This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Potential home sellers notice weak demand, fewer offers and price reductions, prompting them to back away from the market. If potential sellers avoid the market, this will keep a lid on supply growth. Newlistings are hitting the market Last year was an environment with 5% to 10% more sellers each week than a year prior.

However, there are two big trends that stand out as we launch into 2025 affordability and sellers in the market. If we get lucky on economic news and spreads continue to tighten a bit, we could see some alleviation to the affordability vice everyone is now in. These are unsold newlistings.

Florida had an uptick in inventory with a bit of a rebound in newlistings now that the storms are over. Newlistings go up This year continues to have slightly more sellers than last year but fewer than we used to get in past years. There were 60,000 newlistings unsold this week for single-family homes.

This is measurable in both the total unsold inventory and the number of newlistings each week. Because each week we have 815% more sellers than last year, the total inventory will continue to build unless and until demand shifts dramatically, which would require notably lower mortgage rates. Those do not seem imminent.

Newlistings move upward, but remain historically low Altos uses new real estate listings data as a key indicator of seller activity in the D.C NewListings are the homes that were listed for sale in a given week and added to the active inventory. housing market. As unemployment in D.C

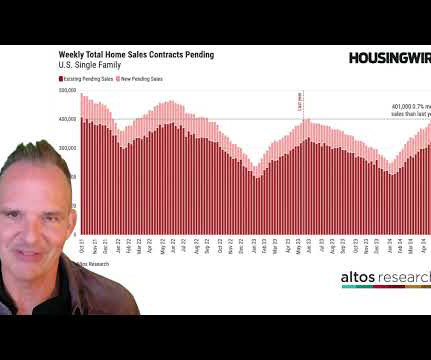

Newlistings To get a lot of homes on the market though we need some sellers. There were only 54,000 newlistings of single-family homes unsold this week. There were another 10,000 newlistings immediate sales which makes 64,000 homesellers. Unsold newlistings amount to 4.8%

Additionally, our weekly pending contract data and newlistings are trending positively compared to last year. Last year, I estimated that a minimum of 80,000 homes would be listed every week during the peak seasonal months, and my prediction was only off by 5,000.

24): Inventory fell from 569,898 to 565,875 The all-time inventory bottom was in 2022 at 240,497 The inventory peak for 2024 so far is 739,434 For some context, active listings for this week in 2015 were 1,104,310 Newlistings data While active inventory didn’t rise, we did get a nice boost in newlistings this last week.

Newlistings volume is trying to grow with its biggest week since September. List prices inched up for the week, though sales prices did not advance. These active market listing prices lead the sales prices so theyre very valuable to track. NEWLISTINGS There was a nice jump in the newlistings volume this week.

One of my critical forecasts for 2024 was the growth of newlistings data and active inventory, even with higher mortgage rates. However, the newlistings data has slightly disappointed me. Newlistings data I am pleased that we’ve seen newlistings data grow year over year — it’s a big step forward.

That shortage reached its crisis peak in January 2022. Supply growth could also come from more sellers, such as investors or distressed borrowers unloading. However, in most of the country, we have no growth from the seller side. Weve been averaging about 8% more sellers each week than a year ago.

Remember that 2023 had the lowest newlistings data ever and 2024 will have the second lowest. One of the reasons total inventory data hasn’t gotten back to 2019 levels is the lack of sellers in 2023 and 2024. The price-cut percentage data is below 2022 levels and risks an earlier seasonal curve lower than 2022 and 2023.

The New Years week was expected to be slow, so it’s no surprise that newlistings and sales are down. The Christmas and New Year’s holidays fell on Wednesdays this year, which messes up two full weeks in terms of getting home sales done and tracking the numbers. Those will start rebounding in next weeks data.

Data from Altos Research shows an area with expensive housing, rising inventory and conditions that lean favorable to sellers. LAs housing market has largely stabilized after the turbulence of the post-pandemic years and the rapid rise of mortgage rates beginning in 2022. The current median home price is $1.47 million, $3.9

The weekly volume of newlistings is now higher than at anytime last year. It’s still April, so there could be as many as eight more weeks of seller growth in the spring housing market. And seller growth is happening pretty much everywhere across the country, with Florida and Texas leading the way. orate further?

