This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

Mortgage rates recently hit a year-to-date low, coinciding with ongoing market disruptions from tariffs. In fact, if mortgage rates head toward 6%, we will have a positive year here. Last year, we saw mortgage rates increase from 6.63% to about 7.50%, leading to challenges in the purchase application data.

Earlier this year, when mortgage rates soared to 7.26%, a cloud of worry hung over the housing market many feared that home sales would tumble in 2025, fueled by concerns about inflation and tariffs. But when it seemed doom and gloom would prevail, the 10-year yield dropped, pulling mortgage rates lower in a lovely slow dance.

Todays housing starts data exceeded estimates; however, a closer examination of the report with the builder confidence reveals that the recent rise in mortgage rates , approaching 7.25%, has negatively affected builder sentiment. Since late 2022, our analysis indicates that mortgage rates in the 6%-6.5%

Higher-for-longer mortgage rates have claimed their first victim of 2025. Ally Financial announced Wednesday that it would exit the mortgage origination business as part of a broader strategy to pursue higher returns on investments. But by 2022, Ally recorded a $136 million impairment tied to its investment in Better.

Another jobs week has come to an end, and amid the chaotic headlines about job numbers, tariffs , and the leadership of the Treasury , mortgage rates remained calm. Better mortgage spreads are limiting how high rates can rise in 2025. Mortgage spreads refer to the difference between the 10-year yield and the 30-year mortgage rate.

Mortgage rates continue to rise, serving as a bucket of cold water for lenders and consumers that were warming to lower borrowing costs just a few months ago. According to HousingWire ‘s Mortgage Rates Center , the average 30-year conforming rate was 6.61% on Tuesday. With mortgage rates back above 6.5%

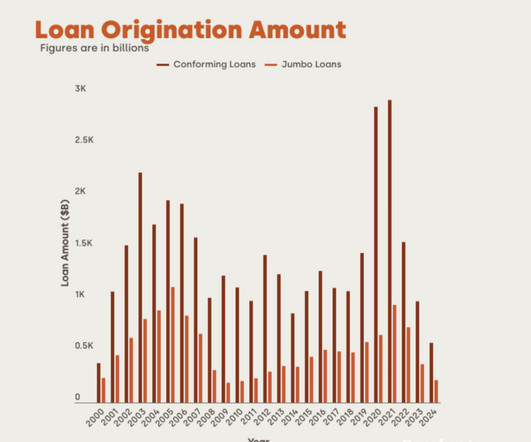

An examination of CoreLogic data indicates that, in comparison to prior years, jumbo mortgage originations saw a discernible drop in both dollar quantities and market share in 2023 and 2024. Origination volumes decreased in 2022 as interest rates rose. Since 2014, this is the lowest level.

Mortgage rates are declining, and recent purchase application data shows a promising 9% week-to-week increase and a 2% rise compared to the previous year. I’ve noticed that housing data tends to improve when mortgage rates drop from 6.64% to 6%, especially when I adjust for seasonal demand.

The labor market is showing signs of softness but is not breaking down yet, which has kept mortgage rates higher for longer. Since 2022, my guiding principle has been that the labor market is more important than inflation in determining mortgage rates. This is the reason mortgage rates are around 7% and not around 6% today.

By at least one measurement, affordability is improving for prospective homebuyers, even as home prices continue to rise and mortgage credit availability remains relatively low. According to data released Thursday by the Mortgage Bankers Association (MBA), the median payment for purchase loan applicants declined by 0.8%

The market reacted badly to the FOMC statement and remarks by Federal Reserve Chairman Powell during the Q&A presser, sending the 10-year yield and mortgage rates higher. What he got is higher mortgage rates again. I’ve been cautious about getting to sub-6% mortgage rates until the labor breaks. So what gives?

According to Alt os Research , the median list price for a condo in Miami-Dade County last week was $505,000, down from the peak of $620,000 on July 1, 2022. One Florida mortgage broker said the Provident exit gave him “a feeling that we will see other major lenders exiting the condominium market in Florida.

