This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

million on an annualized basis – the lowest since Q3 2010. Compared to October 2022, existing home sales slumped 14.6%, down from 4.44 Fannie Mae expects Q4 seasonally adjusted existing home sales to be 3.9 Total home sales are projected to come in at around 4.8 million in 2023, 4.7 million in 2024 and 5.3 million in 2025. in 2024 and 6.9%

million in 2010. housing units, down slightly from 0.25% in 2023, and down from 0.36% in 2019, and down from a peak of 2.23% in 2010. Foreclosure filings in 2024 were also down 89% from a peak of nearly 2.9 The 322,103 properties with foreclosure filings reported on in 2024 represented 0.23% of all U.S.

My housing economic model started in 2010 and I separated my work into two different timelines. The loan profile of buyers during the post-2010 expansion is excellent. From Census : The homeownership rate of 65.7 percent was virtually the same as the rate in the fourth quarter 2023 (65.7 This leaves a lot of homeowners in place.

The expanded historical series, which spans 2004 to 2010, was developed to give the current series historical context by illuminating changes in loan availability during the previous ten years, including the housing crisis and recession that followed. Note: The expanded historical series from 2004 to 2010 does not include updated methodology.

Meanwhile, Rettinger joined Pennymac in 2010 after holding leadership roles at Bank of America and HSBC. He was then replaced by William Chang, who had joined the company in 2012 after 13 years at Credit Suisse. In October, Chang stepped down and was succeeded by Mark Elbaum. He left in June.

He said this puts todays housing market at sales levels similar to the early 1980s, apart from the brief dip in 2010 that followed the expiration of a first-time homebuyer tax credit. percentage points below the historic pre-pandemic average of 4.8%, according to Fleming.

The study notes that from 1976 to 1990, the national birthrate increased by 32%, which eventually led to an influx of young adults moving into cities by 2010. The Great Recession delayed their entry into stable jobs and housing, and by the time they emerged from the recession to buy homes, supply was scarce.

in 2024, below the 2010-2020 average of 3.5% Since February 2020, single-family rents have climbed 30%, with some markets particularly in Florida seeing even steeper increases. Miami , for instance, has experienced a staggering 52% jump over the past four years, CoreLogic added. Single-family rent growth averaged 2.6%

NetCredit referenced a recent report from Arizona State University that highlighted a 72% increase in statewide rent prices between 2010 and 2022, alongside a home-price increase of 57% between 2019 and 2023. Arizona also had three cities with little to no affordable housing options for average-income buyers.

One of these includes a 12-year stint as CEO of the San Antonio Board of Realtors from 1997 to 2010, according to his Linkedin profile. Kessler also held leadership roles across several other Texas-based Realtor associations.

The previous economic expansion, from 2010-2019, wasn’t a housing bubble. Because of this I am calling this the unhealthiest housing market post-2010. When you hear people say that the current housing market is like 2008 all over again, you may want to remind them of the huge differences between this market and that one.

After 2010, qualified mortgage laws were in place, meaning everyone getting a mortgage has to be able to repay the loan. This is what happened post 2010: The millennials started to buy homes in 2013 and they finance 90% of those homes. This matters because inventory was already heading toward all-time lows before COVID-19.

Post-2010, lending standards in America became normal again, and while I still believe they’re very liberal, they’re sane. What happened post-2010 is that exotic loan debt structures that don’t provide long-term fixed debt products left the system. I can’t emphasize enough how critical this aspect is to the American economy.

