This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Early in 2021, when I was talking about how people should worry about home prices overheating, I had a glimmer of hope that maybe toward the end of 2021 we would be spared another seasonal collapse of inventory. Inventory always falls in the fall and winter, but I hoped it wouldn’t be a repeat of 2020.

One of the most important housing market stories in recent weeks has been the decline in new listings , which has slowed the growth rate of total inventory. One thing that I have stressed is that higher mortgage rates can create a slowdown in demand and thus allow more inventory to accumulate through a weakness in demand. million to 1.93

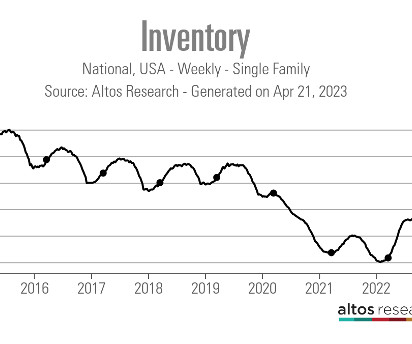

Since 2020, the seasonal bottom for housing inventory has arrived several months later than normal, making it more complicated to track housing inventory data. Still, we have some promising signs that we might have finally hit the inventory bottom for 2023. Again, I am a bit mindful here due to Easter.

Just when I thought it was safe to say we were getting more traditional spring housing inventory , we hit a snag last week, as active inventory and new listings declined. Weekly housing inventory The numbers this week are unfortunate: inventory should be growing like it does at this time every year.

Given the current housing inventory crisis, it might surprise people to realize this: we built too many homes during the housing bubble years. Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. Wait, what?

It’s an excellent time to discuss housing inventory. How can housing inventory be so low today when it skyrocketed back in 2009? If you follow the trend of housing supply since 2014, it’s been falling every year — with a pause in 2018-2019 — and then collapsed lower post-2020. I don’t believe housing inventory below 1.52

2 million , we could be at risk of housing inventory falling to such low levels that I would have to categorize this housing market as unhealthy. We can see that inventory falling to such low levels has created unhealthy home-price growth in both 2020 and 2021. Inventory fades in the fall and winter and picks up in summer and spring.

The housing market experienced more volatility last week, with housing inventory dropping as mortgage rates moved higher. Weekly housing inventory continues to decline, as we saw a decrease of 13,238 units, double the amount we had this time last year. So, when I saw the slight inventory increase, I thought this was a good trend.

In the realm of housing, the term “ silver tsunami ” often refers to the idea that older homeowners will aim to downsize and sell their homes, theoretically flooding the market with new inventory. Such a scenario has not occurred and analysts, including HousingWire ’s Logan Mohtashami , doubt it ever will.

Total available inventory is gradually climbing about 1% per week — last year it was still declining in April. As we roll into the second quarter, we should have accelerating inventory growth each week. NAR reported 33% all cash buyers, which is the most since 2014 when buyers were still cleaning up distressed properties.

Given the current housing inventory crisis, it might surprise people to realize this: we built too many homes during the housing bubble years. Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. Wait, what?

I always try to focus people on the total inventory data until we get inventory back into a range of 1.52-1.93 HousingWire: To add to that, since housing is in an inventory shortage, the market has changed, so the good news is inventory is growing. What levels should we be hoping for? Then this happened. Ghost Supply 2.2

2012: What they said: Shadow inventory will cause prices to fall. The reality: Inventory broke down in 2012, and the monthly supply data got below 6.0 The “shadow inventory” was not an issue as it took years to get rid of the distressed supply from the housing bubble years. million of inventory is normal.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Inventory levels broke to all-time lows and thus created massive housing inflation quickly, which broke my model. We saw this happen in 2013-2014 and 2018-2019.

For now, though, the low inventory means housing starts have legs to move higher. Existing home inventory is also at all-time lows. Existing home inventory is also at all-time lows. Unsold inventory sits at an all-time-low 2.5-month In 2013/2014, when the economic data was improving, mortgage rates rose.

But, there is one bright spot — inventory is rising. This has been a concern of mine after the summer of 2020 as inventory levels were breaking all-time lows, facilitating unhealthy home price growth during a more prominent demographic patch in U.S. The one positive: Inventory is rising. Once total inventory levels reach 1.52-1.93

Second, because of the downtrend in inventory since 2014 and the demand pick-up we will see in the years 2020-2024, we had a risk of home prices accelerating too much. They’re mindful of higher rates because in 2013, 2014 and 2015 they had to deal with a miss in sales expectations. First, total home sales should be 6.2

However, the real story of 2022 is that the savagely unhealthy housing market continues as inventory is still lower than last year, sending home prices growth into double digits again. In 2013-2014, rates rose, and you see the lower trend in sales back then. 2014 was the last year total inventory grew. million and 6.16

The home-price growth from 2020 through 2022 has been so unhealthy that I’ve labeled this a savagely unhealthy housing market as inventory has once again collapsed on a year-over-year basis in 2022. Inventory is still showing negative year-over-year data. The last time this data line was fragile was back in 2013-2014.

The premise of a mortgage rate lockdown is simple: so many American households have such low mortgage rates that some will never move once rates rise, which then locks up housing inventory. Typically we have a natural set of new listings each year; inventory rises in the spring and summer and then falls in the fall and winter.

