This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Right after the Great Recession, between 2009 and 2011, buyers viewed a median of 12 homes before purchasing, as inventory was plentiful. From 2004 to 2006, during the housing boom years, even though homes were moving at a rapid pace, buyers typically looked at nine homes.

points, but has steadily recovered over 60% of its COVID-19 pandemic loss when April’s HPSI hit its lowest reading since November 2011. While the state of the market shines brightly for prospective buyers and sellers, the economy overall is showing some slight hesitation. Compared to this time last year, the HPSI is still down 7.1

Now we are looking at a two- to three- business-day process and the buyer may not like the numbers they get back.” For some buyers, surprisingly high insurance premiums are causing them to second-guess the property they have selected. “I There has also been an uptick in the strength and scale of natural disasters.

points, but has recovered more than half of its early pandemic-period decline when April’s HPSI hit its lowest reading since November 2011. August’s HPSI survey revealed both a confident seller’s and buyer’s market, however, Fannie Mae reported September buyers showing more hesitancy.

The merger combines the strengths of both companies, allowing us to better support agents, buyers, and sellers in the Dayton area while enhancing our leadership in the market.” Alliance Group Realty was founded in 2011 by Bob Clarkson and currently has over 70 agents.

First-time home buyers, especially millennials and Gen Xers, are facing an uphill battle when looking for a home, partly because baby boomers […] are planning to stay put.” The RMMI increased precipitously between 2011 and 2021. Boomers own 35.6% Despite owning 35.6% of the total population of the city’s metropolitan population.

metropolitan areas since 2011. Meanwhile, buyers offer bigger down payments to lessen the cost of monthly payments In September, buyers were typically putting down 16.1% In those cities, the typical buyer put down 25% of the purchase price. and 20.3%, respectively. respectively. in April 2023.

Since 2011, the number of existing single-family homes for sale has declined more than 30%. As Candace Taylor writes in The Wall Street Journal , “These days, buyers eschew the large, ornate houses built in [previous] years in favor of smaller, more-modern looking alternatives.”

In 2011, only 13% of homebuilders worried about the cost of labor, versus 87% in 2019. On the bright side, attracting buyers to the market last year was not a widespread difficulty, but homebuilders fear that might change. Rising inflation came in second among the most widespread problems of 2023, cited by 83% of builders.

The monthly housing supply for the existing home sales has only gone above six months during the bust years after the housing bubble (2006-2011). This period was also during a lull in our prime-age labor force growth, so demand was soft during the years 2006-2011. million jobs lost. Hard pass. It could also function as a jobs program.

The NAHB/ HMI report is based on a monthly survey of NAHB members, in which respondents are asked to rate both current market conditions for the sale of new homes and expected conditions for the next six months, as well as traffic of prospective buyers of new homes.

This contributes to fewer homes being listed , as well as fewer potential buyers, and may lead to a growing share of listings having to cut prices to meet the reduced demand.” This is the slowest quarter of growth since Q4 2011. We expect these trends to continue in the coming months,” Duncan said. in Q3 2022.

In this testimony given before congress in March of 2011 Calabria stated this: “ Reducing the competitive advantage of Fannie Mae and Freddie Mac via a mandated increase in their guarantee fees would both help to raise revenues while also helping to “level the playing field” in the mortgage market. It’s time to take the gloves off.

Currently, we are in a much different housing recession than what we had from 2005-2011. Now that demand is falling, the builders will take their time finishing these homes to ensure they have buyers ready to move in once the homes are completed. The credit cycle looks much different now than the build-up from 2002-2005.

in the fourth quarter of 2020 to its lowest point since the second quarter of 2011. homes flipped in the first quarter of 2021, 10 percent were sold to buyers using loans backed by the Federal Housing Administration (FHA), down from 11.6% The gross flipping return on investment was down from 41.8% Of the 32,526 U.S.