The purpose of the expanded historical series, which runs from 2004 to 2010, is to give the current series historical perspective by illustrating how credit availability has changed over the past ten years, including the housing crisis and the recession that followed.

in 2010 following the Great Recession. In 2023, the cost-burden rate for this group reached 74.2%, marking an increase of 5.4 percentage points over the last four years. This is the highest level recorded in over 20 years, surpassing the previous peak of 71.4%

average from 2010 to 2020. In January, prices for high-end rentals were 3.2% higher than a year ago, compared to December’s growth of 2.6%. Each of these numbers, however, are below the 3.5% The luxury market as a whole is poised for success in 2025, according other experts and data providers.

million new residents since 2010, with 3.7 Additionally, the number of suburban renters grew by 22% between 2010 and 2019, as compared to a 3% increase in the number of suburban homeowners during the same time period. American suburbs surrounding the nation’s 50 largest metropolitan areas gained a total of 4.7 Census Bureau data.

In addition to the bond market yield action, responsible lending post-2010 gave me confidence that forbearance was not going to be the negative issue that many had hoped for. While lending standards were never tight in American in the 21st century, they were very responsible post-2010.

Bankruptcies and foreclosures After 2010, the qualified mortgage laws came into play and all the exotic loan debt structures in the system, especially in the run-up in demand from 2002 to 2005, disappeared. Renters, younger renter households and those with lower FICO scores are the ones showing credit stress today.

Richardson Economic Consulting LLC , “Socioeconomic Consequences,” found that a key factor contributing to the decrease of affordable mortgages for low- and moderate-income families is the 2010 Dodd-Frank Act , which made small-dollar mortgages relatively more expensive to process than larger loans.

From 2010 to 2020, middle-income households gained $2.1 NAR’s Housing Wealth Gains for the Rising Middle-Class Markets study examined the distribution of housing wealth between 2010 and 2020 across income groups in 917 metropolitan and micropolitan areas. in 2010 to 29.8% In 2020, just 27.7% 10 years prior.

In 2010, CoreLogic’s national data in the fourth quarter revealed that a shocking 23.1% However, the situation has significantly improved since then, thanks to the Qualified Mortgage rule (QM) that was implemented in 2010. Most homeowners aren’t in financial distress as their cash flow has been solid since 2010, thanks to that QM rule.

Hitt began his career at Engel & Völkers Americas in 2010 and has served as the firm’s CEO and president since 2013. The brokerage firm announced Tuesday that Hitt will be stepping down from his leadership roles at the end of 2024 in order to “focus on personal endeavors.”

“The same problem is occurring nationally as well, as the number of aged investigations has steadily increased from 4,494 in 2010 to 6,145 in 2022. Despite the increase in cases, the number of investigators tasked with resolving housing discrimination claims has decreased from 622 in 2010 to 598 in 2024.”

If this happens, it would prove a dramatic contrast to that of the financial crisis, in which lenders tightened credit standards from 2007 through 2010, said Curt Long, National Association of Federally-Insured Credit Unions chief economist and vice president of research.

It’s part of the CFPB’s efforts to finally activate Section 1033 of the Consumer Financial Protection Act, a dormant legal authority enacted by Congress in 2010. This rule moves the United States closer to having a competitive, safe, secure, and reliable “open banking” system.

From 2010 to 2024, the reverse mortgage industry sought to allow remote reverse mortgage counseling in the state of Massachusetts, citing an insufficient number of actual counselors and logistical challenges for senior clients. The proposed change would be logistically difficult,” Yedinak reported in May 2010. Massachusetts Rep.

Even during the downturn of 2006-2010, this factor only hit a low of 3.84% (2010). Over the past 40+ years we have tracked this figure, the average percentage of all households (renter and owner-occupied) that purchased a home each year was 4.78% and the median was 4.64%. The factor for 2023 was 3.58%.

Homes built before 1980 saw average improvement spending that was 24% higher than for homes built since 2010, and maintenance spending was 76% higher. At the same time, the nations housing stock is aging, with a median age of 44 years in 2023 a sign of needed reinvestment.

Scarpati has served at FOA since 2010 in various roles, and he is the first occupant of this new C-suite executive position. Top-five reverse mortgage industry lender Finance of America (FOA) announced on Wednesday that it has promoted Jonathan Scarpati to the role of chief production officer.

