after Fridays jobs report showed that employers added more positions than expected in December, which is likely to cement a pause on interest rate cuts by the Federal Reserve later this month. Merritt thinks mortgage lenders could take some comfort in that trend.

Highlands Residential Mortgage announced that Daniel McCoy is joining the company as a regional construction loan manager for the Southeast. Daniel McCoy McCoy leads the construction-focused McCoy Mortgage Team , which has previously affiliated with companies like MVB Mortgage , Intercoastal Mortgage and Cardinal Financial.

homeowners with mortgages nationwide have an interest rate higher than or equal to 6%, the highest percentage since 2016. in Q3 of 2023, that is an increase of almost five percentage points. of homeowners who hold mortgages is less than 6%. of homeowners with mortgages had a rate below 6% in Q3 of 2023.

Cornerstone Financing , a venture co-founded by former Reverse Mortgage Funding (RMF) CEO Craig Corn, has secured $285 million in financing through global investment firms Aquiline Capital Partners LP and Nomura. In 2013, Corn and his partners launched RMF , which became a leading reverse mortgage lender. 31 of that year.

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025. However, this year, mortgage rates rose during this timeframe.

Independent mortgage banks ( IMBs ) and mortgage subsidiaries of chartered banks reported an average profit of $443 on each loan they originated in 2024, up from an average loss of $1,056 per loan in 2023, according to the Mortgage Bankers Association (MBA)’s annual Mortgage Bankers Performance Report.

With fluctuating mortgage rates and economic pressure in the housing market, foreclosure activity ramped up in October 2024. That’s up 4% from September’s total of 29,668 but down 11% from the October 2023 figure of 34,472. According to real estate data provider Attom , homebuyers may face more challenges heading into 2025.

million in Q3 2023. Its funded volume was also driven by growth in refinance and home equity originations, including home equity lines of credit ( HELOCs ) and closed-end second-lien mortgages. “In Better Home & Finance Holding Co., the parent of digital lender Better , reported a net loss of $54.1 million in Q2 2024 and $353.9

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content