This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are similarities and significant differences between the housing recession we’ve seen this year versus 2008, and looking at specific factors in both timeframes gives us an idea of what to expect in 2023. Let’s look at the recessionary factors we see now versus 2008. First, we must define what we mean by recession.

Higher mortgage rates are forcing many first-time homebuyers to adopt a “wait-and-see” approach to the market. Agents reported that 27% of first-timer buyers requested mortgage rate buydowns from sellers. By comparison, first-time buyers comprised 40% of the market before 2008.

Purchase application data is now below 2008 levels! But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Post-2012, whenever mortgage rates rise, existing home sales always trend below 5 million. That happened in March of this year.

However, if home prices hadn’t skyrocketed alongside mortgage rates , we would have more younger homebuyers entering the market and we would have a slightly higher homeownership rate than todays 65.7% One was from 2008-2019 and the other was from 2020-2024. from 2008-2016. From Census : The homeownership rate of 65.7

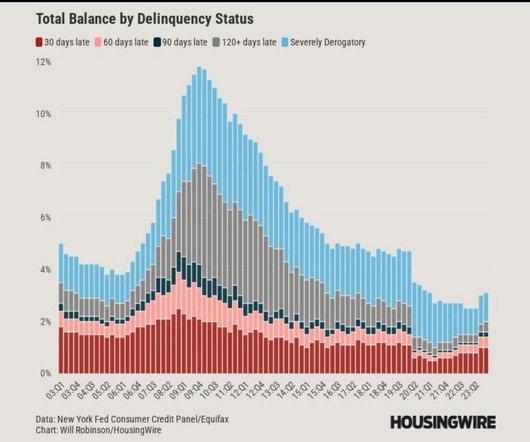

housing credit looks very different than in 2005, 2006, 2007 or 2008. Bankruptcies and foreclosures After 2010, the qualified mortgage laws came into play and all the exotic loan debt structures in the system, especially in the run-up in demand from 2002 to 2005, disappeared. The truth is, U.S.

In a new episode of “The Loan Officer Podcast,” host Dustin Owen chats with John Cornish of Iowa-based Key Mortgage Group about his path into the industry, tips for scaling a mortgage lending business and how to avoid stagnation as a loan originator. Cornish started his career in mortgage banking at Wells Fargo in Iowa in 2003.

When you hear people say that the current housing market is like 2008 all over again, you may want to remind them of the huge differences between this market and that one. Quite the opposite: In that cycle we had the weakest housing recovery ever, even with the lowest mortgage rates during the longest economic expansion ever.

The lofty home prices we’ve seen in recent months have some comparing aspects of today with those foreshadowing the housing bubble that preceded the 2008 market crash and, ultimately, what has come to be known as the Great Recession. The aftermath of the 2008 crisis led to significant attrition among real estate agents.

Movement Mortgage has named Steve Smith, a mortgage veteran who most recently served as Movement’s executive advisor, as its new president and chief financial officer. compared to the same period last year, according to Inside Mortgage Finance (IMF). The announcement was made Wednesday.

These loans pertain to multifamily mortgages, which are used for commercial properties with five or more units, such as apartment buildings. Notably, the rate of multifamily delinquencies currently stands at under 1%, but it is at levels above the 2008 recession.

However, housing demand surged when mortgage rates fell in the early 1980s during a recession. A similar situation could occur now, but we haven’t had mortgage rates low enough for long enough to increase home sales significantly. months we saw with distressed sellers in 2008. A few key notes on the charts below 1.

High mortgage rates, low inventory and sky-high prices resulted in historically low sales at a time when agents are already wrestling with the changes related to the $418 million antitrust settlement signed by the National Association of Realtors (NAR). This is particularly true for builders with in-house mortgage businesses.

The Federal Housing Finance Agency (FHFA) on Thursday announced that it initiated 43,459 foreclosure prevention actions in the third quarter of 2024, bringing the total number of homeowners helped to more than 7 million since the government-sponsored enterprises (GSEs) entered conservatorship in 2008.

