This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Despite several indicators of a slowing housingmarket, prospective home buyers should not get too excited – inventory remains limited and changes are in line with the traditional seasonal slowdown, according to RE/MAX ’s August national housing report. Low inventory is another indication of a still-scorching housingmarket.

housingmarket and that they need to be pro-housing again. Even with all the drama we have dealt with in 2022-2023, the housingmarket stayed intact and never broke. However, one thing is sure: from 2020 to 2023 we never saw credit-stressed home sellers. Weekly inventory change : (Dec.15-22)

24): Inventory fell from 569,898 to 565,875 The all-time inventory bottom was in 2022 at 240,497 The inventory peak for 2024 so far is 739,434 For some context, active listings for this week in 2015 were 1,104,310 New listings data While active inventory didn’t rise, we did get a nice boost in new listings this last week.

The spring housingmarket music is playing, and purchase application data and active listing inventory rose together last week. The fear of not having an increase in inventory this spring should be put to rest. The other focus should be where mortgage rates go; only a little happened last week.

The 2022 housingmarket was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Housing recession. That would be a positive for demand.

This is one reason housing inventory has taken so long to bottom out. Mortgage rate volatility was so wild in the second half of 2022 and even this year that some home sellers are gun-shy in listing their homes, since they will be buying another one. In 2007, when sales were down big, total active listings peaked at over 4 million.

The rise of active listings in this spring housingmarket reminds me of a zombie slowly rising from its grave. Yes, we found the seasonal bottom for housing inventory on April 14, but this year’s rise in active listings has been tepid at best. Can you imagine the housingmarket at that point?

The housingmarket welcomed the news of lower mortgage rates last week after four reports showed that the labor market isn’t as tight as it seems and that the fear of 1970s-entrenched inflation was a lousy narrative. Current housing Inventory is still not suitable for a healthy housingmarket. but now U.S.

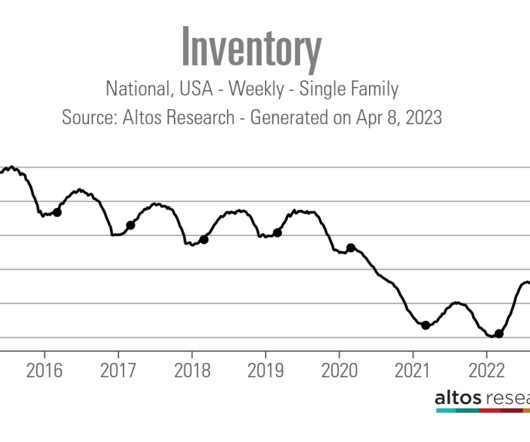

This is precisely what the doctor ordered for the housingmarket. In March of 2022, we only had 240,000 active single-family homes available for sale, leading me to call the housingmarket savagely unhealthy as we simply had too many people chasing too few homes.

The housingmarket in Washington D.C. Sweeping cuts by Elon Musks DOGE agency have sent many government employees packing, while other staff need to find housing in the area to comply with return-to-work mandates. housingmarket. In total, 502 single-family homes hit the market, followed by 457 condos.

We have often discussed that the housingmarket dynamics changed starting Nov. The other big story with housing inventory is that new listing data has been trending negative year over year since the end of June 2022. Since May 15, that trend has continued to the point that inventory in America is now negative year over year.

We created the weekly HousingMarket Tracker because housing data has been so wild since 2020. The housingmarket madness persisted last week as inventory fell and higher mortgage rates took a bigger bite out of purchase application data. A traditional seller is a conventional buyer most of the time.

Mortgage rates recently hit a year-to-date low, coinciding with ongoing market disruptions from tariffs. The more encouraging story, however, is that the spring season is shaping up positively for the housingmarket. Notably, purchase applications show growth both year-to-date and year-over-year.

The affordability hit with higher mortgage rates has impacted new listings data since most sellers are buyers, thus facilitating an all-time low in new listings data. More importantly, it showed that the days on market dropped back to the teenager level, which means we are once again in a savagely unhealthy housingmarket.

