This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

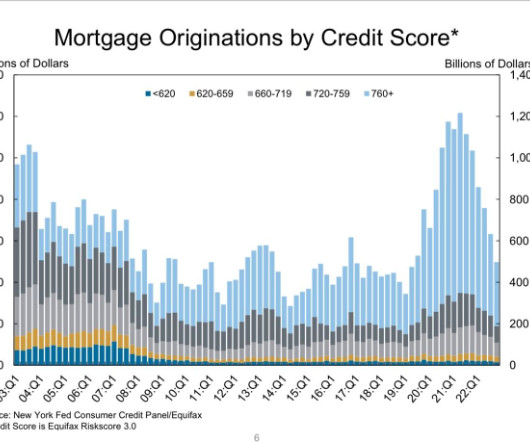

The study claims that the crisis can be traced back to the early 2000s when subprime lending activities were prevalent. The resulting housingmarket crash and the Great Recession led policymakers to overcorrect by tightening mortgage lending standards and limiting funds for new construction.

Economists and housing experts say mortgage lending standards will likely loosen in 2021, despite the increased risk of delinquencies ahead. housingmarket. The post Why mortgage lending standards will ease in 2021 appeared first on HousingWire. Such a scenario illustrates the growing disparities in the U.S.

million in 2010. housing units, down slightly from 0.25% in 2023, and down from 0.36% in 2019, and down from a peak of 2.23% in 2010. The continued decline in foreclosure activity throughout 2024 suggests a housingmarket that may be stabilizing, even as economic uncertainties persist, said Rob Barber, CEO at ATTOM.

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. A few months ago, I was asked to go on CNBC and talk about why I call this a housing recession and why this year reminds me a lot of 2018, but much worse on the four items above.

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. One of the biggest reasons home sales crashed from their peak in 2005 was that the credit available to facilitate that boom in lending simply collapsed. The short (and long) answer is no, not a chance.

This article is part of our 2022-23 HousingMarket Forecast series. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the top predictions for this year, along with a roundtable discussion on how these insights apply to your business.

Post-2010, lending standards in America became normal again, and while I still believe they’re very liberal, they’re sane. What happened post-2010 is that exotic loan debt structures that don’t provide long-term fixed debt products left the system. I can’t emphasize enough how critical this aspect is to the American economy.

One of the reasons that I moved into the “team higher mortgage rate” camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housingmarket savagely unhealthy. million — once that happens, I can take the unhealthy label off the housingmarket.

According to the Mortgage Bankers Association (MBA), theMortgage Credit Availability Index (MCAI)indicates that mortgage credit availability rose in Februarydespite economic changes and housingmarket uncertainty. While an increase in the index signifies loosening credit, a decrease in the MCAI suggests tightening lending rules.

However, there are a number of attention-grabbing headlines, which unfortunately only compare today’s housingmarket to the very recent history of the last two years. It is always good to know where we are with the real estate market, but it is essential to keep all data in historical perspective. . Historically 2.5

One of the most alarming aspects of the housing bubble crash was the staggering number of Americans who were underwater on their homes. In 2010, CoreLogic’s national data in the fourth quarter revealed that a shocking 23.1% This is the risk of late-cycle lending in the U.S., of homes that have a mortgage.

In addition to the bond market yield action, responsible lending post-2010 gave me confidence that forbearance was not going to be the negative issue that many had hoped for. While lending standards were never tight in American in the 21st century, they were very responsible post-2010.

I hear a lot of chatter about a boom in cash-out refinances, and the presumption seems to be that this is destined to wreak havoc on the housingmarket and the economy at some point. First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards.

Since the onset of COVID-19, the Twittersphere has been ripe with rumor and speculation that the financial requirements to qualify for a mortgage have become increasingly more rigorous since the crisis and this would put a damper on the housingmarket. Case in point — the week of March 9 and the mortgage market meltdown.

Michael Gevurtz, CEO and Founder, Bluebird Lending This article originally appeared in the February 2025 edition of MortgagePoint magazine, online now. Since 2010, Michael has focused on opportunities in the revitalization of Philadelphias emerging neighborhoods. The housingmarket will normalize despite politics.

The housingmarket is red hot. The Federal Housing Finance Agency house-price index rose 12% last year due to low inventories and high demand. And the National Association of Realtors reported that, for the first time in a generation, housing prices rose in each of the 181 metro areas it tracks at the end of last year.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housingmarket was last year — and it got a lot worse this year — it’s a blessing that was much needed. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housingmarket we had from 2002-2005.

One of the unsung heroes of the most prolonged economic and job expansion ever recorded in history was the passing of the 2005 Bankruptcy Reform Act and the 2010 qualified mortgage rule under Dodd-Frank. Both these laws paved the way for more responsible lending and a more responsible consumer. Today, we are at 1.25

The online reaction was immediate — housing must be about to crash. That’s not to say that the data points the Fed used are incorrect — in fact, we are in a savagely unhealthy housingmarket , but it’s not a bubble. First, because there is no speculative debt demand going on today, there can’t be a housing bubble.

Well, it isn’t 2008, but this type of loan does have risk — and it’s the risk that is traditional among all late economic cycle lending in America when the loan requires low or no downpayment. We have a much better housing ecosystem now for sure. The entire system has to be designed to inflate the price over time.

With the banking crisis spurring more talk of a recession, the question now is: What would housing credit look like in a recession? housingmarket would crash during the pandemic. One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages.

