This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

According to a report produced by Douglas Elliman and real estate appraisal company Miller Samuel , single-family home listings sloped down 58% year-over-year in July 2021 to a paltry 20 total in the famous ski-resort town. Thirty-three condo contracts were entered in July and 20 were in the $2-$4 million range.

One difference between 2023 and 2024 is that this year the pending contract data shows small but steady year-over-year sales growth. I love that newlistings data is growing yearly, but it’s been too light for me. Our weekly tracking data is months ahead of the existing home sales report, so we always give readers a heads-up.

Newlistings each week, which were record few last year, are growing now. Newlistings volume climbing I want to start today with the newlistings volume, which is notably finally climbing over last year’s anemic levels. There were 66,000 newlistings this week, of which 14,000 are already in contract.

Weekly pending sales The latest weekly pending contract data from Altos Research offers valuable insights into current trends in housing demand. The last two years were the two lowest newlistings data years in history. 26 in Dallas. We are still showing higher growth versus 2023 levels but not by much.

This is a demand-driven slowdown, because newlistings supply is still running 9% to 10% fewer homes for sale each week than this time last year. We’re seeing fewer new sellers each week, but inventory is building as homebuyers wait to see if mortgage rates will come down to make purchases more affordable. from last week.

Home prices jump The median price of the homes that went into contract this week jumped to $389,900. It’s the second week in a row with an uptick in the price of the homes going into contract. Newlistings healthy There were 70,000 newlistings unsold for single-family homes this week.

Yes, home prices are still rising in 2024, but the pace is significantly slower than in 2020 and 2021. The seasonal decline in newlistings will begin soon and we will see if we get fewer sellers in the second half of the year than the current trend. So far the weekly high print in 2024 is only 72,329.

of homes that went under contract that month. month-over-month in December to a seasonally adjusted annual rate of 4,317,683the highest level reported since February 2023, and a 6% year-over-year jumpthe largest annual increase since July 2021. year-over-year, the largest annual gain reported since June 2021. a year earlier.

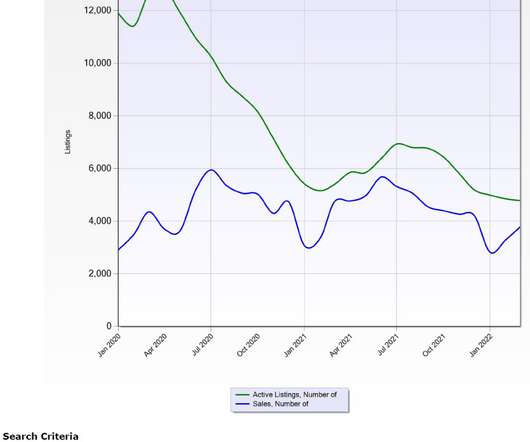

Inventory levels are also still higher than the COVID-19 inventory lows: In late February 2021, inventory levels sat at 2,414 single-family units. Newlistings remain low as owners lock in Altos’s data for newlistings accounts for single-family homes that come to market without an immediate or pending contract.

observed in 2021 and are seeing below-trend growth over the history of the index,” said Brian Luke of S&P Dow Jones Indices. New York City continued to demonstrate strength in home prices, up 7.2% National home prices have risen by 8.8% year over year in December. Home prices reached an all-time high in Boston after a 6.6%

of homes that went under contract that month, according to a new report from Redfin. NewListings Tick Up Slightly, But Overall Housing Supply Remains at Record Low Newlistings rose 0.8% Year-over-year newlistings were down 14.4%. Newlistings have likely bottomed out,” she said.

During that period, we saw newlisting data decline. However, in 2020 newlisting data came back, and we don’t want to see the newlistings continue to decline this year — that would be a double negative for the housing market. from December 2021 ($358,800), as prices rose in all regions.

As part of “team higher rates” in 2021 and 2022, this is precisely what I wanted to see happen because we can’t assume mortgage rates will stay elevated in the 7%-8% range. 2024 is the second-lowest newlisting year recorded in history. Weekly inventory change (Aug.

It was at this point in 2022 when newlistings started plummeting each week. In September, even though new sellers were few, buyers were even fewer, so inventory rose. Through July, newlistings volume each week was in the normal range as in previous years. Suddenly newlistings volume dropped each week.

With the home-price growth we had in 2020 and 2021, my five-year price-growth model that I set for 2020-2024 of 23% was already smashed in just two years. That was a huge red flag, hence all the statements in 2021 about unhealthy housing. . From NAR Research : “Total existing-home sales notched a minor contraction of 0.4%

Active inventory fell 1,109, and newlisting data made a lovely comeback week to week but was still noticeably down year over year. One piece of good news last week was that the newlisting data, which saw a significant collapse two weeks ago, rebounded excellently to return to a usual trend.

