This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Economists and housing experts say mortgage lending standards will likely loosen in 2021, despite the increased risk of delinquencies ahead. The post Why mortgage lending standards will ease in 2021 appeared first on HousingWire. Such a scenario illustrates the growing disparities in the U.S. housing market.

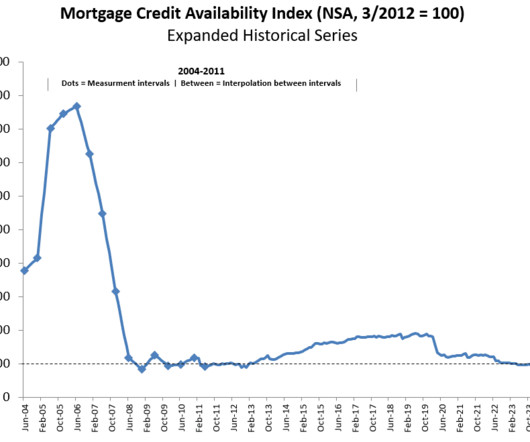

While increases in the index point to looser credit, a decrease in the MCAI suggests tighter lending requirements. Conventional lending programs that are not subject to conforming loan restrictions are examined by the Jumbo MCAI, whereas those that are are examined by the Conforming MCAI.

The study claims that the crisis can be traced back to the early 2000s when subprime lending activities were prevalent. The resulting housing market crash and the Great Recession led policymakers to overcorrect by tightening mortgage lending standards and limiting funds for new construction.

million in 2010. housing units, down slightly from 0.25% in 2023, and down from 0.36% in 2019, and down from a peak of 2.23% in 2010. Foreclosure filings in 2024 were also down 89% from a peak of nearly 2.9 The 322,103 properties with foreclosure filings reported on in 2024 represented 0.23% of all U.S.

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. One of the biggest reasons home sales crashed from their peak in 2005 was that the credit available to facilitate that boom in lending simply collapsed. The short (and long) answer is no, not a chance.

Chase Home Lending , the consumer and commercial banking arm of JPMorgan Chase & Co. , Dimon further suggested a “candid review” of the thousands of new rules implemented since the passage of the Dodd-Frank Act in 2010. has raised its closing guarantee from $5,000 to $20,000 until July 27, 2024, the bank announced on Thursday.

Richardson Economic Consulting LLC , “Socioeconomic Consequences,” found that a key factor contributing to the decrease of affordable mortgages for low- and moderate-income families is the 2010 Dodd-Frank Act , which made small-dollar mortgages relatively more expensive to process than larger loans. particularly in low-income communities.

Between lack of inventory, record high prices, rising interest rates and significant affordability issues, challenges for the purchase and refi markets are leading to a time of opportunity for home equity lending. In the last five years alone, homeowners have gained, on average, $125,000 in equity on their properties.

Post-2010, lending standards in America became normal again, and while I still believe they’re very liberal, they’re sane. What happened post-2010 is that exotic loan debt structures that don’t provide long-term fixed debt products left the system. I can’t emphasize enough how critical this aspect is to the American economy.

While an increase in the index signifies loosening credit, a decrease in the MCAI suggests tightening lending rules. Conventional lending programs that come inside conforming loan limitations are examined by the Conforming MCAI, whereas conventional programs outside of conforming loan limits are examined by the Jumbo MCAI.

In addition to the bond market yield action, responsible lending post-2010 gave me confidence that forbearance was not going to be the negative issue that many had hoped for. While lending standards were never tight in American in the 21st century, they were very responsible post-2010.

Scarpati previously served as the company’s senior vice president of wholesale lending. Scarpati has served at FOA since 2010 in various roles, and he is the first occupant of this new C-suite executive position.

Banks moved to ease lending standards for most mortgage loan products during the second quarter, according to a loan officer opinion survey published this week by the Federal Reserve Board. Overall, feedback from participants – 75 domestic banks and 22 U.S.

