This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

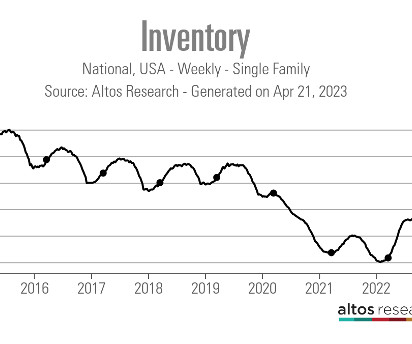

Housing inventory, which saw an excellent pickup a few weeks ago, has been slowing down and last week we saw a slight decline. Has seasonality finally kicked in or did back-to-back hurricanes slow things enough to influence inventory data? Since then, inventory growth has been slowing down and even declined last week.

Mortgage rates recently hit a year-to-date low, coinciding with ongoing market disruptions from tariffs. In fact, if mortgage rates head toward 6%, we will have a positive year here. Last year, we saw mortgage rates increase from 6.63% to about 7.50%, leading to challenges in the purchase application data.

Earlier this year, when mortgage rates soared to 7.26%, a cloud of worry hung over the housing market many feared that home sales would tumble in 2025, fueled by concerns about inflation and tariffs. But when it seemed doom and gloom would prevail, the 10-year yield dropped, pulling mortgage rates lower in a lovely slow dance.

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. Initially, the data showed more robust performance as mortgage rates approached 6%.

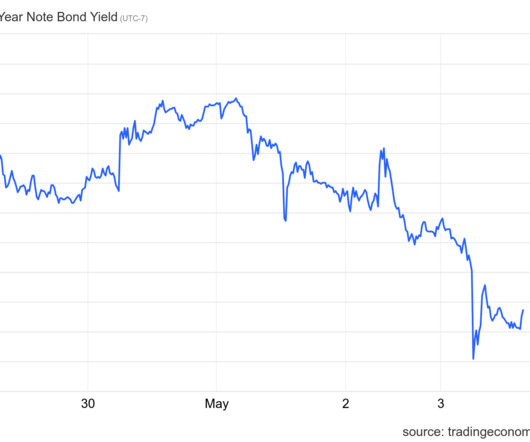

Another jobs week has come to an end, and amid the chaotic headlines about job numbers, tariffs , and the leadership of the Treasury , mortgage rates remained calm. Better mortgage spreads are limiting how high rates can rise in 2025. Mortgage spreads refer to the difference between the 10-year yield and the 30-year mortgage rate.

Will inventory levels skyrocket as federal workers leave? Weekly housing inventory ramps up What do we see in the data on housing inventory levels in the D.C. Weekly housing inventory ramps up What do we see in the data on housing inventory levels in the D.C. But inventory remains well below historical averages.

Mortgage rates are declining, and recent purchase application data shows a promising 9% week-to-week increase and a 2% rise compared to the previous year. I’ve noticed that housing data tends to improve when mortgage rates drop from 6.64% to 6%, especially when I adjust for seasonal demand.

If this happens, will we see lower mortgage rates this spring? However, last week saw a decline in mortgage rates due to softer economic data, which led to an influx of money into the bond market as stocks sold off on Friday. If we were experiencing the worst mortgage spreads of 2023, mortgage rates would be 0.77% higher today.

Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025. However, this year, mortgage rates rose during this timeframe.

Have we seen the peak in housing inventory for 2024? The best part about 2024 has been that higher mortgage rates have created an inventory buffer, so if the economy gets softer and rates fall, we have many more homes to work with than we had in 2020-2023. Weekly inventory change (Aug. Weekly inventory change (Aug.

The mortgage rate lockdown premise holds that very few people will list their homes when mortgage rates are this high, thus suppressing inventory. 2024 has had healthy inventory growth despite mortgage rates above 7%. Each time, inventory has squared right into the model as long as rates stay elevated.

Have lower mortgage rates already started to slow down housing inventory? I have a simple weekly growth model with the Altos inventory data: when rates are high, over 7.25%, inventory should grow between 11,000-17,000 weekly. Still, I would consider the last month of inventory growth healthy.