More than half of homes (51%) have sold above their listing price in the four week period ending May 23, 2021 — up from 26% one year ago, according to a recent study by Redfin. Diving deeper, for the two week period ending May 9, 2021, 57% of homes that went under contract had an accepted offer within the first two weeks on the market.

Newlistings volume is trying to grow with its biggest week since September. List prices inched up for the week, though sales prices did not advance. We calculate that while there were 63,000 newly pending single-family home sales in the week, there were another 20,000 withdrawn listings across the country.

One-third of homes that went under contract had an accepted offer within one week of hitting the market, a new report from Redfin found. In addition, the number of homes that went under contract within two weeks of listing rose to 46% from 42% during the same period in 2020. points from a month earlier.

There are no signs of any surge in listings, and as a result we’ve seen a floor on home prices. Newcontracts dipped as affordability is out of reach for so many. There are 348,000 single-family homes in contract right now, with only 54,000 newcontracts pending in the last week.

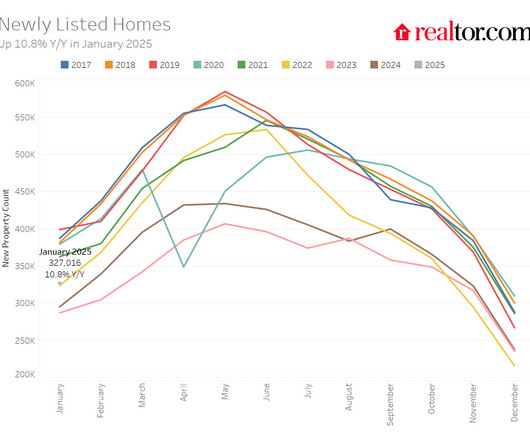

The number of newly listed houses was 10.8% This puts the number of newlistings at its highest January level since 2021 and indicates that sellers are becoming more interested in the market. Active listings +25.3% -25.3% Newlistings +10.8% -18.0% percentage points Median list price per sq.

“I never know how my day is going to go, because when a newlisting comes on the market in Knoxville, the race is on. You set your appointments the night before, and when you get there that morning, they might already be under contract.” Generally, they go under contract in a day or two.”

Pending Sales There are now 378,000 single-family homes in contract. There were 68,000 newcontracts for single-family homes this week. In the chart below, the light portion of each bar represents the newcontracts each week. But, there were another 15,000 condos and townhomes that went into contract this week.

“But if the pandemic surges up again, I think we’re just going to get busier and busier here, because we are definitely located in the correct position, outside of New York City, where parents can still commute to work and children can have space needed for homeschooling and things like that,” Kanacki said.

HouseCanary’s latest Market Pulse report, covering 22 listing-derived metrics and comparing data between July 2020 and July 2021, has found that the while the nation’s housing supply remains a detriment for the market, net newlistings and the number of listings under contract shrinking is a positive sign that is rectifying itself.

The median price of the newlistings this week is $399,900. As the summer progresses, each subsequent week of newlistings gets priced at a slight discount to the previous weeks. The median price of the homes in contract is $385,000. There are now 376,000 single-family homes in contract.

While only one West Coast market, which led the way in 2021, made it into the top 10, the Midwest also performed well. Adding to the price pressure, newlistings can remain sparse in the hottest spots as existing owners continue to hold on and hold back.

See how the tan line of 2021 peaked right about on the same curve we’re seeing this year? If we look at the transaction rate each week — the total number of newcontracts for homes — you can see that in the first half of the year, the pace of sales was steadily returning to normal. At Altos , we don’t predict mortgage rates.

in 2021, Freddie Mac reports. trillion in 2021,” the agency’s quarterly forecast states. New York — Housing markets have been mixed since the last report, with the rental market continuing to strengthen but the sales market weakening noticeably. Freddie Mac projects that home-price growth will average 12.8%

New findings from the National Association of Realtors (NAR) show a fresh picture of who’s buying and selling homes, with more first-time buyers entering the market and families looking for homes that fit multiple generations. They send out updates on newlistings that line up with what buyers are looking for — all on autopilot.

The number of newlistings has decreased but so has the number of pending sales, which means that inventory is lingering longer than it has been which is a positive sign for buyers. Sales are down 5 percent year over year with September 2021 at 9,150 over 9,631 last September. 2021 – 10,451 2020 – 11,210 2019 – 10,950.

