This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Zillow has found that Hispanic homeowners are making great strides in narrowing the homevalue gap with white homeowners over the past two years—regaining ground lost during the pandemic. Hispanic-owned homes are currently worth 11.9% less than homes owned by non-Hispanic white households, down from 12.1% from 17.9%.

A Zillow report released Thursday shows urban homevalues in Midwest cities — namely, St. Louis, Cincinnati, Cleveland, Kansas City, Columbus and Indianapolis — have risen faster than suburban homevalues over the past several months. Today, both sellers and buyers expect to handle a majority of the process online.

Now, soaring premiums demand more careful review and sticker shock is prompting buyers to walk away from deals, especially in states like Florida and Texas. In California, where more than 7,000 wildfires occurred last year, the typical homeowner in many ZIP codes paid premiums as low as 0.05% of homevalue, according to the Times.

A new LendingTree study found that mobile homes are cheaper and their values appreciated almost as quickly as single-family homes over five years, from 2016 to 2021. On the other hand, median single-family homevalues increased by almost a similar average of 35.44% for the same time period.

And now, with the COVID-19 vaccine circulating and the economy slowly regaining strength, Zillow researchers say millions of additional households could enter the housing market in 2021. “The pandemic has catalyzed purchases by millennial first-time buyers, many of whom can now work from anywhere.”

What should be the most competitive markets for buyers this year share two characteristics: relative affordability and a dearth of available homes. Construction that keeps pace with an areas growth remains a crucial piece of keeping homes available and accessible. Thats the good news. 13 position this year.

Zillow’s 2021 housing forecast echoes the projections of other industry experts of a rapid acceleration of homevalue appreciation, with numbers anticipated to be even higher than in 2020. According to Zillow’s HomeValue Index, the company expects seasonally adjusted homevalues to increase by 3.7%

Lock-in Effect Moderates as Buyers Adjust to Elevated Rates The lock-in effect has discouraged homeowners from listing their homes for sale, which has contributed to Americas acute housing scarcity. in Q1 2022 and the lowest share since Q2 2021. have a rate below 3%, the lowest share since Q2 2021. in the middle of 2022.

Even though we may be a long way from rates returning to the 23% range we saw at the end of 2021, its still great to see things trending in the right direction. Your monthly house payment on a 15-year fixed-rate mortgage will be 25% or less of your monthly take-home pay. But 510% is okay, too, if youre a first-time homebuyer.

While only one West Coast market, which led the way in 2021, made it into the top 10, the Midwest also performed well. cities, such as page-view traffic, homevalue increase, and the speed at which properties sell, in order to identify the most popular markets in 2024. As a result, average homevalues have increased by 7.3%

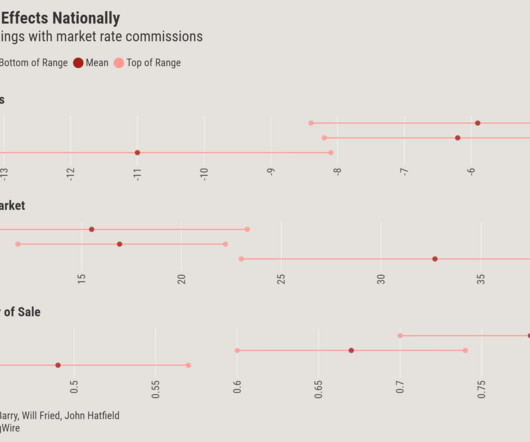

Three researchers believe a first-of-its-kind dataset has enabled them to definitively answer a long-debated question: why have buyer agent commission rates been so stable historically? So how is the uniformity and permanence of buyer agents’ 2-3% rate possible in a free market? One of the researchers, Will Fried, had a hunch.

As work-from-home becomes more of a national norm, prospective homebuyers are seeking better homevalues in small towns that still offer a lot of amenities. Per Realtor.com , homes are being sold at an average of $111,000 in Bay City, and the average listing price per square foot is only $75. compared to 2020.

“If somebody is concerned about that (taxes), I always put it back on the buyer and ask them, ‘Do you have any control in the increase of your rent payment?’” single-family home was $3,901, up 3% compared to 2021, ATTOM reported. But homevalues and taxes have shot up in several neighborhoods.