Economists pointed to lower mortgage rates as the reason for slower growth. According to Bright MLS, it’s the slowest annual gain in 2024 thus far and the first monthly decline since December 2022. On a non-seasonally adjusted basis, the national home price index posted a 4.2% gain year over year, less than the 4.8% gain from July.

This is in line with the Mortgage Bankers Association ‘s (MBA) Purchase Applications Payment Index (PAPI), which uses information from the MBA Weekly Applications Survey (WAS) to calculate how new monthly mortgage payments change over time in relation to income. Since August 2022, it is at its lowest point. in August by 0.8%

Labor over inflation has been my mantra since late 2022. This gives us a glimpse of what may happen over the next 10 months for mortgage rates, especially since, since Jan. However, there is a limit to the downside on mortgage rates until the labor market breaks, or we get more than 1% rate cuts from the Fed.

homeowners with mortgages nationwide have an interest rate higher than or equal to 6%, the highest percentage since 2016. of homeowners who hold mortgages is less than 6%. of homeowners with mortgages had a rate below 6% in Q3 of 2023. in the middle of 2022. of mortgaged U.S. Compared to 12.3%

There were a total of 298 consumer complaints submitted to the Consumer Financial Protection Bureau (CFPB) in 2024 that were related to the reverse mortgage industry, according to a database maintained by the bureau. Among the nation’s top 10 reverse mortgage lenders, Onity Group Inc. the parent company of PHH Mortgage Corp.

California -based direct lender AmeriTrust Mortgage announced a new addition to its leadership team. The company welcomed veteran mortgage executive Jett Farrington this week as its new chief operating officer. Schoep told HousingWire that Farrington has a proven track record of leadership, expansion and mortgage industry expertise.

The Mortgage Bankers Association (MBA) Builder Application Survey (BAS) data for October 2024 shows mortgage applications for new home purchases increased 8.2 The average loan size picked up to almost $410,000, the highest in the survey since August 2022. percent compared from a year ago. percent, RHS/USDA loans composed 0.4

If this happens, will we see lower mortgage rates this spring? However, last week saw a decline in mortgage rates due to softer economic data, which led to an influx of money into the bond market as stocks sold off on Friday. If we were experiencing the worst mortgage spreads of 2023, mortgage rates would be 0.77% higher today.

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025. However, this year, mortgage rates rose during this timeframe.

Cornerstone Financing , a venture co-founded by former Reverse Mortgage Funding (RMF) CEO Craig Corn, has secured $285 million in financing through global investment firms Aquiline Capital Partners LP and Nomura. In 2013, Corn and his partners launched RMF , which became a leading reverse mortgage lender. 31 of that year.

At the beginning of 2024, mortgage technology company LoanPASS was announced as a technology partner for reverse mortgage lender Smartfi Home Loans. Getting the hang of reverse Mitchell is a 25-year veteran of the mortgage technology space, primarily working for LOS companies. What does the future hold?

As 2025 draws near, mortgage rates are once again in the news. Mortgage Rates to Drop, Increase, & Drop Again in 2025 Although there are indications that mortgage rates may ease in 2025, as we witnessed in 2024, mortgage rates rarely move in the anticipated direction.

Tim Nelson, a longtime reverse mortgage industry professional and reverse department manager at VIP Mortgage in Scottsdale, Arizona , spent 20 years in the home lending arena before shifting his focus entirely to reverse. Nelson is now a reverse mortgage borrower in addition to being an industry professional.

median rent is still only $17 (-1.0%) below its peak from August 2022, despite the overall fall. from its peak in October 2022. The post Buyers and Sellers Embrace Market in Wake of Mortgage Rate Dip first appeared on The MortgagePoint. At $1,743, the median asking rent decreased by $8, or -0.5%, from the prior year.

After over three decades of leadership, Robert Wagnon, CEO and founder of Republic State Mortgage Co. It has been the honor of my professional life to be the founder and leader of Republic State Mortgage Co. advocacy group representing smaller mortgage lenders. for the past 31 years, Wagnon said.

Reston, Virginia -based mortgage software company RETR announced this week that it has hired two new senior leaders to guide the company’s growth efforts. Before joining RETR, she founded PlacedE, a boutique mortgage recruiting and coaching firm. RETR was founded in 2022 by Wynands and chief technology officer Steven Mincemoyer.

