This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Newlistings data has been moving lower over the last few weeks. But, we need to see more growth in newlistings data just to grow from 2023 levels. 2023 newlistings data was the lowest ever on record, so it’s already a low bar.

Today’s housingmarket suffers from affordability issues due to mortgage rates in the 7s and high home prices. People are quick to panic over any part of the housingmarket that looks stressed, fearing we’ll see 2008 levels of destruction all over again. Why choose 2011?

The 2022 housingmarket was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Housing recession. That would be a positive for demand.

Just when I thought it was safe to say we were getting more traditional spring housing inventory , we hit a snag last week, as active inventory and newlistings declined. However, one thing is for sure, housing is not going to crash due to large-scale panic-selling — a scare tactic of late 2021 that didn’t work then or now.

The rules of supply and demand economics always end up winning and weekly newlisting data is key. Newlisting data is growing year over year, but it will be the second-lowest newlisting data ever recorded in history. For the fifth time this year, inventory hit my target level with elevated mortgage rates.

One issue that has created a waterfall dive in purchase application data and sales is that newlisting data is declining faster than usual. Traditionally, when mortgage rates rise post-2012, home sales trend below 5 million. Since 2013 I have said that mortgage rates over 5.875% would be problematic to housing.

Home prices aren’t crashing, despite what the housing bubble boys are saying. The housing bubble boys are a crew that from 2012 to 2019 screamed housing crash every year. Those who know my work over the last 10 years know that I have Batman/Joker relationship with the housing crash people, because they never stop.

However, the housingmarket did run into one problem in 2020. Inventory levels broke to all-time lows and thus created massive housing inflation quickly, which broke my model. I knew housing would be OK as long as home prices only grew at 23% over five years — 4.6% This means less demand for housing.

One of the most important housingmarket stories in recent weeks has been the decline in newlistings , which has slowed the growth rate of total inventory. Once that happens, I can finally take the savagely unhealthy housingmarket theme off my talking points. What does this mean? million to 1.93

Typically we have a natural set of newlistings each year; inventory rises in the spring and summer and then falls in the fall and winter. However, we have entered a tricky period in housing economics where we might have to take this premise more seriously since mortgage rates recently got as low as 2.5% The parts of the U.S.

We have had two historic events that created a waterfall dive in demand recently; we now have precise data showing newlisting data declining with those events, which shows how important that data line is to housing demand. This is the biggest story in housing. . None of that has ever happened again since 2012.

from May to June, the largest drop at this time of year on record since at least 2012, according to a new Redfin study released this week. “In June we entered a new phase of the housingmarket,” Fairweather said. Finally, newlistings fell from a year ago in 15 of the 85 largest metro areas.

On a positive note, however, the days on the market are no longer a teenager anymore: that metric grew from 18 days to 21 days. I cheer because the savagely unhealthy housingmarket theme I talked about back in February of this year was the same premise of the housing reset talking point the Federal Reserve uses.

A perfect example is that the last few years, newlistings have been trending between 30,000 and 90,000 per week. It didn’t matter if mortgage rates were at 3% or 8%, newlisting data has trended at historic lows the past few years. So you can see why we have so few stressed sellers.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. From the index : I know it seems strange, but existing home sales are falling, and the monthly supply of new homes is at 10.9 crash, especially from 2012-2019.

above its asking price, that means it was listed for $301,872, said Daryl Fairweather, Redfin’s chief economist. That’s quite the contrast from back in 2012, when Redfin reported that condos were selling for more than 4% below asking price. If a condo sold for 0.7% year over year, and pending sales were up 38.2%

Declining mortgage rates could have improved affordability for buyers in the housingmarket in February, but instead spurred a demand that, combined with a persistent lack of inventory across the U.S., ” The annual home price growth rate fell to 1.94% in February, hitting a rate below 2% for the first time since 2012.