A common theme in the interviews I have done in 2021 has been that this is the unhealthiest housing market since 2010 — not because we have a credit boom or a bubble forming, but because we have forced bidding on too few homes. This will be bullish for housing because the price gains we have been seeing are extremely unhealthy.

average during the 2010 to 2019 time period. This should ensure that initial rates on ARMs will remain low, and we also expect 30-year fixed-rate loans to remain below 3% during early 2021 and average about 3.1% during the next two years. This would be a percentage point lower than the 4.1%

The company claims on its website that the total value of homes it has appraised is over $517 billion since 2010. Also, its total value of transactions closed and recorded since 2010 is over $436 billion. The acquired company will operate as a standalone division.

Since 2010, she has served as the CEO of CAR’s for-profit subsidiary Real Estate Business Services. “It Ferrier has been part of CAR for 37 years, first serving as vice president and assistant general counsel for CAR, before serving as general counsel of CAR’s business subsidiaries.

occupied — one of the lowest numbers RealPage has recorded since 2010. Whitaker said that data should drive Austin’s rental market story. Occupancy data, for one, shows Austin at 92.5%

The expanded historical series, which spans 2004 to 2010, was developed to give the current series historical context by illuminating changes in loan availability during the previous ten years, including the housing crisis and recession that followed. The expanded historical series from 2004 to 2010 does not include updated methodology.

Serious delinquencies were up 20% from June and are now the highest they’ve been since early 2010,” Black Knight said. “In There were 2.25 In total, serious delinquencies are now 1.8 million over pre-pandemic levels.”.

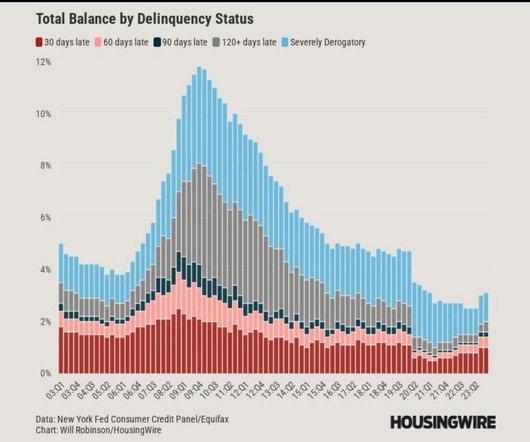

The answer is no, and for that, we must thank the 2010 qualified mortgage (QM) rule, which has high standards for borrower credit scores and the ability to repay the loan. As we can see in the chart below, 2005-2008 was awful, but from 2010-2023, the credit data looks awesome compared to the housing bubble crash years.

If we dig a little deeper into homeowners’ balance sheets, we see that since 2010, cash flow and loan quality of mortgage holders were excellent. This is an excellent article for those interested in diving into the minutiae of the 2020 refinance market. The rest of this content is for HW+ members. Join today with an HW+ Membership !

The big theme of my housing work since 2010 has been that the housing market would have its weakest recovery from 2008 to 2019 because we simply built too many homes versus the real demand curve, and monthly supply proves that. Then we had an 82% crash in new home sales, and the weakest new home sales recovery ever after 2010.

Meanwhile, existing home sales in September fell to their lowest level since 2010, Realtor.com Senior Economic Research Analyst Hannah Jones said in an emailed statement. They dropped below 4 million for the first time since October 2010, she added.

The Federal Reserve also believes this to be the case because of the better credit standards we have in place since 2010. I have stressed that to understand the housing market, you need to understand how credit channels work post-2010. Remember, if you see a forbearance crash bro , hug them, they need it.

New construction starts and permits showed surprising strength in October while existing-home sales slumped to their worst reading since 2010. “This dynamic is reflected in the latest data showing that existing home sales have fallen to a thirteen-year low.”

This is because after 2010, the loan profiles of mortgage seekers before and during the COVID crisis have been, in a word, excellent– the best loan profiles that I have ever seen in my 24 years of lending experience.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content