People have to balance the cost of money with things like job security when theyre buying houses. The thing to keep in mind for the housingmarket as we roll into March is that mortgage rates have been easing down. That comes to 2% more unsold new listings and actually 5% fewer sellers overall than in 2024.

This article is part of our 2022 – 2023 HousingMarket Forecast series. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the predictions for this year, along with a roundtable discussion on how these insights apply to your business.

The housingmarket was crazy again last week. Mortgage rates fell as the banking crisis got worse and purchase application data grew for the second week in a row, but the big question is: Did we hit the seasonal bottom in housing inventory? However, you don’t need to be a rocket scientist or have a Ph.D.

PEARL DISTRICT SUMMARY STATISTICS Taking the 35,000-foot view, we can see the average yearly prices have been steadily declining since 2016: Average prices this year are essentially the same as they were in 2015. As of this post date, the unit is back on the market for a more “modest” asking price of $4,500,000.

One of the reasons total inventory data hasn’t gotten back to 2019 levels is the lack of sellers in 2023 and 2024. Here are new listings for last week over the past several years: 2024: 62,876 2023: 57,229 2022: 59,458 Price-cut percentage In an average year, one-third of all homes take a price cut — this is standard housing activity.

With the exception of the previous four-week period, there is the highest supply on the market in six years, with five months available, up from 4.4 National HousingMarket Data Key Highlights U.S. Weekly housing-market data goes back through 2015. The median monthly housing payment is now $2,784, up 8.3%

Most home sellers are buyers of homes, so the action we are seeing this year is a healthy step in the right direction to get more balance in the housingmarket ,” Mohtashami wrote on Saturday. For context, active listings during the same time frame in 2015 were substantially higher at 958,304. Between Feb.

housingmarket saw dramatic changes in affordability as mortgage rates skyrocketed 500 basis points. After an initial rush to get to market in Q2 2022, new listings volume fell precipitously. After an initial rush to get to market in Q2 2022, new listings volume fell precipitously.

For every 50 basis point change in mortgage rates, the monthly payment for this house would change by $112.In housingmarket saw dramatic changes in affordability as mortgage rates skyrocketed 500 basis points. What’s not measured in the FHFA paper is how by 2023, seller volume had already been declining for nearly a decade.

Going into 2023, people thought housing inventory would skyrocket, home prices would crash, and we would see the housingmarket of 2008 all over again. We created this weekly tracker at the end of 2022 to give people a live weekly outlook on everything that drives the housingmarket and which factors to follow.

The last time we saw this kind of effect was when mortgage lenders had to start incorporating TRID in 2015 — it created a one-month crash in existing home sales because it just took a bit longer to close a deal. The following month, those sales rebounded as everyone finds a rhythm in how to operate. Weekly inventory change (Aug.

Weekly housing inventory data The best story in 2024 has been inventory growth. We can’t have a functional housingmarket with the inventory levels we saw from 2020-2023. This year we’ve gotten enough inventory growth to create a buffer so we don’t have another savagely unhealthy housingmarket when mortgage rates fall.

On a positive note, however, the days on the market are no longer a teenager anymore: that metric grew from 18 days to 21 days. I cheer because the savagely unhealthy housingmarket theme I talked about back in February of this year was the same premise of the housing reset talking point the Federal Reserve uses.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housingmarket was last year — and it got a lot worse this year — it’s a blessing that was much needed. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housingmarket we had from 2002-2005.

