This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Potential home sellers notice weak demand, fewer offers and price reductions, prompting them to back away from the market. If potential sellers avoid the market, this will keep a lid on supply growth. New listings are hitting the market Last year was an environment with 5% to 10% more sellers each week than a year prior.

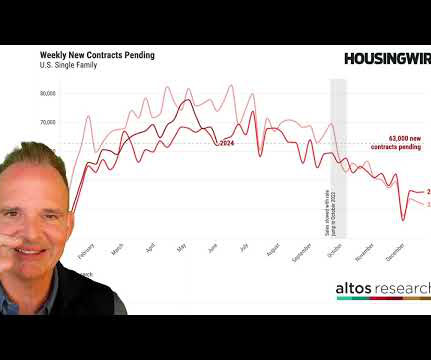

Data from Altos Research shows that higher mortgage rates aren’t necessarily keeping sellers from listing their homes. New pending sales are also on the rise, with the 60,000 homes going under contract last week representing a 9% increase from the same week last year and an 11% increase from the same week in 2022.

However, there are two big trends that stand out as we launch into 2025 affordability and sellers in the market. The other trend to watch is whether we finally have more sellers entering the market in 2025. There are some signals that seller volume is starting to creep back to normal levels. fewer than a week prior.

The median price of the homes that went into contract this week — these are the new purchase offers with contracts pending — is now 6% greater than last year. New listings go up This year continues to have slightly more sellers than last year but fewer than we used to get in past years. Home prices ticked up this week.

New listings To get a lot of homes on the market though we need some sellers. In total, it was another week with fewer home sellers that last year. Its hard to grow inventory too much when there arent many sellers. Demand is slower so more of the sellers are sitting on the market. Thats not a ton. more than a year ago.

The Consumer Financial Protection Bureau (CFPB) on Tuesday released an advisory opinion stating that contracts for deed are under federal home lending rules and should provide consumer protections. According to a CFPB, sellers typically target low-income borrowers, particularly in Black, Hispanic, immigrant, and religious communities.

It’s still April, so there could be as many as eight more weeks of seller growth in the spring housing market. And seller growth is happening pretty much everywhere across the country, with Florida and Texas leading the way. The bearish take is that there are many more sellers than buyers and inventory is rising. That’s up 2.4%

While Monestier, who reportedly sold her Rhode Island home in 2022 and is part of the affected class, believes sellers were paying “inflated commissions,” she feels that prior to the settlement changes going into effect, the rules governing the industry were “clear and confusion did not reign supreme.”

In 2022, it was the end of the post-pandemic boom and buyers were rushing to get a home before mortgage rates climbed, so there was steep price appreciation in the first half of the year. But by June, prices peaked for the year while remaining below the June 2022 peak. Home sellers and listing agents know where demand is for homes.

Because each week we have 815% more sellers than last year, the total inventory will continue to build unless and until demand shifts dramatically, which would require notably lower mortgage rates. There are more sellers each week, and there are more sales, but the supply side is growing faster than demand. Those do not seem imminent.

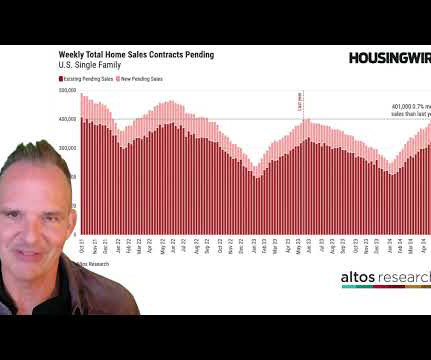

Weekly pending sales The Altos Research weekly pending contract data provides insights into real-time demand. Even today, the pending contract data remains resilient despite higher home prices and mortgage rates than last year. Last week saw 2% week-to-week growth but was down 1% year over year. Weekly inventory change (Nov.

This week, we count 14% more homes in the contract pending stage now than a year ago. When you include the 9,400 immediate sales, the total is 13% more sellers than a year ago. Last year at this time, the market was in deep retrenchment — both buyers and sellers were walking away. Sellers could dip again next week.

Additionally, our weekly pending contract data and new listings are trending positively compared to last year. Weekly total pending sales The latest weekly total pending contract data from Altos offers valuable insights into current trends in housing demand.