Newlistings rise There were just under 61,000 newlistings unsold this week. When you include the 9,400 immediate sales, the total is 13% more sellers than a year ago. Last year at this time, the market was in deep retrenchment — both buyers and sellers were walking away. Sellers could dip again next week.

The rules of supply and demand economics always end up winning and weekly newlisting data is key. Newlisting data is growing year over year, but it will be the second-lowest newlisting data ever recorded in history. 2024 has a much healthier inventory level.

In 2022, it was the end of the post-pandemic boom and buyers were rushing to get a home before mortgage rates climbed, so there was steep price appreciation in the first half of the year. But by June, prices peaked for the year while remaining below the June 2022 peak. Home sellers and listing agents know where demand is for homes.

Now its pretty clear that sellers arent slashing asking prices and mortgage rates arent plummeting, so mindsets are shifting. Key findings from the four weeks ending January 26: Before the seller accepted an offer, the average U.S. Key findings from the four weeks ending January 26: Before the seller accepted an offer, the average U.S.

Mortgage interest rates above 6% continued to impact potential homebuyers’ purchase power, while also contributing to a lock-in effect among would-be home sellers who bought their homes years ago with a mortgage rate of 3% to 4.5%,” the association explained in an announcement. “Newlistings of single-family homes were up 16.7%

There’s a showdown at the housing market corral between homebuyers and sellers. It facilitated a very unhealthy housing market in 2020-2021 that became savage in 2022. To top it all off, we started 2022 at all-time lows, forcing bidding action everywhere until mortgage rates rose. Now fast forward to 2022.

In the 24 months beginning March 2022, the U.S. After an initial rush to get to market in Q2 2022, newlistings volume fell precipitously. In July 2022, newlistings volume per week dropped from 90,000 at the end of June to approximately 74,000 just after the July 4th holiday.

Newlistings remain low as owners lock in Altos’s data for newlistings accounts for single-family homes that come to market without an immediate or pending contract. Newlistings for single-family homes or condos are key indicators of seller behavior and newlistings ramped up during the week of Feb.

It looks like we’re heading back to those conditions of the second half of 2022 where inventory grew rapidly, but any real downside correction was mitigated with a withdrawal of supply. Sellers can just wait it out, and it looks like the U.S. I think it’s worth examining if sellers will indeed just wait it out now.

Active listings of homes for sale rose to the highest level since early in the pandemic. Newlistings hit the highest level since July 2022, increasing 1.9% I have sellers saying, I think were at the top of the marketIm ready to cash out and put my money into another investment. They climbed 0.3% year-over-year.

In the 24 months beginning March 2022, the U.S. However, if you ask, most people think the mortgage lock-in occurred in 2022. million fewer home sales between March 2022 and December 2023. What’s not measured in the FHFA paper is how by 2023, seller volume had already been declining for nearly a decade.

Sales are sluggish because high homebuying costs are making both house hunters and prospective sellers skittish. Even though homes are selling for higher prices than ever before, many sellers are still having to drop their list prices after putting their properties on the market—one positive sign for potential homebuyers.

metropolitan areas in February 2022, based on year-over-year growth in median listing price according to the residential real estate listing website, Realtor.com. The table also reports the year-over-year percent change in newlistings for each market. Table 1, below, reports the 10 hottest U.S. Panama City, FL 39.7%

in February of previous year, indicating that sellers are becoming more accustomed to the present market conditions. The number of newly listed homes grew 4.2% over the previous year, making 2019 February the most active month for sellers since 2021. Key Findings: Newly listed homes increase 4.2% Newlistings +4.2% -13.7%

The second dynamic to watch here is how many sellers are cutting their prices each week. It’s not as steep as 2022 — the market now is not shifting as quickly from big growth to price declines, like it did briefly about 18 months ago. NewlistingsNewlistings appear to have peaked for the year three weeks ago.