My model for inventory growth with higher mortgage rates came crashing down last week. After two weeks of significant increases , inventory growth slowed dramatically and is far from my 11,000-17,000 growth model with mortgage rates over 7.25%. When mortgage rates increase, demand falls and the price-cut percentage grows.

Lower mortgage rates tend to take housing supply off the market and demand has been picking up lately as rates have fallen. However, the recent drop in housing inventory has more to do with seasonality factors than lower mortgage rates. Mortgage rates and the 10-year yield The 10-year yield ended the week roughly flat.

31, 2022, that mortgage rates would hit 8% in 2023, you would reasonably assume housing inventory would sky rocket higher, home prices would fall noticeably, and the number of price cuts would be higher year over year. Last year, the seasonal peak for inventory was Oct. Weekly inventory change (Oct.

The mortgage rate lockdown premise says that if rates rise, inventory can’t grow meaningfully. The idea is that nobody will trade their low mortgage rates to buy another home — even though this happened every week last year. With mortgage rates higher, will this stop inventory from growing year over year?

Housing inventory, new listing data and mortgage rates are all rising, but the price cut data percentages are falling. I will watch for rising mortgage rates to see if they change the weekly data. I will watch for rising mortgage rates to see if they change the weekly data. So far, so good in 2024.

Active weekly housing inventory growth slowed slightly last week, but it’s still running at a healthier clip than in 2023. I have a simple model with mortgage rates being above 7.25%: weekly inventory data should grow between 11,000-17,000 per week. We have now seen it for two weeks as inventory grew by 13,247.

How will mortgage rates impact seasonal inventory in 2024? In the last four years, we have had abnormal seasonal inventory data, meaning that the spring inventory bottom happens later in the year. Also, when mortgage rates rise, the inventory peak happens later in the year.

Housing inventory finally hit my target level of growth last week with mortgage rates now over 7.25% , something I couldn’t get all last year. Weekly housing inventory data Higher mortgage rates with duration will likely lead to higher inventory, which we have seen repeatedly for the past 10 years. 2022: 18.7%

What’s going on with housing inventory ? The last four weeks of new listings data have been the most volatile since mortgage rates breached 6% in 2022. In reality, the volatility in housing inventory is due to the Labor Day holiday, the start of school and the fact that new listings are trending at the lowest levels ever.

Since 2020, the seasonal bottom for housing inventory has arrived several months later than normal, making it more complicated to track housing inventory data. Still, we have some promising signs that we might have finally hit the inventory bottom for 2023. I hope the seasonal bottom was two weeks ago.

We finally have six weeks of numbers that hit my housing inventory growth model perfectly in 2024. Last year, with higher mortgage rates , we had zero weeks at this level so I am now giving 2024 inventory growth a grade of A. have higher inventory than the national data.

The spring housing market music is playing, and purchase application data and active listing inventory rose together last week. The fear of not having an increase in inventory this spring should be put to rest. The other focus should be where mortgage rates go; only a little happened last week.

But, even with mortgage rates higher this year than last year, demand is rising. Once I make some holiday adjustments, we have eight weeks of a positive trend since mortgage rates fell from the 8% high , and as of now, the slightly higher rates we’ve seen recently haven’t impacted the data just yet. This is common in January.

After seeing disappointing inventory growth two weeks ago , which I chalked up to the Memorial Day holiday, I was hoping for a big push in active listings last week, but that didn’t happen. And, the recent uptick in mortgage rates to almost 7% slowed purchase application data again. First, it took the longest time in U.S.

The slow zombie crawl of housing inventory went lower last week as inventory was negative week to week. In addition, mortgage rates rose to a yearly high as labor data stayed firm and purchase apps had their first negative week after three straight weeks of positive growth. The 10-year yield is close to yearly highs as the U.S.

Going into 2023, people thought housing inventory would skyrocket, home prices would crash, and we would see the housing market of 2008 all over again. Looking back on 2023, the inventory story was a big surprise even as mortgage rates headed toward 8%, as the data below will show. Weekly inventory change (Dec.

