This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The rules of supply and demand economics always end up winning and weekly newlisting data is key. Newlisting data is growing year over year, but it will be the second-lowest newlisting data ever recorded in history. For the fifth time this year, inventory hit my target level with elevated mortgage rates.

After 2010, qualified mortgage laws were in place, meaning everyone getting a mortgage has to be able to repay the loan. You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008.

The recent CoreLogic Homeowner Equity Insights report for Q3 shows a continued positive trend of a lack of underwater mortgages in America today. Underwater mortgages where borrowers owe more on their home than what it is worth pose a risk of foreclosure and hinder people from selling their homes, something that was rampant after 2008.

The 10-year yield is at the same critical point as last year before the Fed went hawkish and sent mortgage rates to 8% and the 10-year yield to 5%. A serious 10-year yield and mortgage rate talk My work on housing moves around the 10-year yield and the economics that move that. Could this happen again?

“The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. Since the credit standards have improved post-2010, we shouldn’t see distressed sellers until a job loss recession happens, even if sales fall noticeably.

The best housing story in 2024 is that inventory is growing — both active inventory and newlistings. With mortgage rates at the current levels, inventory is still below my expectations, but it’s still such a positive story that I had to discuss it on CNBC last week. Still, newlisting data is a positive story.

Today’s housing market suffers from affordability issues due to mortgage rates in the 7s and high home prices. Consider: In the fourth quarter of 2010, 23.1% Newlistings The most significant and glaring difference between 2011 and 2024 is the weekly newlistings data for the peak season.

After seeing disappointing inventory growth two weeks ago , which I chalked up to the Memorial Day holiday, I was hoping for a big push in active listings last week, but that didn’t happen. And, the recent uptick in mortgage rates to almost 7% slowed purchase application data again. Of course, we have a third story in this U.S.

The 2022 housing market was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Mortgage rates. So where does all that drama leave us for 2023?

Home Prices will fall, but don’t expect 2010. There will be two key differences between 2023 and 2010. First, mortgage lending standards have remained high after the last bubble. People can afford to pay their mortgages. The event is exclusively for HW+ members , and you can go here to register. months nationally.

Elevated mortgage rates and high home prices pushed sales of existing homes down again in October to the lowest monthly pace since August 2010. Selma Happ, the chief economist at CoreLogic , said transaction data suggests that existing home sales are leveling off despite the uptick in mortgage rates.

Existing home sales fell in today’s report , which isn’t surprising, but one headline that shocked some people was that home prices are still up year over year, even with higher inventory and higher mortgage rates. From NAR : The median existing home price for all housing types in March was $393,500, an increase of 4.8% All four U.S.

I don’t need to see total active listing get back to the historical range of 2-2.5 Newlistings are declining now. Inventory is always seasonal, but the decline in newlistings this year was not what I wanted to see. This is not encouraging news at all, in my view. From Redfin.

Credit channels and inventory channels both changed after 2010 because of the qualified mortgage laws and the 2005 bankruptcy reform laws. Once mortgage rates rise in this environment, it can lead to big-time demand destruction, which is what has happened. million would mean much better mortgage demand. million in May.

If we are trending below 4 million — a possibility with newlisting data trending at all-time lows — then we have much weaker demand than people think. One thing higher mortgage rates have done for sure is that home-price growth is cooling down noticeably since the big spike in rates. are different post-2010. economy.

As a result, markets were quick to respond, driving mortgage spreads and rates much higher than most experts expected by this time of year. At over 5%, mortgage rates are now the highest they have been since 2010. Mortgage rates should hover around 5%, but there may be more oscillation than we have seen recently.

Even as mortgage rates rose, and affordability was pushed out of reach for many potential homebuyers, there are still sufficient buyers who can afford these prices and these rates. After the mortgage rate spike in September 2022, we got significantly more bearish on home prices for 2023. If mortgage rates increase to the 7.5%

Since 2010, Bluff ton’s population has nearly tripled to about 34,000 making it one of America’s fastest growing towns. According to McGrath, out-of-town buyers and local move-up buyers taking advantage of low mortgage rates have decimated the area’s housing supply. However, this growth has come at a cost. in 2021 to $330,745. “In

Why are home prices still rising even as mortgage rates have gone higher? A number of people predicted that home prices would experience a steep drop as mortgage rates rose, but that’s not what has happened. This is not a new idea — I’ve been dealing with people predicting a housing crash since 2012.

