This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Today’s housing market suffers from affordability issues due to mortgage rates in the 7s and high home prices. Let’s look specifically at the current market data compared to 2011. Why choose 2011? Last week in 2011, 396,955 homes hit the market without a contract. of homes were underwater.

The rules of supply and demand economics always end up winning and weekly newlisting data is key. Newlisting data is growing year over year, but it will be the second-lowest newlisting data ever recorded in history. For the fifth time this year, inventory hit my target level with elevated mortgage rates.

Mortgage rates had a chance to break to new highs this year, but the Federal Reserve took a moderate tone at the last Fed meeting. We saw the benefit of lower mortgage rates with the last two existing home sales reports, which showed growth. Then mortgage rates rose, facilitating five weeks of negative purchase application data.

We survived jobs week and Federal Reserve Chairman Jerome Powell talking to Congress, with mortgage rates ending the week below 7%. But will mortgage rates keep heading lower? Mortgage rates and the 10-year yield The 10-year yield is the key for all my housing work, so I focus on it religiously. We haven’t broken either yet.

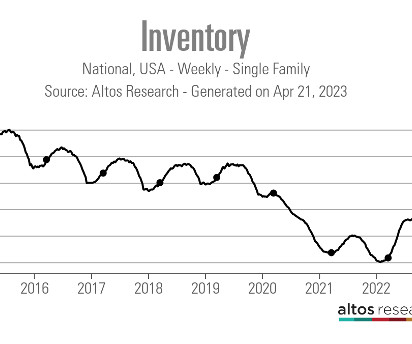

Looking back on 2023, the inventory story was a big surprise even as mortgage rates headed toward 8%, as the data below will show. This didn’t happen once in 2023 — even with rising mortgage rates. What we want to see in 2024 is newlisting data growing in the spring season. Weekly inventory change (Dec.

Mortgage rates have risen recently but they could be much worse than they are today. Mortgage rates and the 10-year yield The 10-year yield is the key for housing in 2024. The most important data line for me, along with mortgage rates , is jobless claims data because I value labor data over inflation. That hasn’t happened.

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? However, mortgage rates have fallen more than 1% since the recent highs, so it’s time to look at the data to explain how to interpret it.

We didn’t see too much volatility in mortgage rates last week, but purchase apps declined in reaction to rates rising two weeks ago. Here’s a quick rundown of the last week: Active listings rose by 8,546 , and newlisting data showed some growth. Again, I am a bit mindful here due to Easter.

Mortgage rates have more than doubled from the beginning of the year and homebuyers facing affordability challenges are increasingly turning to adjustable-rate mortgages (ARMs) to reduce their monthly payments. The Freddie Mac’s index compiles purchase mortgage rates reported by lenders during the past three days.

The one period where this didn’t happen was from 2006-2011, when credit forced Americans to sell, to rent or to be homeless. From NAR : “December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates ,” said NAR Chief Economist Lawrence Yun.

The 2023 housing market faced one of the same roadblocks we saw in 2022: mortgage rates were too high for home sales growth. Here’s my forecast for 2024: 10-year yield and mortgage rates For 2024, the 10-year yield range will be similar to 2023, but with a few different variables to watch. Instead, they closed 2023 at 6.67%.

“The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. Mortgage rates spiked in March, and then the newlisting data started to decline at the end of June. This is the biggest story in housing. .

The 2022 housing market was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Mortgage rates. So where does all that drama leave us for 2023?

Even though this was a beat of estimates, the sales decline trend due to higher mortgage rates and home prices continues. The savagely unhealthy housing market theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . However, it’s not the market of 2002-2011.

To top it all off, we started 2022 at all-time lows, forcing bidding action everywhere until mortgage rates rose. And we aren’t talking about your grandfather’s mortgage rates rising; we went from 2.5% However, with price growth and mortgage rates skyrocketing, the hit to affordability is historic.

We don’t have any data that shows sales are crashing from this low level: this is key when looking at the future because it does give us a place to grow sales as long as mortgage rates fall. This sounds odd to people because mortgage rates went all the way to 8% , and price growth was picking up. Sales faded 6.2% All four U.S.

If we are trending below 4 million — a possibility with newlisting data trending at all-time lows — then we have much weaker demand than people think. This is the reality of our world: total active listings are still near all-time lows and demand so far has been stable since Nov. Now if we get a few sales prints above 4.6

This is why we brought HousingWire Lead Analyst Logan Mohtashami, Kate Amor, senior vice president and head of enterprise products at Guaranteed Rate , and Arjun Dhingra, who lead sales and business development at All Western Mortgage , together for a preview of the information you can expect to hear at HousingWire Annual in Austin Texas, from Oct.

I don’t need to see total active listing get back to the historical range of 2-2.5 Newlistings are declining now. Inventory is always seasonal, but the decline in newlistings this year was not what I wanted to see. This is not encouraging news at all, in my view. From Redfin.

With rates trying to reach equilibrium after their nosedive in 2020, everyone has had to accept that pandemic-era rates are a thing of the past and therefore higher monthly mortgage payments are here to stay. 2023 produced the lowest number of home sales since 2005 with the exception of 2011. The opposite is happening now.

As interest rates sought to stabilize following their sharp decline in 2020, both buyers and sellers had to acknowledge the end of the era of historically low pandemic-induced rates, and the beginning of higher monthly mortgage payments. This hesitancy, spread over two years, has resulted in the lowest number of newlistings since 2000.

You can see this is the second year in a row that sales have been down since the 2020 COVID market, but now in 2023, sales are the lowest they’ve been since 2011. Consequently, we’re witnessing the lowest number of newlistings since 2000. Will the 2024 Real Estate Market Improve? A lot to digest.