Total housing inventory growth has been slow in 2023, but with rising mortgage rates over the last few months, inventory has grown a bit faster than average. The question now is: Have we hit the seasonal peak in inventory for 2023? Last year, according to Altos Research , the seasonal peak for housing inventory was Oct.

Mortgage rates were scarier than Freddy Krueger last week, rising to a 23-year high as some of the labor data surprised to the upside. Unfortunately, those higher mortgage rates didn’t spur inventory growth this week, so we didn’t even get the benefit we would usually see when rates rise.

Last week we saw a noticeable decline in new listings and active inventory was barely positive. Does this mean housing inventory has begun its seasonal decline? That said, I hope we extend inventory growth longer before the seasonal decline. Here are the numbers, according to Altos Research : Weekly inventory change (Sept.

Just when I thought it was safe to say we were getting more traditional spring housing inventory , we hit a snag last week, as active inventory and new listings declined. We had a lot of drama over the week between Federal Reserve meetings and banking stress, and mortgage rates and purchase applications both fell.

These events led to lower mortgage rates and increased purchase application data last week, but decreased housing inventory. Here’s a quick rundown of the last week: The 10-year yield had a Lord of Rings battle at a critical technical level, pushing mortgage rates lower at the end of the week with no real break in the bond market.

The seasonal housing inventory bottom evaded us again last week as active listings fell and new listing inventory decreased. Mortgage rates didn’t move much last week, but the 10-year yield rose even though inflation data was tamer than expected, and we had a weaker retail sales report number. The answer is no!

Last week, housing inventory grew and the number of price cuts fell, which is expected at this time of the year. I hope the next thing we see is housing inventory grow at the level it typically does in January or February instead of being delayed until March or April. So let’s hope for more home sellers in 2024. 2022 21.7%

The best housing story in 2024 is that inventory is growing — both active inventory and new listings. With mortgage rates at the current levels, inventory is still below my expectations, but it’s still such a positive story that I had to discuss it on CNBC last week. 2022: 17.2% So far, so good here.

The housing market faced some serious obstacles last week as the 10-year yield broke over 4%, mortgage rates rose to over 7%, purchase apps fell again and we are still trying to find the elusive seasonal bottom for housing inventory. I discussed my theory on why inventory bottoms out later in the year on this HousingWire Daily podcast.

This is why I’ve created the Housing Market Tracker — a weekly analysis of purchase apps, housing inventory and mortgage rates that will be published every Monday. The Altos Research weekly inventory data looks ahead before the sales report inventory data. The 10-year yield shows where mortgage rates will go.

Last week we saw a noticeable slowdown in housing inventory growth that I hope has more to do with a holiday week than a trend. Mortgage rates fell last week after the debt ceiling issues were resolved, but the damage from higher rates took its toll on purchase application data again.

The 30-year fixed mortgage has followed suit, recently falling as low as 6.75%, the lowest level since mid-December. Its quite obvious that stubbornly high mortgage rates slowed down early season homebuyers in the first quarter of 2025. So, mortgage rates have been declining for several weeks now. Thats a pretty notable swing.

Given the current housing inventory crisis, it might surprise people to realize this: we built too many homes during the housing bubble years. Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. Wait, what?

Housing demand grew and inventory levels fell again while mortgage rates rose. Mortgage rates rose to 6.57%. Active inventory fell by 3,141, and new listing data fell again and is still trending at all-time lows. The 10-year yield and mortgage rates Last week was interesting for the 10-year yield and mortgage rates.

While weekly inventory is still falling, we have year-over-year growth in total active listing and new listings data. This calls into question a mortgage rate lockdown, as mortgage rates are also higher year over year. However, this data can move stronger in either direction when mortgage rates rise or fall aggressively.

Last week, mortgage rates hit a 21st-century high, the 10-year yield closed slightly higher than my peak forecast for 2023 , and housing inventory growth was still slow. Mortgage rates went from 7.19%% to 7.37%. Last year, the seasonal decline took longer than usual, but 2022 was an abnormal year with mortgage rates.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content