Now that the Federal Reserve has cut interest rates, home buyers should swarm the market with low-interest mortgages …. Consumers considering a change of address are holding out amid forecasts for lower mortgage interest rates in 2025. After the Fed rate cut, mortgage applications jumped 9% in a week. Hold on, there!

November newlistings fell by about half of the previous month’s rate while home prices saw a welcome decline. Even with mostly lower prices, affordability remains the biggest challenge for buyers as mortgage interest rates climbed toward 7%. The number of newlistings tumbled 48% from October and was down 2.7%

Variations between the two years are stark, to say the least: A “re-evaluation” for future buyers can be defined as consumers determining when to jump (or jump back) into the home-search pool as mortgage rates appear stuck around 7.0%. Mortgage rates are high, home prices are high, there’s no inventory.” The county saw a 4.9%

The market is spooking many potential buyers and sellers thanks to stubbornly high mortgage interest rates. fewer newlistings, the rate of sales rose 1.7% fewer newlistings (1998) compared to July and 5.0% At least that’s what some economists have expressed. Only buyers and sellers who must move are doing so.

As interest rates strive to find equilibrium following their sharp decline in 2020, buyers and sellers have had to accept that the era of pandemic-induced low rates is over, ushering in a period of higher monthly mortgage payments. This has led to the lowest number of newlistings since 2010. It has been a vicious cycle.

Annual sales across King County totaled 21,515 homes – down an incredible 24% from the year before and the fewest since 2010 (20,761). And, despite the rise in newlistings, the number of homes still on the market on Feb. Seattle led the way with a 156% increase in newlistings (517) month-to-month and 4.0%

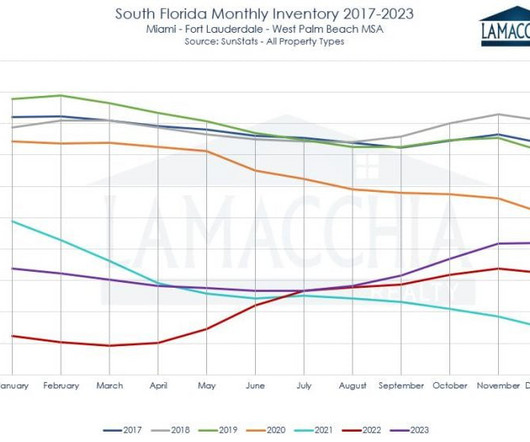

Condo sales are at the lowest point since 2010. 2023 Sees the Lowest Number of Homes Listed in Fifteen Years There was a 10% decrease in the number of newlistings compared to 2022, with 113,883 homes listed in South Florida, down from 126,545.

According to the latest census, the population in Raleigh grew by almost 64,000 residents between 2010 and 2020. 4,840 new apartments were constructed in Raleigh throughout 2021. Statista) The number of newlistings in Raleigh in April 2022 was more than newlistings in January 2022. of a person’s income.

First a look at September’s numbers: A wave of last-chance listings for the year hit the market after Labor Day. That increased newlistings by 7.5% (2884) and available homes on the market by 12% (3602) between Sept. Seattle alone saw a 29% (1213) monthly increase in newlistings. 1 and Oct. on the year.

The optimism comes from signals in economic data that show improving conditions and a likely end to rising mortgage rates in the coming months – a story that we are all looking forward to reading. The Eastside led the way with a 33% drop-off in newlistings (420) and Seattle fell 31% (586). units, a 13-year low. higher YoY.

The region’s real estate scene in 2023 will be remembered for rising home prices and scant newlistings. As the year dims, all eyes fixate on 2024’s potential: a hopeful dance fueled by dreams of lower rates and a wave of new homes for sale. Buyers and sellers tiptoed through caution. Um, bye-bye! The number of U.S.

Many homeowners were reluctant to put their properties on the market due to the attractive low mortgage rates secured before the pandemic. 2024 Listings Rise for the First Time in Two Years Connecticut has experienced a steady decline in listings since 2015. increase in newlistings.