In comparison, in 2011, homes took 96 days to sell. . Notably, the market has contracted as fewer buyers can afford to purchase in today’s market with the rise in interest rates and the continual rise in home prices. One way to understand the competitiveness of the market is to look at buyers who are waiving contingencies.

“Fall could bring more declines in home prices as more buyers bow out.” The year 2023 is shaping up to be the first year since 2011 when annual existing-home sales will come in below 4.5 However, month-over-month, the median home price nationally was flat in August, Bright MLS Chief Economist Lisa Sturtevant noted.

homebuying season, Zillow’s latest monthly report finds that home listings are beginning to pile up as buyers step back from the peak of home shopping season earlier than usual. “A Sellers are increasingly cutting prices to entice buyers struggling with affordability,” said Dr. Skylar Olsen, Chief Economist for Zillow.

Though price growth has cooled and prices have begun to come down, high and still climbing mortgage rates mean many of today’s buyers face larger home payments than they would have when home prices were at their peak Hannah Jones, economic data analyst at Realtor.com. Buyers, builders and sellers take a step back as inflation persists .

From NAR: First-time buyers were responsible for 29% of sales in December; Individual investors purchased 16% of homes; All-cash sales accounted for 29% of transactions; Distressed sales represented 2% of sales; Properties typically remained on the market for 29 days. This is a positive for housing in 2024 as most sellers are buyers.

After months of fending off an unsolicited takeover bid by two of its significant investors, CoreLogic today confirmed that it is looking for a buyer. “In CNBC also cited a source that said CoreLogic “has already signed a non-disclosure agreement with at least one potential buyer.”

The one period where this didn’t happen was from 2006-2011, when credit forced Americans to sell, to rent or to be homeless. From NAR : “December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates ,” said NAR Chief Economist Lawrence Yun. Also, this is what the Federal Reserve wants.

However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. These two factors were happening from 2006 to 2011 and added supply to the market. You don’t want to overcomplicate this topic. Credit stress was evident from 2005 to 2008.

However, persistently high mortgage rates pose a significant affordability challenge to buyers and sellers (not to mention the workers of a trillion dollar-plus industry). In July, 26% of existing homes sold to cash buyers while 7% of new homes sold to cash buyers. said Sturtevant.

The last time we had a stressed seller market was when national home prices crashed in 2008-2011 and even with more inventory , we’re nowhere close to those levels. 2009 281,734 2010 345,146 2011 396,955 2012 318,041 Weekly housing inventory data I am almost ready to give an A grade for inventory this year.

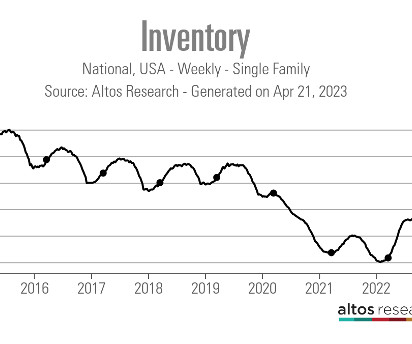

Below is the monthly supply of existing homes from 1999-2014, where you can clearly see the growth in monthly supply from 2006-2011. As you can in the chart below, the monthly supply data shows we have no forced selling action in the housing market today, unlike the 2006-2011 period. I believe that number is four months.

In high-demand areas where only one or two properties come on the market, maybe in a month, we’re seeing [buyers paying] upwards of $100,000 to $150,000 over asking price.”. Notably, in 2011, existing home prices in Ada County were at $160,113. Now, in 2020, median existing home prices are at $410, 414.

From NAR : First-time buyers were responsible for 31% of sales in November; Individual investors purchased 18% of homes; All-cash sales accounted for 27% of transactions; Distressed sales represented 1% of sales; Properties typically remained on the market for 25 days. So, let’s not make that mistake in 2024. Unsold inventory sits at a 3.5-month

A traditional primary resident seller is also a buyer, which means if they don’t list, they’re not just taking a potential home to be bought off the table — they’re taking a future sale off the books as well. However, it’s not the market of 2002-2011. From NAR Research : “Total existing-home sales notched a minor contraction of 0.4%

.” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. This explains why total active listing inventory data has been stable over the decades, with the exception of 2006-2011, when those forced distressed credit home sellers couldn’t buy.