The chart (below) puts it in sharp focus: Except for the pandemic year of 2020 when there were 2559 newlistings that April, last month was the slowest April since at least 2008 when easy access to Northwest Multiple Listing Service data became available. Where are all the sellers? You can’t buy what’s not for sale! There are 1.7

Traditionally, the months of May and June see the most newlistings as the school cycle hits – graduating families sell and rising families buy. The charts below focus on key indicators; number of listings, number of sales, days on market and sale to list ratio. Low but it was running around 5 days in mid-2021.

The amount of home sales in 2021 was down by 43 sales, 0.3% There were 14,946 sales in 2021 compared to 14,989 in 2020. Broken down, single-family sales are the only category that decreased in 2021, down by 4%. Broken down, single-family sales are the only category that decreased in 2021, down by 4%. Sales Down 0.3%

In this 2021 Mid-Year Housing Report, we’re looking at home sales in the first half of 2021 compared to the first half of 2020 and how the market performed in that area. Home sales more than doubled as of June 30, 2021, with an 85.1% Listings increased by 22.7% 2021 Outlook. Pending Homes.

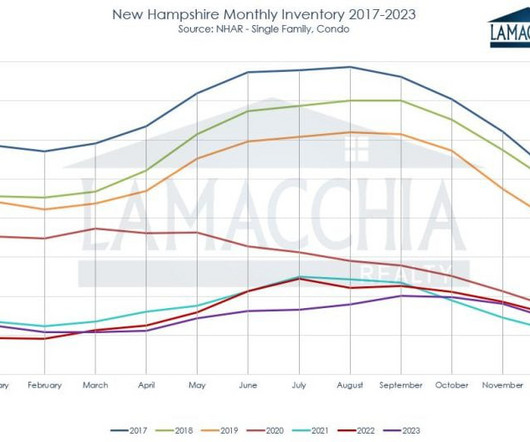

Single families: $481,694 (2023) | $498,107 (2024) Condominiums: $520,070 (2023) | $508,628 (2024) Multi-families: $507,495 (2023) | $437,002 (2024) Homes Listed For Sale: T he number of homes listed is up by 2.2% 2024: 2,551 2023: 2,495 2022: 2,428 Pending Home Sales: The number of homes placed under contract is down by 20.8%

In 2021 , we saw houses receive multiple offers and sell for thousands of dollars over asking price within hours. Buyers and sellers can be in completely different parts of the world and still access their contracts at any time! No printing, scanning, or faxing needed. We know the feeling.

Single families: $565,508 (2023) | $601,939 (2024) Condominiums: $316,487 (2023) | $377,514 (2024) Homes Listed For Sale: T he number of homes listed is up by 8.2% when compared to September 2023. 2024: 3,922 2023: 3,624 2022: 4,027 Pending Home Sales: The number of homes placed under contract is up by 0.3%

Single families: $604,300 (2023) | $677,400 (2024) Condominiums: $515,242 (2023) | $508,017 (2024) Multi-families: $468,463 (2023) | $610,896 (2024) Homes Listed For Sale: T he number of homes listed is up by 21.0% 2024: 1,553 2023: 1,283 2022: 1,495 Pending Home Sales: The number of homes placed under contract is up by 11.2%

Single families: $552,142 (2023) | $616,575 (2024) Condominiums: $319,672 (2023) | $361,324 (2024) Homes Listed For Sale: T he number of homes listed is down by 1.4% 2024: 1,633 2023: 1,657 2022: 1,682 Pending Home Sales: The number of homes placed under contract is up by 9.0% when compared to December 2023.

Newlistings and pending sales are also down year over year as many sellers are hesitating to put their homes on the market, so less homes are being placed under contract and inevitably less homes are closing. The average price slightly increased for single-family homes and decreased for condos and townhomes.

Single families: $707,730 (2023) | $738,731(2024) Condominiums: $626,077 (2023) | $643,949 (2024) Multi-families: $707,288 (2023) | $747,450 (2024) Homes Listed For Sale: T he number of homes listed is up by 17.0% 2024: 8,579 2023: 7,330 2022: 8,372 Pending Home Sales: The number of homes placed under contract is up by 12.2%

Single families: $541,3636 (2023) | $624,255 (2024) Condominiums: $454,535 (2023) | $512,872 (2024) Multi-families: $475,035 (2023) | $598,944 (2024) Homes Listed For Sale: T he number of homes listed is down by 0.6% 2024: 772 2023: 777 2022: 787 Pending Home Sales: The number of homes placed under contract is up by 0.9%

The 2022 slowdown was a welcome break from the unsustainable frenzy of 2021 , and 2023 continued the trend towards balance, albeit with some challenges. Lowest number homes listed in recorded history, decreased by 15.1% Lowest number homes listed in recorded history, decreased by 15.1%

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content