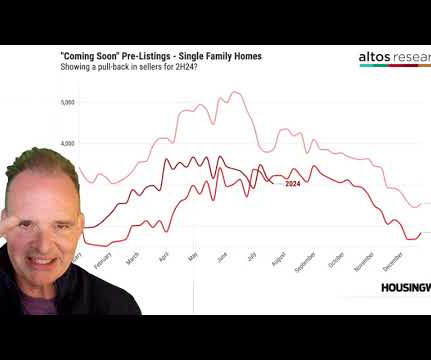

New listings move upward, but remain historically low Altos uses new real estate listings data as a key indicator of seller activity in the D.C New listings volume grows each year during the spring months, and this year seller rates appear to be accelerating faster than in recent years. housing market. As unemployment in D.C

That shortage reached its crisis peak in January 2022. Supply growth could also come from more sellers, such as investors or distressed borrowers unloading. However, in most of the country, we have no growth from the seller side. Weve been averaging about 8% more sellers each week than a year ago. is $384,900 now.

A History of Policy Change In mid-March of this year, NAR announced an agreement to resolve litigation over broker commission claims asserted on behalf of home sellers. Traditionally, sellers paid the buyer’s agent commission as well as their own agent’s commission.

It looks like we’re heading back to those conditions of the second half of 2022 where inventory grew rapidly, but any real downside correction was mitigated with a withdrawal of supply. Sellers can just wait it out, and it looks like the U.S. I think it’s worth examining if sellers will indeed just wait it out now.

In those times, we just had far more buyers than sellers. So lets take the opportunity to look at a slightly different view of seller volume. These are new listings that take offers within a couple days of listing and go into contract immediately. There are 260,000 single-family homes in contract right now. Thats only 2.3%

That is, theyre no longer listed for sale and theyre not in contract. When a home gets listed for sale in March, the seller and the listing agent use all the information about possible buyers and traffic to price that as most likely to sell. At the left end of the chart, thats 2021 and 2022. Something to watch. above last year.

As we approach the end of another hot year for the market, homebuyers and sellers are eagerly looking ahead to the 2022 housing market. Demand will continue to be strong into 2022. In a normal market, we tend to see about 30% to 35% of sellers initially over-price their homes and eventually reduce the price to attract buyers.

Now its pretty clear that sellers arent slashing asking prices and mortgage rates arent plummeting, so mindsets are shifting. Key findings from the four weeks ending January 26: Before the seller accepted an offer, the average U.S. Key findings from the four weeks ending January 26: Before the seller accepted an offer, the average U.S.

One of the reasons total inventory data hasn’t gotten back to 2019 levels is the lack of sellers in 2023 and 2024. Here are new listings for last week over the past several years: 2024: 62,876 2023: 57,229 2022: 59,458 Price-cut percentage In an average year, one-third of all homes take a price cut — this is standard housing activity.

Marty Green thinks of the housing market in 2022 as two very different movies. But the housing market in the second half of 2022? The number of home listings dried up , contracts were canceled , the few buyers still out there demanded concessions , mortgage rates spiked to 7% and homebuilder sentiment hit rock bottom.

New listings remain low as owners lock in Altos’s data for new listings accounts for single-family homes that come to market without an immediate or pending contract. New listings for single-family homes or condos are key indicators of seller behavior and new listings ramped up during the week of Feb. Whats the reason for this?

New listings hit the highest level since July 2022, increasing 1.9% of homes that went under contract last month. I have sellers saying, I think were at the top of the marketIm ready to cash out and put my money into another investment. Active listings of homes for sale rose to the highest level since early in the pandemic.

No one wants a scenario in which there’s a flood of sellers but no buyers. You can also see the light red line from 2022 when rates were first skyrocketing. Inventory in 2022 was building much more quickly than it is now. As previously mentioned, any signs of rising seller volume is helpful to this market.

New listings decline isn’t as steep as a year ago There were only 53,000 new listings (single-family homes) unsold this week, plus 10,000 more new listings that are already in contract. There are far fewer sellers now than in any recent year. However, last year’s seller decline was much more steep.

Under a lease-purchase arrangement, the property seller also acts as the landlord. The buyer rents the home as a tenant first, typically paying an up-front fee or down payment under an option contract to preserve the right to purchase the property within a set time period. Market Embraces Wave of Business Players About 2.4 million U.S.

