This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Let’s look specifically at the current market data compared to 2011. Why choose 2011? The housing bubble crash years of 2008-2011 saw a surge in foreclosures due to the lack of selling equity and this also profoundly impacted housing demand. Last week in 2011, 396,955 homes hit the market without a contract.

The rules of supply and demand economics always end up winning and weekly newlisting data is key. Newlisting data is growing year over year, but it will be the second-lowest newlisting data ever recorded in history. This contract data will grow if mortgage rates head lower and stay lower.

The one period where this didn’t happen was from 2006-2011, when credit forced Americans to sell, to rent or to be homeless. During that period, we saw newlisting data decline. The Federal Reserve did not like the homebuying atmosphere during COVID-9, especially the non-contingent buying contracts.

Our housing market tracker counts weekly active single-family listings, those homes that aren’t in the contract, and the raw available number of homes for sale. This is why the Altos Research numbers we cite are always smaller than the NAR numbers, which accounts for all home types and those in contract.

17-24), Inventory fell from 437,282 to 430,395 The recent inventory bottom was in 2022 at 240,194 The inventory peak for 2023 was 569,898 For context, active listings for this week in 2015 were 958,304 Newlistings data Newlistings data is growing year over year and increasing week to week, but I wish we were seeing more significant growth.

From NAR Research : “Total existing-home sales notched a minor contraction of 0.4% Existing home sales have more legs to go lower, especially now that newlisting data is falling. However, it’s not the market of 2002-2011. from July to a seasonally adjusted annual rate of 4.80 million in August.”

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2023 compared to 2022 and discusses what is predicted to unfold in 2024. Lowest number of homes listed in recorded history, decreased by 18.7% Average prices for closed sales increased by 3.4%

This report, the first one we are publishing for Rhode Island, examines sales, average prices, the number of active listings, and listings under contract for 2023 compared to 2022. Lowest number of homes listed in recorded history, down 19.5% The number of homes placed under contract decreased by 19.3%

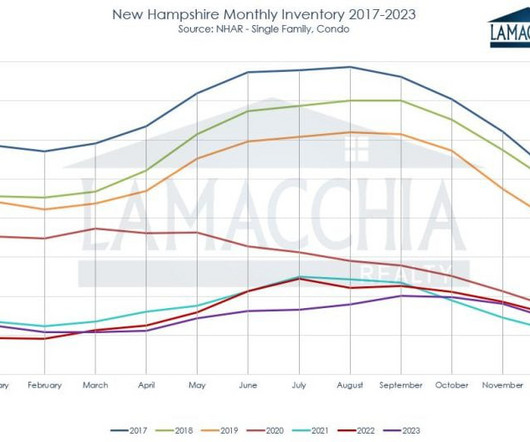

This report breaks down state-wide sales (previous years mostly covered Southern NH and the Lakes Region ), average prices, the number of active listings, and how many listings went under contract for 2023 compared to 2022, and discusses what is predicted to unfold in 2024. Average prices for closed sales increased by 7.2%

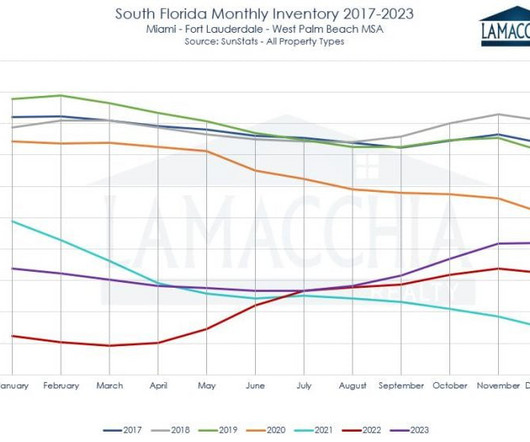

The 2023 South Florida real estate market, like national trends, saw a decrease in sales, an increase in prices, and a decrease in the number of homes listed and placed under contract. The number of homes listed decreased by 10% The number of homes placed under contract decreased by 14.1%

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. The number of homes listed increased by 7.7% The number of homes placed under contract (pending) increased by 4.2%

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. The number of homes listed increased by 10.1% increase in newlistings.