As 2022 proves to be a challenging year for the housingmarket, lenders are looking to take advantage of potential downtime by improving their internal processes. But when rates began to soar starting in 2005, increased foreclosure rates led to a housingmarket crash in 2008.

The latest report, which examined program data from 2010 to 2020, found no meaningful change in neighborhood poverty for program participants,” the report explained.

percent recorded in the fourth and first quarters of 2010 and 2011, and it has remained constant from previous quarters. In addition, FHFA must collect information on the creditworthiness of borrowers, including a determination of whether subprime and nontraditional borrowers would have qualified for prime lending. A further 0.6%

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. Nor can we ever have a credit sales boom again with lending standards back to normal. Case in point, purchase application data is already below 2008 levels today.

million, the existing home sales forecast represents the slowest annual pace since 2010, according to the ESR Group. New home construction is expected to pull back later in 2023 – consistent with Fannie Mae’s forecasted recession – which is due, at least in part, to tighter credit availability for construction lending.

Racial Equity Accelerator for Homeownership, a collaboration between Urban Institute and Federal Home Loan Bank (FHLB) of San Francisco , on Monday released a report that examines how the adoption of alternative data can benefit Black households within the mortgage lending landscape.

As all lenders have “skin in the game” on every loan, rigorous quality control across the lending lifecycle is imperative. Meanwhile, incomplete or inaccurate information can lead to faulty lending decisions that put lenders and their AMCs at risk.

With over 40 years of mortgage experience, Hale has held C-suite positions for some of the top housing companies in the industry, including ClosingMark Financial Group , Stearns Lending , MetLife Home Loans , MetLife Bank , Countrywide , Wells Fargo and Fleet Mortgage. Brian Hale: Purchase volume will be key.

In August, Zillow ‘s 2023 Consumer Housing Trends Report proclaimed that half of all homebuyers are purchasing their first home, the highest share that Zillow has ever recorded. One of the primary reasons for this surge is the strong presence of millennials in the housingmarket, particularly those at the peak, around ages 33 and 34.

UAD originated in 2010 and since then we appraisers are accustomed to using codes like “C4,” “N;Res,” and “1200sf0sfin” in our mortgage appraisal reports to communicate the results of our analysis. Appraisers will want to make sure that their software vendors can accommodate non-lending work in their new platforms.

The years 2020-2024 were going to be different not only for the housingmarket but also for the labor market. Just whistle, folks — that is a hot labor market. So, in essence, every American and Russian troll that has been talking about an impending recession since 2010 based on economic data has been wrong.

Chopra previously served at the CFPB from 2010-2015. In 2011, the Secretary of the Treasury designated him as the agency’s student loan ombudsman, where he led the Bureau’s efforts on student lending issues. When financial institutions take these types of actions, they risk violating the Consumer Financial Protection Act of 2010.

Campbell is now something of a JV guru, having completed over 80 joint ventures with real estate or lending firms. That, combined with the housingmarket slowdown, created a perfect storm for some questionable business practices to arise, piquing the interest of regulators. Why not create one entity to ensure a smoother process?

For the first time since 2010, homes facing low risk from natural disasters are rising in value faster than homes facing high risk, according to a new report from Redfin (redfin.com), the technology-powered real estate brokerage. We help people find a place to live with brokerage, rentals, lending, and title insurance services.

But this year, as rates have crested 6%, about 70% of Neat’s originations are adjustable-rate mortgages, a product that until recently had fallen out of favor due to the role they played in the housing crash of 2008 and a decade-plus of fixed-rate mortgages under 5%. . Not a one-size fits all”.

I have always been good with numbers, and I enjoy looking at houses,” he said. But DeZarn was an independent contractor business of one, and he lost his clients in 2008 when the housingmarket imploded. The value add is compliance, more than anything else,” said Shashank Shekhar, CEO of Arcus Lending.

A key focus of his research has been on the financial and demographic dimensions of homeownership, and the implications for housing policy. Having previously worked at the Center in the 1990s, Chris rejoined the Center in 2010 from Abt Associates, to serve as the Director of Research.

According to the Federal Housing Administration, their share of lending to Black borrowers is around 17%, compared to 6% for the rest of the mortgage market. If the program does break right, the benefits for the housingmarket are clear. In 2010, the Treasury launched the Hardest Hit Fund (HHF) program.

The Seattle area housingmarket right now reads like a mystery novel with half the pages missing. Existing home sales fell 18% between October and November for all homes on the market and are off 11% Year-on-Year (YoY). 13 to update America when the central bank will likely hold firm on short-term lending rates.

An Interesting Trend Among New Homes As a residential real estate appraiser in the Birmingham, AL market for over 30 years I have seen many changes in new home construction. Census Bureau, home size steadily increased from 1999 through 2008/2009, which we all know was when the housingmarket crashed.

Seriously though, there must be a ceiling to rising rates that have all but extinguished a robust housingmarket. While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. We are nowhere near that!

We are starting to see all of those signs following the release of September housing data from the Northwest Multiple Listing Service (MLS). Unfortunately for buyers, a combination of the typical seasonal trend and higher borrowing costs has slowed housingmarket activity to an excruciatingly slow pace – and there are concerning signs ahead.

The Seattle/King County housingmarket appears to have come through the worst of times with a slightly stronger showing in January than in previous months. Annual sales across King County totaled 21,515 homes – down an incredible 24% from the year before and the fewest since 2010 (20,761). higher than January 2023.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content