This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

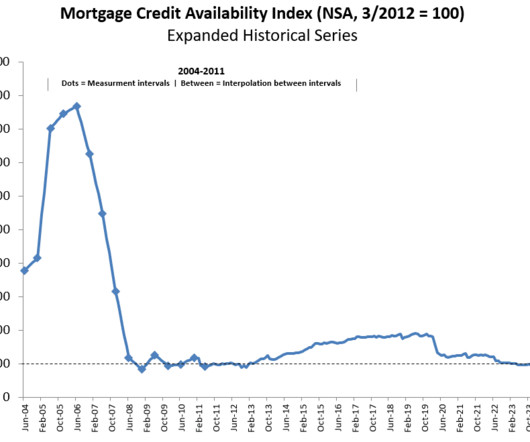

The Mortgage Credit Availability Index (MCAI), a report from the Mortgage Bankers Association (MBA) based on data analysis from ICE Mortgage Technology , indicates a drop in mortgage credit availability in September. While increases in the index point to looser credit, a decrease in the MCAI suggests tighter lending requirements.

to 96.6the MCAI, a survey from the Mortgage Bankers Association (MBA) that examines data from ICE Mortgage Technology , shows that mortgage credit availability also ticked up in January. While an increase in the index signifies loosening credit, a decrease in the MCAI suggests tightening lending rules.

A former Quicken Loans executive, Booth has over 15 years of experience working in state and federal government bodies, focusing on transforming the mortgage industry through technology. Planet Home Lending has promoted four people to vice president positions, supporting the company’s continual growth.

A decrease in the index score indicates that lending standards are tightening, while increases are indicative of loosening credit. The index which uses data from ICE Mortgage Technology was benchmarked to 100 in March 2012. Mortgage credit availability increased in January, rising 2.5%

Mortgage credit availability saw a slight increase in May, according to an analysis of ICE Mortgage Technology data by the Mortgage Bankers Association (MBA). The index was initially benchmarked to 100 in 2012. The MCAI measures how tight or loose lending standards are in any given month.

Snapdocs, founded in 2012, works with hundreds of mortgage lenders and title companies, as well as 100,000-plus settlement agents and 140,000 qualified notaries. The collaboration in May was aimed at enabling warehouse lenders to seamlessly and securely manage eNote transactions within their warehouse lending system of record.

million in 15 funding rounds with 25 investors since its inception in 2012. HousingWire reported that in June 2022, the company raised $115 million — $60 million in equity and $55 million in debt — while acquiring Denver-based lending startup Accept.inc. In 2019, HomeLight acquired Eave , a digital mortgage lending startup.

The Mortgage Credit Availability Index (MCAI), a survey from the Mortgage Bankers Association (MBA) that examines information from ICE Mortgage Technology, indicates that mortgage credit availability rose in June. While increases in the index point to looser credit, a decrease in the MCAI suggests tighter lending requirements.

A decline in the MCAI indicates that lending standards are tightening, while increases are indicative of loosening credit. The index, which uses data provided by ICE Mortgage Technology, was benchmarked to 100 in March 2012.

The availability of mortgage credit increased in January, according to a report issued by the Mortgage Bankers Association (MBA) based on data sourced from ICE Mortgage Technology. over December’s figure, based on initial benchmarking of the index to 100 in 2012. and the Conforming MCAI rose by 0.2%

The report, which analyzes data from ICE Mortgage Technology, was benchmarked to 100 in March 2012. A decline in the index score indicates that lending standards are tightening, while increases in the score are indicative of loosening credit. Mortgage credit availability increased in October, rising to a score of 99.2

The Mortgage Credit Availability Index (MCAI) , a survey from the Mortgage Bankers Association (MBA) that examines information from ICE Mortgage Technology, indicates that mortgage credit availability rose in July. While increases in the index point to looser credit, a decrease in the MCAI suggests tighter lending requirements.