After more than a decade of under-building relative to population growth, there are simply not enough affordable entry-level and first-time move-up options available for buyers. From February 2011 to April 2022, mortgage rates never rose above 5%, making the cost to borrow money and buy a home very cheap. million homes.

For some historical context, back in 2011, this data line was 101 days. NAR: First-time buyers were responsible for 28% of sales in March; Individual investors purchased 17% of homes; All-cash sales accounted for 27% of transactions; Distressed sales represented 1% of sales; Properties typically remained on the market for 29 days.

It launched an interactive media platform as well in the fall of 2021, called Glocaly, which serves as a listing and marketing exchange for matching sellers and buyers of condos. Between 2011 and the end of 2021, Japanese companies operating in Texas accounted for a total of some $6.8

On the other hand, investment-return decline during this year’s summertime home-selling season marked the largest quarterly downturn since 2011, with the third-quarter reversal also marking the first since 2010 that seller returns went down from the second to third quarter.

million, the equilibrium balance between a buyer and seller marketplace that has been here for four decades. Only from 2006-2011 did we see this break due to forced sellers who couldn’t buy homes. NAR: Total Inventory levels 1.22 million Historically inventory levels range between 2 million and 2.5

Experienced real estate investors often say that there are opportunities in every market — whether prices are rising or falling, whether the trends lean towards a buyers’ market or a seller’s market. in 2021, the lowest level of gross margin since the first quarter of 2011, during the Great Recession. in 2020 to 33.2%

In 2011, he founded the innovative brokerage The Agency RE, and he recently launched a real estate agent trade group that aims to serve as an alternative to the National Association of Realtors (NAR). If you analyze how a commission is paid, a commission has always been paid by the buyer, not by the seller.

Last years scenario emerged as buyers buoyed by rising wages, a strong investment market and mostly receding mortgage interest rates competed for a historically tight supply of homes. times the nationwide median in 2011, a point in time right before the housing market began recovering from the Great Recession. in 2023, the U.S.

Moving the needle doesn’t take much since we all know we have buyers ready to go and home sales are at record lows. Weekly new listing data for the last week over several previous years: 2024: 59,243 2023: 50,687 2022: 59,661 For some historical context, new listing data this week in 2011 was 362,248.

Sustained outperformance of the Northeast market was last observed in 2011. The Northeast is the best performing market for the previous nine months, with New York rising 9.4% For the decade that followed, the West and the South held the top posts for performance. growth in active inventory in the housing market in this period.

That was the slowest growth in a calendar year since 2019 and the second-slowest since 2011. There are more homes for sale right now than in recent years and that has led to buyers markets in many areas of the country. In percentage terms, the total value of the U.S. housing market grew 5.2% year-over-year.

“The housing market continues to face headwinds as mortgage rates increase again this week, following the 10-year Treasury yield’s jump to its highest level since 2011,” Sam Khater, Freddie Mac’s chief economist, said in a statement. However, the number of homes for sale remains well below normal levels.”

The Federal Reserve Bank of New York ’s second-quarter 2022 Household Debt and Credit Report shows that limits on HELOCs jumped by $18 billion in the second quarter of this year, “the first substantial increase in HELOC limits since 2011,” and an indicator of an increase in new originations. We’ll probably trade a little over $1.2

As you can see above, the monthly supply in 2006, 2007, 2008, 2009, 2010, and 2011 was above 6 months on average, running at 8.71 history are ages 26-32, and the first-time median home buyer age is now 33. Don’t forget the mortgage buyer is the most significant homebuyer out there; they matter the most. We are currently a t 1.7

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content