Mortgage credit availability ramped up in January, according to a report released Tuesday by the Mortgage Bankers Association (MBA) that analyzed data from ICE Mortgage Technology. The MBA’s Mortgage Credit Availability Index (MCAI) increased by 250 basis points (bps) on a monthly basis to 99.0 in January 2025.

The report is based on a sample of mortgage applications from 2018 to 2022, and it examines flood risk in the southeast and central southwest census regions of the United States, according to flood risk data from the Federal Emergency Management Agency (FEMA) and the First Street Foundation.

New home sales arent crashing anymore New home sales peaked in October of 2020 with 1,031,000 new home sales and then in 2022 that number crashed all the way down to 519,000 by June. However, after that decline and when mortgage rates started to fall late in 2022 home sales rebounded all the way back to 741,0000.

Weekly housing inventory data Four weeks ago was the best week of inventory growth in 2024, as we hit my model range without higher mortgage rates : I gave it the chef’s kiss. Rising mortgage rates last year and this year have created a growing level of price cuts, especially when inventory rises.

Sierra Pacific Mortgage has hired Suzy Lindblom as its new Chief Operating Officer, the company announced in a LinkedIn post. With more than 40 years of experience in the mortgage industry, Lindblom was most recently chief operating officer (COO) at lender and servicer Arc Home , serving in that role from August 2022 to February 2024.

As Zillow expands into mortgage and other products, they should increase that rate, too. Mortgage in particular is an exciting proposition. Mortgage in particular is an exciting proposition. Zillow’s been scaling its call center mortgage business since 2022, and in 2024 achieved $3.1

This is due to several factors, including rising housing costs, stagnant wages, and a decline in the availability of small-dollar mortgages, defined as those for homes priced at $150,000 or below. Cities: A Qualitative Analysis ” and “ The Socioeconomic Consequences of the Decline in Small Mortgages.” Authored by Craig J.

Mortgage applications increased 2.3% The Mortgage Bankers Association ‘s market composite index increased 6% on an unadjusted basis compared with the previous week. The refinance share of mortgage activity increased to 40.2% on a seasonally adjusted basis in the latest MBA survey. of total applications from 39.0%

at the beginning of 2022 and 30.5% The lock-in effect has begun to lessen, in part because people are sick of waiting for mortgage rates to drop before selling their house and looking for a new one. During that time, the lock-in effect and rising mortgage rates caused a decline in the inventory of existing homes. in Q2 of 2022.

housing market slowed down in the third quarter due to rising home prices and higher mortgage rates , investor purchases also ramped down, according to a new report by Redfin. in Q1 2022, when investors were taking advantage of low mortgage rates. As the U.S. Investors purchased $38.8 Now there’s a middle ground.

Fairway Independent Mortgage Corp. Department of Justice (DOJ) over the regulators’ allegations of mortgage lending discrimination in majority-Black neighborhoods of the Birmingham, Alabama , metro area. The agreement, which was submitted for court approval, requires the Madison, Wisconsin-based mortgage lender to pay a $1.9

Because each week we have 815% more sellers than last year, the total inventory will continue to build unless and until demand shifts dramatically, which would require notably lower mortgage rates. That pace slowed dramatically in 2022 and turned negative in January 2023. Ive highlighted those in the green line here from 2022.

Consumer confidence in the housing market increased in October, reaching its highest level since February 2022, according to Fannie Mae’s Home Purchase Sentiment Index. The share of consumers who think it’s a good time to buy a home increased to 20%, while the share who think it’s a good time to sell a home declined to 64%.

Given the unrelenting mortgage costs, generally weak homebuyer demand, and the year’s rising supply of unsold homes, I’ve been expecting home prices to recede a bit in the second half of this year. Maybe next year, if mortgage rates stay in the high 6s, inventory will build closer to the old normal after five years of a severe shortage.

Without more clarity on mortgage rates , substantial growth in housing permits is unlikely. My initial impression is that sales are not plummeting as they did in 2022, but are also not experiencing significant growth. We are maintaining a steady level, with the best results appearing when mortgage rates approach 6%.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content