Zillow also announced it has agreed to pay $500 million to acquire ShowingTime , which makes software for prospective buyers to arrange showings with agents. The Seattle-based company , which has mostly pivoted from selling advertising to real estate agents into iBuying, acquired 1,789 homes in the fourth quarter. million – up 25.8%

As the first quarter of 2021 nears its end, a recent Redfin report shows both good and bad news for Black homeowners. The positive: Homeowners in primarily Black neighborhoods earned an average of $59,000 in home equity in 2020, compared with $50,000 for homeowners in primarily white neighborhoods between 2019 through January 2021.

Skyrocketing mortgage rates – now in the 7% range for some buyers – and limited inventory have driven mortgage affordability to its lowest levels since the early 1980s, a reversal from the frenetic boom in buying during 2020 and 2021. That monthly payment is up $930 from August 2021, a 73% increase. With mortgage rates at 6.7%

From 2009 to 2019, the share of recent buyers who are 60 years and old grew 47% , while the share of recent buyers ages 18-39 fell by 13%. From 2009 to 2019, the share of recent buyers who are 60 years and old grew 47% , while the share of recent buyers ages 18-39 fell by 13%.

Even during a period when homevalues are typically at their lowest, many prospective first-time buyers were unable to reach their long-term financial goal of becoming homeowners in Q1, according to the Q1 2024 First-Time HomeBuyer Affordability Report from Nerdwallet. Cleveland (3.0) Buffalo, NY (3.2)

The average 30-year fixed rate mortgage rate was its lowest ever at 2.65% on December 31, 2021. Assuming a $250,000 loan was committed on December 31, 2021, your monthly payment was approximately $1,007 exclusive of escrow for real estate taxes and insurance. Therefore, it begs the question: what will happen to homevalues?

Quickly rising mortgage rates are compounding affordability challenges that have been brought on by record homevalue growth. home is now 19.5% Despite this, the pace and volume of sales picked up in March, showing the depth of the pool of homebuyers willing and able to meet.

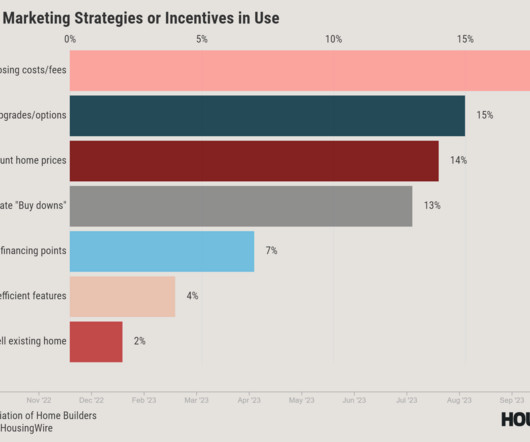

The Western pessimism is also unsurprising given the year-over-year declines Western states have seen in homevalues. Builders reported covering closing costs, offering discounted or free features, helping buyers sell their existing home and providing other incentives. 2019 level.

The agent said rich “mainland” residents replaced international buyers, who are restricted in their travel amid the pandemic. That’s reflected in home prices, where the median Honolulu home sold for $975,000 in the second quarter of 2021, according to the National Association of Realtors , a climb of 20% year-over-year.

At the end of February, an estimated 407,000 new homes were still for sale, which at the current sales rate represents a 6.3 from a month prior and a 40% increase from the February 2021 level. Buyers are facing a housing market that looks to be as competitive as ever,” Handy said in a statement. months supply. after a 10.4%

months in October 2021. Inventory levels are still tight, which is why some homes for sale are still receiving multiple offers,” Yun said. “In In October, 24% of homes received over the asking price. Conversely, homes sitting on the market for more than 120 days saw prices reduced by an average of 15.8%.”. ” .”

For the first time in a year, the number of buyers who locked in mortgage rates to purchase a second home fell in June. Per a recent Redfin study , second home mortgages saw a year-over-year decrease of 11.1%. Home prices in seasonal towns, meanwhile, rose 28% year over year to $468,000 in June.

New data from LendingTree and CoreLogic highlights the struggles and successes of young buyers in todays real estate landscape. Young buyers still face an uphill battle According to a LendingTree analysis of anonymized credit reports, only 3.1 % of Americans under 30 currently hold a mortgage in the nations 50 largest metro areas.

That’s a problem when a typical Colorado home – as defined by Zillow ‘s HomeValue Index – costs more than $528,000. When teachers can’t afford to buy homes, school districts can’t hire teachers. Other districts have adopted the same approach.