At least, that’s what the data seems to suggest as inventory grows and newlistings decline at a less aggressive rate than last year. Newlistings decline isn’t as steep as a year ago There were only 53,000 newlistings (single-family homes) unsold this week, plus 10,000 more newlistings that are already in contract.

Typically we have a natural set of newlistings each year; inventory rises in the spring and summer and then falls in the fall and winter. in 2021 and as high as 6.25% in 2022. It wasn’t the rate move that caught my attention — it was the newlisting data. But now this is a real risk. The parts of the U.S.

Newlistings climbed during the past week and there are now 72,000 more single-family homes on the market. It appeared that newlistings might be on the decline already, but the pace picked up a tad this week, which is encouraging. No one wants a scenario in which there’s a flood of sellers but no buyers.

Inventory , newlistings, etc. Newlistings volume peaked a few weeks ago. While there won’t be a big drop off for newlistings in July, we can assume we’ll have fewer sellers each week through the rest of the year. There won’t be a big drop-off in newlistings volume in July.

We created this weekly tracker at the end of 2022 to give people a live weekly outlook on everything that drives the housing market and which factors to follow. 9, 2022, and they’ll be ready for what’s coming next. So today’s tracker is focused on 2023, the inventory data, and how different this year was from 2022.

We’re rapidly approaching the peak of the market in terms of sellerlistings, and as inventory builds, the sales rate will peak by the end of June. Newlistings Growing inventory is not just about slowing demand. We are also consistently measuring more sellers coming back into the market. Now we’re at 69,000.

However, let’s keep an eye out on this story over the next six months because of what late 2022 and 2023 data has shown us: if the mortgage rates fall and we can get at least two to three months’ worth of positive data, it will show up in the future existing home sales report.

Mortgage spreads The spread between the 30-year mortgage rate and the 10-year yield has been an issue since 2022 and things got worse after the March 2023 banking crisis. If mortgage rates keep falling and demand picks up, we will have a much better buffer with active inventory than in 2022 and 2023.

Even with all the drama we have dealt with in 2022-2023, the housing market stayed intact and never broke. However, one thing is sure: from 2020 to 2023 we never saw credit-stressed home sellers. However, the key to this data line is that we want to see real year-over-year growth in the spring of 2024 — back to levels of 2021 and 2022.

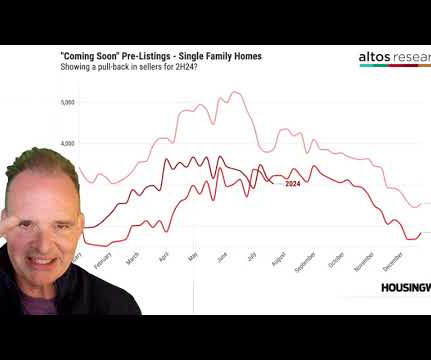

Our Immediate sales measure of homes that get listed, take offers and go into contract in a few days is also notably lower than last year. On the supply side, newlistings are slightly more than a year ago, but pulling back. If fact the “coming soon” pre-listings are now running behind last year by 5%.

We’re rebounding inventory after the holiday, so it’s not that much of a surprise, and it’s less of a jump than what was happening at this time in 2022. Newlistings rise This week saw 69,000 new single family listings unsold. So that’s a total of 84,000 total newsellers for single-family homes this week.

If you need to communicate about the real estate market with buyers and sellers, you should join us. It’s the peak season for buyers and sellers. Remember that, back in 2022, as mortgage rates were rising quickly, so too was inventory. There are more sellers now as rates have stayed higher for longer. That’s up 1.5%

Massachusetts and New York, for example, are still just coming off the record tight markets of the pandemic, but that trend is changing — finally. Newlistings show 12% more sellers than a year ago When we look at the new supply hitting the market each week, we see the same trend we’ve had for a few months.

I like to point out that consumers are more sensitive to changes in mortgage rates than to the absolute levels, and since rates are now basically unchanged for the month, just easing down from the early March peak of 7.2%, sellers and buyers are tip-toeing back into the market. More sellers means more sales will happen.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content