In 2010, CoreLogic’s national data in the fourth quarter revealed that a shocking 23.1% However, the situation has significantly improved since then, thanks to the Qualified Mortgage rule (QM) that was implemented in 2010. Most homeowners aren’t in financial distress as their cash flow has been solid since 2010, thanks to that QM rule.

While increases in the index point to looser credit, a decrease in the MCAI suggests tighter lending requirements. Conventional lending programs that are not subject to conforming loan restrictions are examined by the Jumbo MCAI, whereas those that are are examined by the Conforming MCAI. In August, the MCAI increased by 0.9%

First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards. If we dig a little deeper into homeowners’ balance sheets, we see that since 2010, cash flow and loan quality of mortgage holders were excellent. The rest of this content is for HW+ members.

This is because after 2010, the loan profiles of mortgage seekers before and during the COVID crisis have been, in a word, excellent– the best loan profiles that I have ever seen in my 24 years of lending experience. The rest of this content is for HW+ members. Join today with an HW+ Membership !

The company claims on its website that the total value of homes it has appraised is over $517 billion since 2010. Also, its total value of transactions closed and recorded since 2010 is over $436 billion. The acquired company will operate as a standalone division.

While increases in the index point to looser credit, a decrease in the MCAI suggests tighter lending requirements. Conventional lending programs that are not subject to conforming loan restrictions are examined by the Jumbo MCAI, whereas those that are are examined by the Conforming MCAI. In July, the MCAI increased by 3.3%

Michael Gevurtz, CEO and Founder, Bluebird Lending This article originally appeared in the February 2025 edition of MortgagePoint magazine, online now. Since 2010, Michael has focused on opportunities in the revitalization of Philadelphias emerging neighborhoods.

One of the unsung heroes of the most prolonged economic and job expansion ever recorded in history was the passing of the 2005 Bankruptcy Reform Act and the 2010 qualified mortgage rule under Dodd-Frank. Both these laws paved the way for more responsible lending and a more responsible consumer. Today, we are at 1.25

Since 2010, Bank of America , Wells Fargo , and JPMorgan Chase have all paid multi-million-dollar settlements in response to U.S. Justice Department charges of fair-lending violations. As with many industries, the mortgage-lending market has increasingly moved online.

While increases in the index point to looser credit, a decrease in the MCAI suggests tighter lending requirements. Conventional lending programs that are not subject to conforming loan restrictions are examined by the Jumbo MCAI, whereas those that are are examined by the Conforming MCAI. In June, the MCAI increased by 1.0%

. “With a similar culture and alignment of values, Veritex has helped Thrive grow by understanding our business and assisting Thrive with tailored financing, including construction warehouse lending. The investment in Thrive comes amid a wave of M&A activity in the mortgage lending space. It posted net income of $31.8

Prior to her seven-year stint at the Federal Home Loan Bank of Pittsburgh, from 2013 to 2014 Anderson worked as an attorney at Relman, Dane & Colfax PLLC , specializing in fair lending counseling and compliance. Before that, she worked at Ballard Spahr in public finance and housing. It will not be her first time at Fannie Mae.

The Consumer Financial Protection Bureau (CFPB) has appointed two veteran regulators to lead enforcement and supervision, the latest indication that Director Rohit Chopra will heavily prioritize fair lending and racial equity issues. He also had a stint as director at the Center for Responsible Lending. a legal defense nonprofit.

Harley founded Fathom Realty in 2010, and the company has since expanded to Fathom Holdings. It encompasses brokerage, mortgage, title, insurance and technology companies like Real Results, Verus Title and Encompass Lending.

The fair housing organization argued that Old National should have “ been especially attuned to the country’s fair lending laws and the need to make loans available in communities of color due to its 2018 purchase of KleinBank.”

“Inaccurate HMDA data can make it difficult for the public and regulators to discover and stop discrimination in home mortgage lending or for public officials and lenders to tell whether a community’s credit needs are being met,” the CFPB said in a release. ” Washington Federal is located in Seattle.

