This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Weaker demand from the local community developers buying at auction suggests continued weakness in the retail housingmarket into early 2025 given that those local community developers are anticipating retail market conditions about six months into the future,” Daren Blomquist, vice president of market economics at Auction.com, said in a statement.

Dramatic mortgage rate movements are destined to play a major role in the coming year, according to Zillow ‘s newest forecast , which also calls for declining mortgage rates to be a catalyst for home-sales growth and home-price appreciation in 2025. “There’s a strong sense of dj vu on tap for 2025. million in 2025.

Weve now been in the post-pandemic housingmarket recession market as long as we were in the pandemic boom. Does the housingmarket start to get back to normal? The number of unsold homes on the market is finally getting closer to 2019 levels. The MBAs mortgage applications data has been surprisingly strong.

The housingmarket in 2024 was about as frustrating for the real estate industry as you can imagine. And its a higher number than at any point since the financial crisis, other than 2020 and 2021 during the post-pandemic boom. This is particularly true for builders with in-housemortgage businesses. million.

housingmarket slowed down in the third quarter due to rising home prices and higher mortgage rates , investor purchases also ramped down, according to a new report by Redfin. a year earlier and the lowest share since the end of 2020. in Q1 2022, when investors were taking advantage of low mortgage rates.

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? Now, with five weeks of data in front of us, we can say they have stabilized the market. Mortgage rates went from a low of 2.5%

The housingmarket experienced more volatility last week, with housing inventory dropping as mortgage rates moved higher. The start of 2023 has been good, considering mortgage rates have stayed above 6% most of the time. I am keeping an eye on how much growth we can get with mortgage rates over 6%.

However, if home prices hadn’t skyrocketed alongside mortgage rates , we would have more younger homebuyers entering the market and we would have a slightly higher homeownership rate than todays 65.7% My housing economic model started in 2010 and I separated my work into two different timelines. in Q2 of 2016.

Fluctuating interest rates have been a feature of the housingmarket over the last three years. As mortgage rates rose, homebuyer demand slowed and inventory grew. In 2025, mortgage rates have stayed stubbornly high for yet another spring buying season. Today, home sales still remain super slow. Is it economic vibes?

In a housingmarket shaped by uncertainty, military veterans and service members are emerging as some of the most confident and prepared homebuyers, outpacing their civilian counterparts. This was driven by optimism about the housingmarket and economy. But with mortgage rates climbing back above 6.5%

You can see why I have been on team higher mortgage rates for some time now because we don’t have any other way to get off this madness. Total inventory data is deficient, and this was my biggest fear in the years 2020-2024, and it happened. Housing is the cost of shelter to own the debt; it’s not an investment.

The recent surge in immigration to the United States has ignited discussions about its potential effects on the housingmarket, particularly concerning housing costs. Senior Research Analyst Riordan Frost from the Harvard Joint Center for Housing Studies, recently took a deeper dive into the impact of immigration on the U.S.

I have been part of the mortgage banking industry since 1983 — 39 years to date through different housingmarkets. So when I talk to loan originators today, I harken back to my early days when fixed mortgage rates were over 14% and there were absolutely no refinances to be had. Things will get better.

They say housing leads the economy in and out of a recession. Currently, housing starts are back at the levels seen during the COVID-19 recession in 2020. Perhaps most importantly, some homebuilders have been subsidizing mortgage rates to help maintain employment and finish ongoing projects.

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. Housing permits and starts are falling now, even with the backlog of homes in the system. With less transaction volume , general incomes in the housing sector are falling.

Now that we are almost in July, we can safely say the premise that once mortgage rates hit 4%, the mass panic selling of American homeowners who need to get out at all costs, driving total inventory up in the millions, hasn’t happened. Now that mortgage rates have risen, demand is getting hit, while we are still showing 14.8%

The 2022 housingmarket was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Mortgage rates. Home price s.

million , with double-digit home-price growth driving a housingmarket that is still savagely unhealthy. However, this year has seen one big game-changer: the 10-year yield finally cracked over 1.94%, which drove mortgage rates over 4%. The real story in housing has been the price boom that we have seen since 2020.

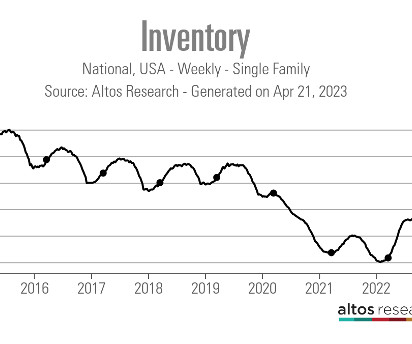

Can we now say that the housingmarket ‘s spring selling season is finally underway? Since 2020, the seasonal bottom for housing inventory has arrived several months later than normal, making it more complicated to track housing inventory data.

Last year saw the softest home-price growth in more than 10 years, according to an analysis by ICE Mortgage Technology. Despite that and other positives, the LA wildfires are still making an impact on the housingmarket at the local and national levels. National mortgage delinquency rates sit below pre-pandemic levels.

housingmarket and that they need to be pro-housing again. Even with all the drama we have dealt with in 2022-2023, the housingmarket stayed intact and never broke. However, one thing is sure: from 2020 to 2023 we never saw credit-stressed home sellers. Weekly inventory change : (Dec.15-22)

The days on market are back to a teenager level in the existing home sales market, which means I can officially say we are back to a savagely unhealthy housingmarket! Nothing good happens in the housingmarket when the days on market are at a teenager level or lower. million in May.