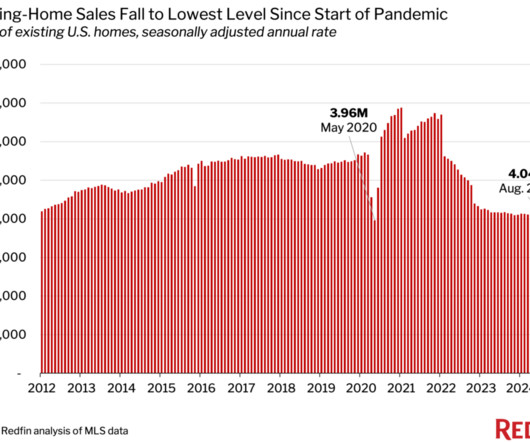

That’s the lowest level in records dating back to 2012, with the exception of May 2020, when the pandemic brought the housingmarket to a standstill. Pending sales—a more current gauge of housingmarket activity that includes both existing and newly constructed homes—fell to the lowest level on record aside from April 2020.

The chart (below) puts it in sharp focus: Except for the pandemic year of 2020 when there were 2559 newlistings that April, last month was the slowest April since at least 2008 when easy access to Northwest Multiple Listing Service data became available. between May 2007 and January 2012. Where are all the sellers?

The housingmarket across the country, and especially in Boston and New England, is experiencing a growth trend that’s accelerated over the last few years. With this apprehension in mind, we’ll discuss some of the things to expect from the housingmarket in the second half of 2019, going into 2020.

The housingmarket across the country, and especially in Boston and New England, is experiencing a growth trend that’s accelerated over the last few years. With this apprehension in mind, we’ll discuss some of the things to expect from the housingmarket in the second half of 2019, going into 2020.

This is not a new idea — I’ve been dealing with people predicting a housing crash since 2012. Where I disagree with Yun is this: We have more inventory because demand has been softer, and we have more newlistings this year compared to last. million for active inventory, the housingmarket is balanced.

This marks the introduction of a new feature. Each month, this blog will publish a fresh assessment of the King County area housingmarket. A patch of foul weather and persistent economic challenges chilled an already cold housingmarket. The bar is so low on listings and sales data that one might trip over it.

The season has been shaped by slumping newlistings, a slowly climbing number of homes sitting on the market from previous months, fewer closed sales compared to last year and prices moving plus/minus five percentage points year-on-year (YoY). monthly decline in available Seattle listings (793). on the Eastside.

The opening months of the Seattle/King County housingmarket can best be expressed as sparks of activity within a mostly tentative purchasing environment. The number of homeowners deciding to sell continues to lag, but inventory and time on market continue to [mostly] climb, reflecting still-hesitant buyers.”

As proof of the impact of the country’s low inventory and high cost of building materials , newlistings fell 16% – the second-largest decline on record since Redfin’s data began in 2012, only passed by the drop in April 2020. That’s with unprecedented winter storms hitting most of the South in February, too.

We need to take an approach to the housing crisis that embraces change, is inclusive and extremely productive. BY THE NUMBERS >> The West has suffered the greatest from the housing-market downturn over the past year, according to ATTOM Data Soluti ons, which indicated 23 of the 50 worse-off U.S. 8pm-midnight Rodeo, Aug.

in 2019, the amount of vacant office space has grown each quarter to finish 2021 at 11.6% (excluding available sub-lease space), a level not seen in the city since 2012. >> The chart below, courtesy of the Northwest Multiple Listing Service (MLS), shows breathtaking price appreciation in our region in recent years.

Warns Danielle Hale, chief economist with realtor.com: “While younger Millennial and Gen Z buyers are expected to play a growing role in the housingmarket, fast-rising prices will create a bigger barrier to entry for the many first-time buyers in these generations who don’t have existing home equity to tap for down payment savings.”.

Additional housing, particularly more affordable units, will only help strengthen the health of the public and economy. Housing affordability decreased in 45 of the 50 states from 2012 to 2019. About 57% of all newhousing was classified multifamily (four or more units in one location). AUGUST HOUSING UPDATE.

None of that action has been happening for 14 years because the credit market changed after the 2010 qualified mortgage rule. We had multiple refinancing waves in 2012, 2016, 2020 and 2021. Again, everyone pushing housing 2008 needs to snap out of it. Foreclosure data fell quarter to quarter in Q3.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content