Kicking off this week’s string of senior leadership hires, InterLinc Mortgage Services promoted to CEO Gene Thompson, who has served as president since 2010. Thompson started his mortgage career as an originator, working his way up to regional manager, eventually starting his own firm, Texas Capital Lending.

Home Prices will fall, but don’t expect 2010. There will be two key differences between 2023 and 2010. First, mortgage lending standards have remained high after the last bubble. The event is exclusively for HW+ members , and you can go here to register. Median home prices have declined for four straight months.

Flagstar Bank and the FinTech Consortium revealed that fintech startups Home Lending Pal , Stavvy and Real Key are the latest initiates to the companies’ ongoing MortgageTech Accelerator program. in 2010 and 2011. The company’s cloud-based platform also automates the document collection, verification, and review process.

The lawsuit alleges that, between 2010 and 2018, Wells Fargo failed to detect errors in its automated system to determine whether consumers in default would be eligible for loan modifications with Fannie Mae or Freddie Mac , or under the U.S. The benefit distribute date is currently scheduled to occur on March 15.

She joined Union Savings Bank as its regional vice president in 2010 and the Ohio Mortgage Bankers Association as its president in 2020, after being a member there for more than 10 years. PrimeLending currently operates in all 50 states in the U.S.

A decrease in the MCAI suggests tighter lending rules, whilst an increase in the index indicates looser credit. Mortgage credit availability increased in May, according to the Mortgage Credit Availability Index (MCAI) , a report from the Mortgage Bankers Association (MBA) based on data from ICE Mortgage Technology. The MCAI increased by 0.1%

A report by the Latino Donor Collaborative found that Latino GDP grew 72 percent faster than non-Latino GDP over the entire period from 2010 to 2018. Together with a pricing model and strong fair lending protections, the NAHREP said expanded access to credit opportunities can arise for Latinos.

Well, it isn’t 2008, but this type of loan does have risk — and it’s the risk that is traditional among all late economic cycle lending in America when the loan requires low or no downpayment. Are we really doing those types of loans and promoting homeownership again without understanding the risks?

Today, it’s the complete opposite story: the 2005 bankruptcy reform laws and the 2010 Qualified Mortgage laws laid the foundation for the best housing credit profiles recorded in U.S. We now have real credit risk, as prices are falling from the peak in some areas; late-cycle lending risk is always traditional.

Mortgage banks act as intermediaries between borrowers and the government entities that set guidelines for mortgage lending. In 2021, non-depository lenders originated mortgages representing 91% of all FHA forward business, up from 57% in 2010, per HUD’s most recent annual report to Congress.

Mozilo avoided working with subprime loans until the late 1990s, when after noticing that his firm was losing business to competitors, Countywide embraced the type of subprime mortgage lending that eventually led to the housing crisis in 2008. Mozilo settled with the SEC in October 2010 for $67.5 And they did it at a massive scale.

Mortgage compliance attorneys interviewed by HousingWire said the program, dubbed “Control Your Price,” raises potential areas of concern across three subjects: rules that govern loan officers’ compensation; fair lending; and unfair, deceptive and abusive acts and practices. ” According to Selden, the rule is clear.

percent recorded in the fourth and first quarters of 2010 and 2011, and it has remained constant from previous quarters. In addition, FHFA must collect information on the creditworthiness of borrowers, including a determination of whether subprime and nontraditional borrowers would have qualified for prime lending. A further 0.6%

As you can see above, the monthly supply in 2006, 2007, 2008, 2009, 2010, and 2011 was above 6 months on average, running at 8.71 housing market, and we should never ease lending standards to try to facilitate demand. Lending standards are already liberal enough, so we don’t need to go down that avenue. Time will tell on that.

The community lending segment has experienced impressive growth over the last 10 years. From 2010 to 2016, for instance, the top five depositories saw mortgage origination fall from 64% to 25% , a loss of ~$500 billion in originations.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content