In light of this, HousingWire recently caught up with Teraverde Chief Technology & Innovation Officer Rob Peterson to learn more about the key to lender profitability in today’s lending environment. Rob Peterson: Most segments of the economy have effectively adopted technology to reduce their costs. Louis computes a 34.7%

Jamie Thornton, director of online mortgage lending at Real Genius, said in a statement that the company has “invested a significant amount of time and resources” into developing technology for customers. Since 2016, we’ve helped more than 51,000 families with their mortgage needs, lending more than $15 billion,” said Thornton.

The cooperative members cover the entire lending spectrum, originating between $50 million and $25 billion per year. Another initiative is a cloud-based technology called Lenders One Loan Automation (LOLA), launched to automate the loan manufacturing process.

I sat down with Deitch for a wide-ranging conversation on the ways lenders can claw back profitability through smart technology and products that meet the moment. Cost to originate But providing the right lending products is only one factor in succeeding in this market. “Lenders spend 66% on people and 6% on technology. .

As demonstrated in the brilliant UWM Superbowl ad , Millennial homebuyers are looking to technology to match them with the right partners in life, including their mortgage. With smarter and faster data, a personalized service experience is key for the future of lending. #2 5 Technology becomes fintech. 1 Personalization.

California-based ICE Mortgage Technology announced this week two enterprise agreements to integrate its eClose solution to Maxwell and Roostify platforms, enabling a more streamlined closing process for lenders and borrowers. Roostify, a mortgage technology provider, will integrate the solution to its digital home lending platform.

Johnson, whose career with Fannie Mae spans for almost two decades, is currently responsible for leading the mortgage giant’s digital transformation , which includes overseeing Fannie Mae’s technology, data, enterprise models and operations. What are the building blocks of digital lending? Presented by: Wolters Kluwer.

has raised $175 million to accelerate growth and fund new technologies , just 16 months after relaunching its operations. billion in 2012 to $2 billion in 2016. Last year, Interfirst relaunched its services with a new proprietary loan origination technology platform. Chicago-based mortgage originator Interfirst Mortgage Co.

Back in 2008, an artificial housing bubble burst due to reckless mortgage lending and speculative buying, leading to widespread foreclosures and a dramatic drop in home prices. million in 2006 to about 999,000 by 2012. The aftermath of the 2008 crisis led to significant attrition among real estate agents. About 38% of U.S.

Mortgage credit availability increased in May, according to the Mortgage Credit Availability Index (MCAI) , a report from the Mortgage Bankers Association (MBA) based on data from ICE Mortgage Technology. A decrease in the MCAI suggests tighter lending rules, whilst an increase in the index indicates looser credit.

It has raised a total of $655 million since its founding in 2012, according to Crunchbase. Blend’s white label technology is what powers mortgage applications on the site of banks such as Wells Fargo and U.S. Since it was estabslihed in 2012, Blend has been run by its co-founders ? Presented by: FADT.

Even in the midst of a banner year, originators have to keep one eye on the technologies and competitors that could upend their carefully crafted business strategy. Taking those lessons with him, Ghamsari decided to start Blend in 2012 along with his co-founders. The focus of the Spring Summit is The Year-Round Purchase Market.

Most recently, the private-equity firm invested in Real , a technology-powered real estate brokerage in 2020, and perhaps most notably, e-recording provider Simplifile in 2013. In fact, prior to founding SimpleNexus in 2011, CEO Matt Hansen worked on the Simplifile development architecture team for nearly five years. billion.

Available in its Blend Builder Platform, users can build their own origination products, leverage integrations, and use modular blocks to resolve the complexity of an existing technology infrastructure, the company said in an announcement about the launch on Tuesday. Founded in 2012, Blend went public in 2021.

LoanStar Technologies , which connects lenders with borrowers who are traditionally underbanked or unbanked, also made the list again. 403 Homelight 1,444% 2012 Providing a platform that helps deliver better outcomes for homebuyers and sellers. Homelight , a platform for homebuyers and sellers, was No. The company was No.

Debenture interest refers to the percentage of a return that an investor would receive for lending money through a debenture. As in the proposed rule, the final ML also includes certain changes made in January 2024 to the Home Equity Reverse Mortgage Information Technology (HERMIT) system. The ML goes into effect on Sept.