Here’s the housingmarket rundown for the last week: Purchase application data had a solid week-to-week gain of 25%. Housing inventory decreased by 566 units, which is not a significant decline. Mortgage rates fell, but the bond market didn’t break what I see as a critical level, so for now, stabilization is more important.

But in light of Redfins blockbuster sale to Rocket Mortgage that was announced less than two weeks later, hindsight dictates that Kelman may have known that the end of independence was coming for the company hes run for almost 20 years. economy, the housingmarket ceased to function when the COVID-19 pandemic began in March 2020.

Just when I thought days on market were returning to normal, that number for existing homes fell back down to 22 days. If the days on the market are at a teenager level or even lower, it’s never a good sign for the housingmarket. This is why the days on the market are so low historically after 2020.

The housingmarket saw inventory fall 4% last week from the week before. Traditionally, we do see housing inventory fall in the month of December, however, we clearly saw in the second half of 2022 that higher rates created more days on the market and inventory was lingering longer. That’s a big one-week change.

Marty Green thinks of the housingmarket in 2022 as two very different movies. The first half of the year, with mortgage rates in the 3s and 4s, was like “Fast and Furious.” ” Houses were selling at a fever pitch in a matter of days, with multiple offers, waived contingencies and buyers paying $100,000(!)

Do rising mortgage rates necessarily trigger an economic recession or vice versa? With six of 10 distinct housing recessions since the 1970s preceding an economic recession (as determined by the National Bureau of Economic Research Business), it is tempting to answer, “yes.” A housing recession does not necessarily kick things off.”

This is the lowest monthly jobs number since employment fell in December 2020,” Lisa Sturtevant, chief economist at Bright MLS , said in a statement. Mike Fratantoni, chief economist for the Mortgage Bankers Association , noted that while mass layoffs have not occurred, the pace of hiring has slowed in recent months.

The spring housingmarket music is playing, and purchase application data and active listing inventory rose together last week. The other focus should be where mortgage rates go; only a little happened last week. Since 2020, the seasonal inventory bump has happened later than usual — not until March or April.

After heating up like the rest of the country, the Louisiana housingmarket has continued to cool since interest rates began to rise in the second half of 2022. Across the state, agents feel these rising insurance costs on top of higher mortgage rates and list prices. recorded in mid-February 2020.

Like the vast majority of the country, the city’s housingmarket has been stymied by high mortgage rates, low inventory and mismatched expectations between buyers and sellers. From March 2020 to July 2022, the median home price rose 23% before hitting a brief lull. 25 statewide in 2023 transaction volume.

It will get worse for the housingmarket – and mortgage industry – before it gets better. The latest forecast also projects total mortgage origination activity at $2.47 The latest forecast also projects total mortgage origination activity at $2.47 trillion in 2022, down from $4.47 trillion in 2021.

We created the weekly HousingMarket Tracker because housing data has been so wild since 2020. The housingmarket madness persisted last week as inventory fell and higher mortgage rates took a bigger bite out of purchase application data. Weekly inventory change (Feb.

Despite mortgage rates briefly falling below the 6% threshold, both housing inventory and mortgage demand fell last week. Let’s dive into the trend lines of the housingmarket. The show-me part of the housingmarket starts with this bounce from an extreme bottom. Weekly inventory change (Jan.

Here’s the housingmarket rundown for the last week: Purchase application data showed positive weekly growth again — and the bounce from the bottom is more noticeable now. Housing inventory decreased by 6,468 units, a more pronounced decline from the previous week. And, so far, it’s been a good start to the year.

annually since 2020 , led by markets in Florida, North Carolina, Southern California, and Arizona. Home prices stalled during the second half of the year with markets in the West dropping the fastest. San Francisco , the lowest-performing major market since 2020, saw prices drop by 4.5% Home prices were up 3.9%

The housingmarket faced some serious obstacles last week as the 10-year yield broke over 4%, mortgage rates rose to over 7%, purchase apps fell again and we are still trying to find the elusive seasonal bottom for housing inventory. What can bring mortgage rates down, even below 5.75%? 1 song of the year.

Auction.com has released its 2025 Distressed Market Outlook , which forecasts foreclosure auction volume decreasing 8% in 2025 as a baseline scenario. The forecast also incorporates two other less likely scenarios with differing macroeconomic and housingmarket assumptions.

The June housing starts data beat estimates with positive revisions, however, this doesn’t change the housingmarket recession call that I made last month. The smart thing to do is go with the builder sentiment trend until it reverses, and most likely, we will need to see lower mortgage rates for that to happen.

New home sales arent crashing anymore New home sales peaked in October of 2020 with 1,031,000 new home sales and then in 2022 that number crashed all the way down to 519,000 by June. However, after that decline and when mortgage rates started to fall late in 2022 home sales rebounded all the way back to 741,0000.

To that end, Veterans United Home Loans conducted a study to find which housingmarkets are best for current and former military members in these two generations. It concluded that the most favorable markets are on the East Coast and in the Midwest. The city that topped the list is Tampa. and the quality of life score ranks No.

We had a lot of drama over the week between Federal Reserve meetings and banking stress, and mortgage rates and purchase applications both fell. Mortgage rates fell last week as we started the week at 6.73%, got as low as 6.43% to end the week at 6.5%. Mortgage rates fell to a low of 6.43% then ended the week at 6.5%.

This article is part of our 2022-23 HousingMarket Forecast series. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the top predictions for this year, along with a roundtable discussion on how these insights apply to your business. months nationally.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content