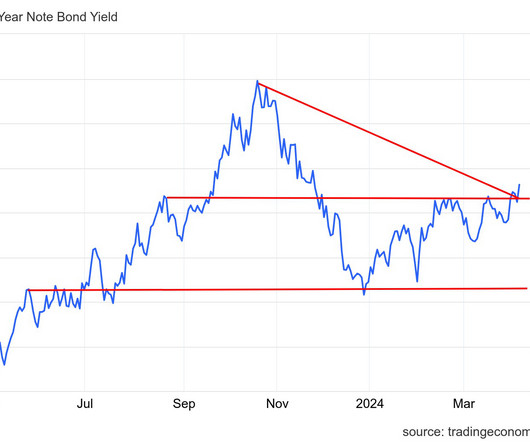

So, what does this all mean for the housingmarket and the future of mortgage rates? One thing to remember with the labor data is that it’s no longer a tight labor market, but it hasn’t broken yet. But now we have the big jobs week coming up!

Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. We had a few years where sales missed expectations in 2013, 2014, and 2015. million total housing starts until 2020-2024, when demand would warrant that many housing starts.

We finally have six weeks of numbers that hit my housing inventory growth model perfectly in 2024. Low inventory has plagued the housingmarket since the pandemic, plummeting to all-time lows in March of 2022 when we only had 240,000 single-family homes available for sale. Today that number is 668,383.

Here is the price cut percentage data for the same week in other years: 2023 38% 2022 42% 2021 27% As you can see, affordability is an issue, and the price cut percentage is higher now than in any period from 2015-2021, but still below 2022 levels. Last year, according to Altos Research , the seasonal peak for housing inventory was Oct.

Let’s take a look at the inventory data this year to test this premise, since for many months it has been a working theory of mine that new listings data behavior last year marked a bottom and even going into 2024 we should see more sellers. With mortgage rates higher, will this stop inventory from growing year over year?

Imagine a housingmarket with just 6% mortgage rates or lower — it would be growing like what we see in the new home sales market. Weekly housing inventory data The best housing story for 2024 so far is that inventory is growing yearly. When mortgage rates fall, demand picks up.

In a hostile housingmarket and a noisy industry environment, why is Zillow outperforming?” According to Barton, the “substance of the settlement” is a “very reasonable middle path forward for the industry, where commissions are communicated between sellers and buyers and both parties are better educated.” he posited.

As most sellers are buyers, seeing more sellers listing their homes has been good. With more sellers who are buyers, we have a tad more demand this year. If mortgage rates head lower and stay lower, this contract data will grow, but we don’t see that growth in mortgage demand yet.

Most sellers are buyers and the housingmarket needs standard new listing data for the rest of the year. With more sellers who are buyers, we have a tad more demand this year. The last thing I want to see is a repeat of the second half of 2022 when we saw new listings data take a noticeable seasonal decline.

I believe we should get more sellers in 2024 than in 2023, but that doesn’t necessarily mean home prices will fall. This is why following the housingmarket tracker tied to the 10-year yield, mortgage rates, and purchase application data will be as critical as last year to tell you what’s going on in the housingmarket.

Today, we will examine new listing data more extensively to provide a clear example of a stressed sellermarket and compare that to where we are today. 2015 81,875 2016 80,293 2017 84,293 2018 98,972 2019 87,278 Now, let me show you what stressed sellers’ data looks like.

That is the critical period for new listing data to grow; remember, most sellers are buyers. 9, 2023, we can retire this data, as this was the date I believed the housingmarket dynamics shifted last year. Weekly inventory change (Nov. 10) : Inventory rose from 566,882 to 566,941 Same week last year (Nov. If we start from Nov.

housingmarket, and we should ignore the decline last week. Number of new listings last week, by year: 2024: 54,769 2023: 55,008 2022: 63,374 Price-cut percentage In an average year, one-third of all homes take a price cut; this is standard housing activity. This variable can change when we experience a recession or job loss.

Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. We had a few years where sales missed expectations in 2013, 2014, and 2015. million total housing starts until 2020-2024, when demand would warrant that many housing starts.

However, considering the affordability challenges with the housingmarket , it’s good to see a flip in the housing data without rates getting under 6%. Since most sellers are buyers, we need this data line to get back to the pre-COVID-19 trend range, which it hasn’t been able to do since the second half of 2022.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content