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. The number of homes listed increased by 10.0% The number of homes placed under contract (pending) increased by 3.4%

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. The number of homes listed increased by 2.9% The number of homes placed under contract (pending) decreased by 1.1%

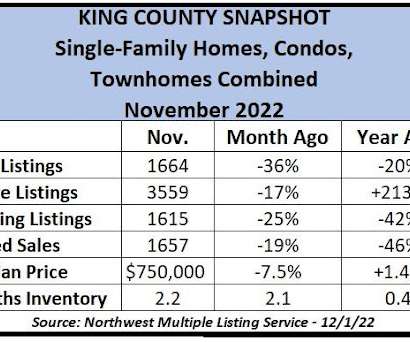

This year’s “cold down” is stark, with 36% fewer newlistings and about 26% fewer homes under contract (Pendings) for all King County home types combined as well as single-family structures alone – and that’s simply from October to November. A little more than a third of inventory is under contract. Prices declined 5.4%

Most notably, it’s the first time mortgages declined from Q1 to Q2 since 2011, according to ATTOM Data Solutions. averaged a 17% home-price rise from Q2 of 2020 to Q2 of 2021 and prices have risen nationally each quarter since Q3 of 2011. >> The pandemic seriously affected U.S. New data show this subset of buyers accounted for 2.8%

Between 2011 and 2019, the median household income in our area increased by about 34% but housing prices jumped 78%. That includes 621 fewer Pending contracts in April 2022 than the previous April, as the net number of newlistings remains on average lower than in years past. List price: $3.495M ($782/sq.

That’s up from 36% of sales in 2022 but far from the peak this century of 45% in 2011, according to ATTOM. >> We are seeing more homes for sale in submarkets – except for Mercer Island and Woodinville, where active listings are down 30%+ – compared with a year ago. . >> All-cash purchases accounted for 38% of U.S.

The gross-flipping profit of $67,000 in Q2 translates into a 34% return on investment compared to the original acquisition price, its lowest point since Q1 of 2011, when the housing market was recovering from a price slump brought on by the Great Recession. Newlistings are up 6.3% in Q2, down from 6.8% OCTOBER HOUSING UPDATE.

The King County housing market has seen inventory increase by 55% in the past month, while the number of homes going under contract fell 22% from May to the lowest June level since 2011. While the number of newlistings in June jumped 8.2% The fresh data show a clear slowing of the housing market.

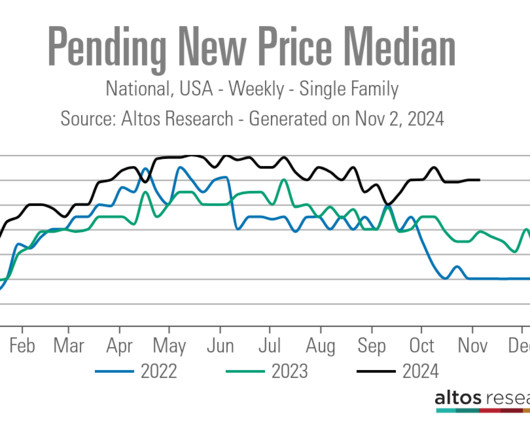

The rate of homes hitting the market was also about one-third stronger than in January 2024 and, at 2533 newlistings, it is the most of any January in four years. That is quite a rebound from late 2024 when only 950 listings hit the market for all home types single-family, townhomes and condos combined.

Pending contracts First, we must realize that we are working with the third calendar year of the lowest home sales ever recorded, once you adjust that number to the workforce. Newlistings data had a slight increase this week from 60,066 to 60,819. To this date, these principles still apply.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content