Inventory, which has been falling for years, broke to all-time lows in 2020. We didn’t have a seasonal push in inventory in 2020, and things worsened in 2021. Of course, this has brought back some inventory, as demand weakness always creates inventory through accumulation. million active listings, but at just 1.28

Inventory has broken to all-time lows, but it doesn’t look like the year-over-year data will be positive at all this year unless demand softens up. NAR Research : Unsold inventory sits at a 1.7-month NAR Research : Unsold inventory sits at a 1.7-month However, negative year-over-year inventory is not what we want to see.

years in 2014. Its unclear how effective Prop 19 has been at freeing up housing inventory. Tight inventory only pushes home prices up more, and adds to the generational homeownership divide. California is also home to three of the five U.S. metros with the biggest increases in homeowner tenure over the last decade.

However, Khater noted the homebuying surge has created a seller’s market, where inventory is at a record low and home prices are rising, beginning to offset the benefits of the low rates. census divisions rose 7% in September from a year ago, the greatest year-over-year gain since 2014.

Realtors cited a combination of high demand and low inventory, which are making conditions more competitive and exerting upward pressure on prices. Pending home sales looks specifically at contracts that have been signed but where the transaction has not closed on sales of already existing inventory. Presented by: Fannie Mae.

Available inventory of homes to buy follows a reliable seasonal trend with the low in Q1 and the high in Q3 of each year (except for the 2020 pandemic year). We include details of inventory changes and the relationship to interest rates in the sections below. Part of the home sales slowdown in 2023 was due to a lack of inventory.

census divisions rose 7% in September from a year ago, the greatest year-over-year gain since 2014, and nearly 23% higher than its last peak in 2006. uptick reported in August, and represented the largest annual gain since May 2014 as record-low mortgage rates and a lack of inventory continued to put upward pressure on home prices.

The three categories I’ll cover will be the weekly purchase application data, the Altos Research weekly inventory data , and what the bond market/ mortgage rates did recently. Housing market inventory. Altos Research data shows that the weekly inventory fell from 521,957 to 507,934 last week.

As elevated mortgage rates and tight inventory continue to weaken housing demand, the volume of existing home sales declined for an eleventh consecutive month as of December, according to the National Association of Realtors (NAR). This is the longest run of declines since 1999.

history, and because of that, not even low inventory could prevent home prices from declining month to month in the second half of 2022. Now we can talk about the final stage: inventory in the U.S. Housing inventory The No. How would new listing data trending at all-time lows impact the active inventory in 2023?

The last time we had a consistent downtrend in existing home sales was back in 2013-2014. During that same period, the MBA purchase application data were down 20% year over year on-trend in 2014. We saw this in 2018 and then spent the entire year of 2019 selling off the excess inventory. Keep this scenario in mind for 2021.

Mohtashami focused on the latest inventory and the Federal Reserve’s rate hike announcement. In 2013-2014, when rates jumped very fast, this index trended down by negative 20% year over year to hit an adjusted population all-time low in 2014. On a sour note, we still need more inventory to return to normal.

3 above), for example rising inventory and long days-on-market, I get discouraged about my ability to sell. And in fact, inventory of unsold homes in the country is up 40% over last year. As homeowners with high mortgage rates are more likely to sell their homes, rising rates leads to rising inventory. 2 above) themselves.

By watching the unsold inventory data, we can observe that demand accelerated more than supply at this time. Part of the home sales slowdown in 2023 was due to a lack of inventory. In 2024 as inventory increases, we can see the rate of sales increasing as well. We call this a supply-constrained market.

After making some Covid-19 adjustments to the data line, we will have our first negative year over year since 2014, unless something changes on the mortgage rate side. 2014 was the last year we saw a noticeable weakness in purchase application data. Inventory is very seasonal. What have we seen this year? million – and 1.93

Looking at the housing market in the years 2020-2024, one risk i identified early on was that home prices could accelerate more in this period than we saw in the previous expansion if inventory channels broke to all-time lows. Back then, we had higher sales, higher inventory, and less price growth, but we had a massive credit bubble.

last month, still hovering near levels previously seen in 2014, though it is the third month in the past four that credit availability has picked up as supply eases out. Ongoing strength in home-purchase applications and home sales continue to signal robust housing demand, even as low housing inventory remains a constraint,” Kan said.

This is something that I said would change the tone of housing, and we are seeing that result this year as sales decline and inventory picks up. We were told that population growth is slowing, we were told that Americans would panic sell and that massive inventory would hit the marketplace once rates got to 4%. Wait, what? I use the 1.52-1.93

For refinances, Fannie Mae’s survey revealed the net share of lenders who expect demand growth reached a survey high for government loans and the second highest reading since 2014 for GSE-eligible and non-GSE-eligible loans.

Some historical references: The last two times rates rose, this is what we saw — 2013/2014 negative — 20% year over year trend 2018 purchase application data was flat to slightly positive all year long; we only had three mild negative years over year prints when rates headed to 5%. This data line is trend survey data.

On top of all that, since inventory is at all-time lows, it’s been harder and harder for first-time homebuyers to win some bids because they don’t have more money to bring into the bidding process. However, let’s be realistic here: housing inventory has been falling since 2014 and 2022 isn’t looking any better.

Home prices have continued to increase this year as a result of low inventory and high demand for homes. growth rate was more than six and a half years ago, in March 2014.”. The S&P CoreLogic Case-Shiller index covering home prices of all nine U.S. census divisions, reported an 8.4% The National Index is now up 24.5%

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. To have that market, we need total inventory data to get back to 1.52-1.93

While spring of 2022 saw a similar share of all-cash homebuyers, one needs to look back to 2014 before seeing similar shares. Homebuyers placed competitive offers on homes while inventory grew increasingly difficult to find. At that time, housing inventory dropped to historic lows making the environment ripe for investors.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content