A combination of fast-rising homevalues and the fact that nearly two-thirds of borrowers with at least some home equity have mortgage rates below 4% — and would not benefit from refinancing — is helping to propel a resurgent market for home-equity lines of credit (HELOCs). billion in 2021 to $4.6

For many buyers, closing day represents the beginning of the next chapter in their lives – having a new place to celebrate important milestones and create new memories. Unfortunately, as buyers are preparing for this momentous day, wire fraud – a scam in which cybercriminals attempt to steal buyers’ hard-earned money – poses a serious threat.

After blowing past the 2% core inflation target in April 2021, it continuously rose for 18 months until peaking in September 2022. We can also expect low housing demand, which favors buyers. Since the COVID-19 pandemic lockdowns of 2020, inventory has dropped to record-low levels both in 2021 and 2022. It did not hit 6.7%

Annual house price growth hit a record high in 2021, over 17%, and growth remains in the double digits thus far in 2022. Homes that reach the market sell quickly, bidding wars are the new normal and the investor share of sales continues to rise. To register for the HW+ event, go here.

The good news for homeowners is that homevalues in most areas remain stable, and inventory levels for homebuyers are still low. How has the foreclosure-related regulatory landscape changed since 2020 and 2021? By September 2021, however, there was still much foreclosure reluctance.

In many ways it was similar to today, with one exception: When I started, I hadn’t been spoiled by a housing market like the one in 2020 and 2021. It boxed out many first-time homebuyers who found themselves unable to compete against buyers willing to place a non-contingent offer above full price.

This is the first decline in home prices in almost three years, down from 57.6% in the second quarter, with median national homevalues dropping 3% quarterly to approximately $340,000, the report said. Despite this drop, investment returns for home sellers is still up from 48.8% of sales in Q3 of 2021.

percentage points) Median List Price Per Sq.Ft. : (+2.3 %) (+50.8 %) “Lock-in” Effect Causing Buyers to Stay Put The real estate market has been hampered by the “lock-in” effect for many years now, whereby homeowners, who are tied into a relatively cheap mortgage rate, have been remaining there, having a negative influence on available inventory.

Our forecast is for homevalues to rise 16% from December 2021 to December 2022. One of the main headwinds for buyers — higher mortgage rates — will also dissuade some sellers who want to avoid paying more interest on their next home purchase. Zillow’s answer: price growth won’t slow much, at least not nationally.

Affordability concerns were also reflected in USMI’s 2021 National Homeownership Market Survey, which reported that 69% of Americans say lack of affordable housing is the biggest homebuying challenge. Buyer morale is at an all-time low for good reason. points year-over-year with only 24% of consumers saying now is a good time to buy.

home purchases fell 1.9% during the same period, which Redfin attributed to elevated mortgage rates and home prices. While investors are still sensitive to mortgage rate changes, they are less sensitive than consumer buyers as 69% of investors pay in cash. In comparison, total U.S. metro areas going back to 2000.

Fewer buyers rushed to lock mortgages last month amid a rapid climb in long-term mortgage rates , reflecting home affordability concerns, reports from Mortgage Capital Trading and Black Knight showed. . Compared with April 2021, rate-and-term refinances were down 89.2%. in April from the previous month. from a year earlier.

For a homevalued at $250,000, the cost of an owner’s title insurance policy would be just 11 cents a day on a 30-year mortgage. nationally since 2004 and roughly 5% the past two years, based on the most recent industry data from 2021. Recently, an attorney shared with me how one of her clients purchased a home in Connecticut.

In November 2024, national home sales climbed 6.1% compared to a year ago , marking the biggest year-over-year gain since June 2021. Despite this trend, South Florida saw a decrease in home sales. The decline in overall sales and pending transactions suggests a slowdown in buyer demand. by month’s end.

This surge follows a period of fluctuating investor activity during the COVID-19 pandemic, where purchases more than doubled during the 2021 homebuying boom, only to drop nearly 50% in 2023 due to declining rents and homevalues. Despite the renewed investor interest, overall home purchases in the U.S.

Interest rates, though down slightly in recent weeks, are still double what they were at the end of 2021, and the Federal Reserve continues its monetary tightening policies to fight inflation. Nobody was doing buydowns in 2020 and 2021 [when 30-year fixed mortgage rates were in the 3% range]. in November, down from a 9.2%

The decline in total sales and pending homes suggests that buyer demand may be weakening. As a result, more sellers have entered the market, but many buyers now find these properties to be outside their budget. Instant Home Evaluation See immediately how this market is impacting your homevalue.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content