Many sellers hesitated to list their properties due to the low pre-pandemic mortgage rates, but increased market activity emerged driven by necessity and life changes, making competitive pricing crucial. increase in newlistings. The 5% rise ended 2024 with 11,155 pending sales compared to 10,911 the previous year.

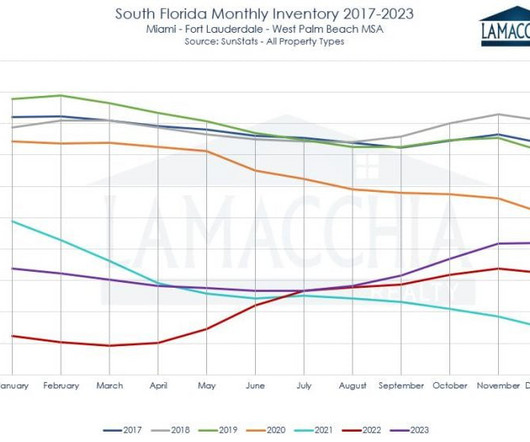

In the chart below you’ll see that the number of single-family homes sold is the lowest it has been in South Florida since 2011. 2023 Sees the Lowest Number of Homes Listed in Fifteen Years There was a 10% decrease in the number of newlistings compared to 2022, with 113,883 homes listed in South Florida, down from 126,545.

Many sellers were reluctant to list due to low pre-pandemic mortgage rates, but increased activity emerged from necessity and life changes , with competitive pricing becoming essential. rise in the number of listings. Sellers had been hesitating to list because they wanted to hold onto their pandemic era rates.

Why are home prices still rising even as mortgage rates have gone higher? A number of people predicted that home prices would experience a steep drop as mortgage rates rose, but that’s not what has happened. This is not a new idea — I’ve been dealing with people predicting a housing crash since 2012.

Many sellers were hesitant to list their properties due to low pre-pandemic mortgage rates, but increased market activity emerged out of necessity and life changes , making competitive pricing essential. Many sellers, hesitant to part with their pandemic-era mortgage rates, had kept inventory tight, leaving buyers with limited options.

Many homeowners were reluctant to put their properties on the market due to the attractive low mortgage rates secured before the pandemic. 2024 Listings Rise for the First Time in Two Years Connecticut has experienced a steady decline in listings since 2015. increase in newlistings. Pending Sales Decreased by 1.1%

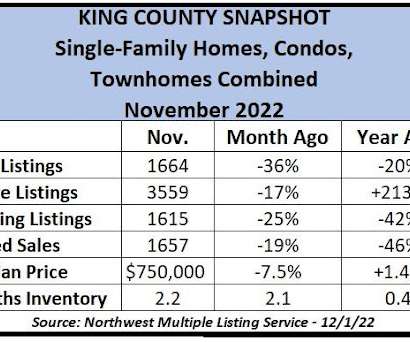

Sales activity across the county is at historic lows; no October has experienced fewer listings in King County – not even close – since at least 1992 when records were first archived online. Newlistings for all home types in King County stood at 2157, a whopping 25% drop from September to October. Closed sales fell 0.9%

This year’s “cold down” is stark, with 36% fewer newlistings and about 26% fewer homes under contract (Pendings) for all King County home types combined as well as single-family structures alone – and that’s simply from October to November. Does this signal a peak in mortgage rates or a temporary blip? Prices declined 5.4%

If you have access to emergency funds – a 401(k), pension, gift money from friends or family, or restricted stock units (RSUs) for some tech employees – consider using them toward a new home purchase. million mortgages in Q2, a 3% drop from Q1, marking the first time since early 2020 that the total number of home mortgages decreased.

Between 2011 and 2019, the median household income in our area increased by about 34% but housing prices jumped 78%. That’s where buyers are paying about 42% more in their monthly mortgage payments for the same house today than they did a year ago. It has also set its sights on rezoning portions of the city to increase housing density.

The Federal Reserve, which has been buying mortgage-related securities for more than a year to artificially keep interest rates low, has signaled a desire to taper its bulk purchases within the next month or so. A 30-year mortgage in our area could be had for about 3.125%, up from about 2.875% a month ago. Newlistings are up 6.3%

The King County housing market has seen inventory increase by 55% in the past month, while the number of homes going under contract fell 22% from May to the lowest June level since 2011. annualized for May – mortgage rates will remain high. annualized for May – mortgage rates will remain high. for 30-year conventional financing.

That’s up from 36% of sales in 2022 but far from the peak this century of 45% in 2011, according to ATTOM. >> MAY HOUSING UPDATE Even after a few weeks of mortgage rate jumps, the Seattle/King County housing market is displaying surprising strength. .

The rate of homes hitting the market was also about one-third stronger than in January 2024 and, at 2533 newlistings, it is the most of any January in four years. That is quite a rebound from late 2024 when only 950 listings hit the market for all home types single-family, townhomes and condos combined. since Christmas.

However, I will give you all the charts to show Uncle Dave that housing credit doesn’t look like it did in 2008 because the qualified mortgage (QM) law makes that impossible. None of that action has been happening for 14 years because the credit market changed after the 2010 qualified mortgage rule.

Home prices have remained firm over the last two months, even with higher mortgage rates and inventory data. I want to show you how the data changed with mortgage rates heading toward 6% so the next time this happens, we have a better idea of what to expect in the housing market. I have long believed that it’s rare in the U.S.

Not to sound like a broken record but, along with seasonal consumer habits in which school, raking leaves and Seahawks football occupy our attention, stubbornly high mortgage rates have kept many prospective home buyers out of the marketplace – except for one fleeting moment. More on interest rates in a moment.) since the Sept.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content