These are the homes that go into contract immediately after listing. New listings dry up On the other hand, inventory can’t build too much if sellers don’t sell. There are some signals of seller volume drying up. Seller volume in 2024 had been slowly growing, and I viewed that as an optimistic trend.

New listings show 12% more sellers than a year ago When we look at the new supply hitting the market each week, we see the same trend we’ve had for a few months. There are more sellers than a year ago, but still not a lot of sellers. That’s 114,000 sellers vs. 87,000 now. We see that sellers are still restricted.

Beginning in January 2020, 7% of purchase transactions had a contract price above the appraisal value. Five months later, the frequency increased to 19%, leaving homebuyers to either pay more out of pocket or request the seller to lower their asking price. of homes are valued lower than the contract price. More Remote Contact.

We’re rapidly approaching the peak of the market in terms of seller listings, and as inventory builds, the sales rate will peak by the end of June. We are also consistently measuring more sellers coming back into the market. In fact, there are more new sellers this week than in any week of 2023. But we’re not close to that yet.

There are now 83% more homes on the market than in May 2022. More home sellers are coming back to the market each week. These are new listings that are already under contract, so they’re not counted in the active inventory. That makes a total seller count of 93,000 for the week, which is 20% more than last year at this time.

If you need to communicate about the real estate market with buyers and sellers, you should join us. It’s the peak season for buyers and sellers. Remember that, back in 2022, as mortgage rates were rising quickly, so too was inventory. There are more sellers now as rates have stayed higher for longer. That’s up 1.5%

As brokerages across the country have begun implementing buyer agency contracts into their business practices in the wake of the Sitzer/Burnett commission lawsuit verdict, the Consumer Federation of America is warning consumers that they may be filled with “unfair provisions” that primarily protect agents and brokers.

There were 58,000 new listings this week, with 10,000 of those homes already under contract as immediate sales. A few more sellers appear to be braving the market each week. We had 52,000 new pending sales this week. We had 52,000 new pending sales this week. That’s 5% more sales initiated than this time a year ago.

New home sales contracts are coming in pretty consistently fewer than last year — 4.9% Our Immediate sales measure of homes that get listed, take offers and go into contract in a few days is also notably lower than last year. There are fewer sellers than normal, and slightly more than last year, but the gap from last year is closing.

We have more homes going into contract each week now than we did a year ago — supply and demand are climbing together. That’s fewer than last week of course it’s the holidays, but it’s almost 5% more than where we ended 2022. Each week sellers are easing back into the market a little more than last year.

We’re rebounding inventory after the holiday, so it’s not that much of a surprise, and it’s less of a jump than what was happening at this time in 2022. There were another 15,000 new listings that are already in contract, which is very low for immediate sales recently. In fact, sellers seem to be pulling back.

The second dynamic to watch here is how many sellers are cutting their prices each week. It’s not as steep as 2022 — the market now is not shifting as quickly from big growth to price declines, like it did briefly about 18 months ago. That’s a pinch fewer sellers than last week, still 13% more sellers each week than a year ago.

I like to point out that consumers are more sensitive to changes in mortgage rates than to the absolute levels, and since rates are now basically unchanged for the month, just easing down from the early March peak of 7.2%, sellers and buyers are tip-toeing back into the market. More sellers means more sales will happen.

Mortgage spreads The spread between the 30-year mortgage rate and the 10-year yield has been an issue since 2022 and things got worse after the March 2023 banking crisis. If mortgage rates keep falling and demand picks up, we will have a much better buffer with active inventory than in 2022 and 2023.

How will homebuyers and sellers react and how quickly can we measure it? Available inventory of unsold homes on the market is 30% greater than last year at this time and 102% more than in mid-April 2022. In early 2022, inventory rose quickly and home prices fell in Q4 of that year. But the U.S. This concept is counter-intuitive.

The leading indicators for sales prices show that 2023 will end with home price gains of 1-2% over 2022, but the 2024 outlook is weakening and depends on your view of mortgage rates in Q1 and whether home prices will appreciate next year. Note the inventory climb is not from sellers. 5% fewer sellers each week than last year.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content