It has raised a total of $655 million since its founding in 2012, according to Crunchbase. Blend’s white label technology is what powers mortgage applications on the site of banks such as Wells Fargo and U.S. In all, its technology platforms saw $1.4 That January round gave Blend a $3.3 billion valuation.

Fintech-focused Canapi Ventures led the investment, which brings Blend’s total venture raised to $365 million since its 2012 inception. That digitization, he said, has been fueled by rapidly changing consumer expectations and increased confidence in the ability of lenders and other mortgage industry players to adopt new technologies quickly.

The company’s job cuts include human resources, technology, talent acquisition, and executive assistant positions. Presented by: Acra Lending. In 2012, the historically low interest rates led to a boom in refinances, and the lender grew to $14.5 The workforce reduction is also focused on mortgage loan production.

Mortgage Bankers Association (MBA) reports that mortgage credit availability decreased in May according to the Mortgage Credit Availability Index (MCAI), a report that analyzes data from ICE Mortgage Technology. The index was benchmarked to 100 in March 2012. The MCAI fell by 0.9% to 120 in May. Mortgage credit supply declined for the.

HousingWire recently spoke to Amanda Phillips, executive vice president of compliance at ACES Quality Management, about getting servicing staff and technology ready to meet upcoming regulatory requirements while ensuring quality throughout the life of the loan. Without technology, this will be an overwhelming burden.

Blend’s investors are apparently convinced that the company can radically transform lending, simplifying and digitizing regimented-but-clumsy processes that are still rather paperwork-heavy. ” Blend’s white-label technology is what powers mortgage applications on the website of traditional banks such as Wells Fargo and U.S. .

Mortgage credit availability decreased in March according to the Mortgage Credit Availability Index (MCAI), a report from the Mortgage Bankers Association (MBA) that analyzes data from ICE Mortgage Technology. The index was benchmarked to 100 in March 2012. The MCAI fell by 0.7% The Conventional MCAI increased 0.3%, while.

Real estate still relies on a “system” unable to integrate production across the silos of media, brokerage, lending, insurance and trading. Technology and the trust model Real estate is too vital to our economy to be so financially concentrated and functionally outdated.

Mortgage credit availability decreased in January according to the Mortgage Credit Availability Index (MCAI), a report from the Mortgage Bankers Association (MBA) that analyzes data from ICE Mortgage Technology. The index was benchmarked to 100 in March 2012. The MCAI fell by 0.9% in January.

HousingWire recently spoke with John Keratsis, President and CEO of Deephaven Mortgage, about the potential benefits of non-QM lending in today’s tight housing market. The technology is excellent and has significantly streamlined our communications and processing. Deephaven has been doing non-QM since 2012.

Interest rates have risen from a low of less than 3% in 2012 to over 7% today, meaning that 99% – according to Goldman Sachs – have a lower rate and would not benefit from a refinance. This left a void in the mortgage lending market, which was filled by IMBs.

In 2012, Dmitry Godin was seemingly on top of the world. The historically low interest rates that led to a boom in refinances in 2012 had ended, and Interfirst struggled to maintain volumes in following years as the market turned to purchase. Interfirst Mortgage , the retail mortgage business he founded in 2001, had grown to $14.5

The program is available to a wide range of homeowners, with lending limits as high as $4 million*. For lenders unfamiliar with reverse mortgage products, RMF makes it easy to get into the business with its technology platform, training, marketing assistance and industry-leading support.

Over the last year, it has also sold off large chunks of the business – including sub-servicing with ServiceMac and delegated correspondent to Planet Home Lending – which accounts for several thousand workers transitioning to new firms. billion in 2012, the company decided to shutter its business in 2017.

A decrease in the index score indicates that lending standards are tightening, while increases are indicative of loosening credit. The index was benchmarked to 100 in March 2012. Mortgage credit availability decreased in September, falling 0.5% to a score of 98.5 Credit availability for conventional loans decreased 1.7%

The first category is real estate credit, which covers most establishments focused on lending with real estate as collateral. The second category is mortgage and non-mortgage brokers, which includes establishments that facilitate lending by bringing borrowers and lenders together. Source: Nationwide Multistate Licensing System.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content