Sales activity across the county is at historic lows; no October has experienced fewer listings in King County – not even close – since at least 1992 when records were first archived online. Newlistings for all home types in King County stood at 2157, a whopping 25% drop from September to October. Closed sales fell 0.9%

The boost in equity was helped most simply by saving more while in “pandemic hibernation” and from many homeowners refinancing mortgages amid generationally low interest rates. >> million loans in forbearance – mortgage payments on pause, most likely for financial reasons during the pandemic. of all mortgages in the country.

That’s where buyers are paying about 42% more in their monthly mortgage payments for the same house today than they did a year ago. home prices, up 14% year over year (YoY) by one measure, and escalating mortgage rates, which have risen about 2.1 The potent combo of rising U.S. home (about $400,000 vs. $880,000 in King County).

At what point will mortgage interest rates peak? While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. When you raise [mortgage] rates to the point they’re at today, it breaks the back of housing.”.

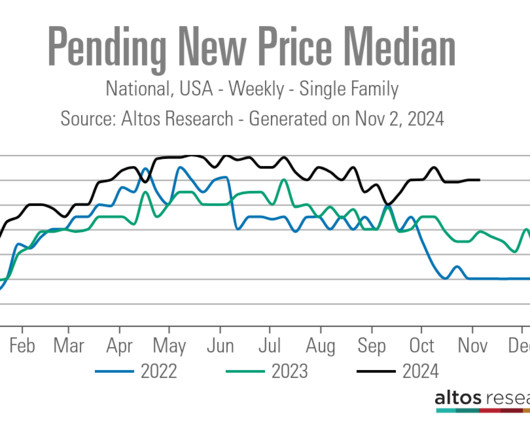

NAR total inventory since 1982: I prefer the Altos Research weekly single-family data to the NAR data because it gives us a fresh look at not only active listing data but newlisting data. The Altos Research newlisting data is essential in tracking the supply aspect of housing, which is why I include it as part of the Tracker.

“That’s a triple whammy hitting potential homebuyers,” notes Len Kiefer, deputy chief economist at Freddie Mac, which buys many of our mortgage loans from lenders. People are looking at higher prices, there’s slim pickings in inventory and now we have higher mortgage rates.”. The new fees will take effect on April 1. “As

That median figure is the smallest measure for a home since 2010 and marks a reversal after a brief increase during the post-Covid building boom. >> First a look at September’s numbers: A wave of last-chance listings for the year hit the market after Labor Day. Seattle alone saw a 29% (1213) monthly increase in newlistings.

Home prices are overheating, mortgage rates are inching up from the start of the year and the supply of homes is in an unseasonable valley – far from its Mt. Today, 37% of all buyers are Millennials and they comprise about 54% of all mortgage applications. of mortgages underwater); Multnomah County (Portland), Ore. points at 34.

Memories of the Great Recession still linger for anyone linked to the real estate industry – including the estimated seven million households that lost their homes to foreclosures around 2008-2010. Adjustable-rate mortgages were cheap and easy to acquire, home prices were artificially inflated and supply plentiful. That leaves about 2.1

The rate today is the same as in the late 1960s, except during the housing bubble of 2008-2010 when ownership rose – and we know how that ended up! Co-buying comes with marriage-like considerations, such as how to split mortgage payments and domestic concerns. >> Forty-five percent of residential mortgages in the U.S.

The index showed a growing difficulty to afford a home even while household income and mortgage rates improved compared to last year. And, Seattle’s attempt to force building developers to incorporate more affordable homes within their new residential endeavors yielded only 21 units in 2020 out of a swell of 224 construction projects.

However, I will give you all the charts to show Uncle Dave that housing credit doesn’t look like it did in 2008 because the qualified mortgage (QM) law makes that impossible. None of that action has been happening for 14 years because the credit market changed after the 2010 qualified mortgage rule.

Home prices have remained firm over the last two months, even with higher mortgage rates and inventory data. I want to show you how the data changed with mortgage rates heading toward 6% so the next time this happens, we have a better idea of what to expect in the housing market. I have long believed that it’s rare in the U.S.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content