Mortgage rates continued to climb this week as U.S. bond yields hit their highest level since 2008. Freddie Mac ‘s Primary Mortgage Market Survey, which focuses on conventional and conforming loans with a 20% down payment, shows the 30-year fixed rate averaged 7.09% as of August 17, up from last week’s 6.96%.

Independent mortgage banks ( IMBs ) and mortgage subsidiaries of chartered banks reported an average profit of $443 on each loan they originated in 2024, up from an average loss of $1,056 per loan in 2023, according to the Mortgage Bankers Association (MBA)’s annual Mortgage Bankers Performance Report.

As a result, Ackman claims the plan would boost the stock prices of both companies to the $30 range without putting upward pressure on mortgage rates. This would ultimately raise mortgage rates, which would be politically challenging, the KBW analysts wrote. The plan starts by cleaning up the capital structure, assuming the U.S.

This, in turn, will lead to risks of higher delinquencies for mortgages originated last year or late 2021, according to the company. The expected declines in these markets are not far from what occurred during the 2008 housing crash, when home prices in the U.S. Mortgage rates will also stay higher for longer than investors expected.

When reverse mortgage professionals from Australia and New Zealand made the long journey to San Diego last year to attend the National Reverse Mortgage Lenders Association (NRMLA) Annual Meeting and Expo, they were ready to learn about the core differences between the businesses in a different part of the world.

Describing the modern-day mortgage market as challenging would be an understatement, to say the least. Mortgage interest rates have steadily ramped up throughout 2024. The average rate throughout 2024 for 30-year fixed mortgages was 6.72% higher than it was during the 2008 market crash.

Elevated mortgage rates, sky-high home prices, tight credit and stagnant wages have all contributed to homebuyers getting older. Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008.

In 2024, second-lien mortgage programs (20) stand out with the highest number of veteran-tailored DPA programs. Grant programs (15) and first-lien mortgage programs (12) came in next. With mortgage rates expected to sink further in 2025 , program demand could continue to grow.

Digital mortgage exchange platform and loan aggregator MAXEX announced on Tuesday the hiring of mortgage technology veteran Daniel Wallace as its new chief operating officer. Wallace brings more than 30 years of experience as a leader of tech-focused mortgage, asset management and capital market platforms. “The U.S.

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. When people say credit will collapse down to 2008 levels, I kind of snicker and think, well, we can’t collapse to 2008 levels because credit availability is already there. It really is that simple, folks.

has agreed to buy a majority stake in Angel Oak Companies , the holding company for a non-QM lender and investor that manages more than $18 billion in mortgage assets. Angel Oak, founded in 2008, owns mortgage originator Angel Oak Mortgage Solutions (AOMC) and asset management arm Angel Oak Capital Advisors.

The federal government will now back mortgage loans of nearly $1 million, with the new ceiling loan limit for one-unit properties in most high-cost areas now $970,800 — or 150% of $647,200. In the third quarter, the FHFA announced that its house price index saw the largest increase since the metric was introduced in 2008.

One of the most unloved American economic success stories has been how spectacular American households with mortgage debt look today. We can see a slow and steady positive downtrend in stressed financial data, unlike in the 2005-2008 period where people filed for bankruptcies and foreclosures without a job loss recession.

A staffer who spoke with the outlet under the condition of anonymity cast doubts on the ability of the plan to succeed, citing the unregulated nature of the technology and the 2008 housing crisis as evidence of a need to proceed cautiously. I dont see any way this will help anything. I see a lot of ways this could hurt.

Movement Mortgage , a multichannel mortgage lender, has appointed Joe Thompson as its new regional director. Founded in 2008 and based in Fort Mill, South Carolina , Movement Mortgage offers a range of products including conventional, jumbo and government-insured loans, as well as a dedicated reverse mortgage division.

South Carolina-based Movement Mortgage has acquired the brokerage Superior Rate Mortgage of New England to expand operations in the region, the company announced Wednesday. Founded in 2014, Massachusetts-based Superior Rate Mortgage reached $412 million in sales volume in 2021. The terms of the deal were not disclosed.

From 1998 to 2006, according to Freddie Mac , the median annual mortgage rate was 6.45%. Mortgage rates today are not much higher than they were then. One challenging historical fact is that while mortgage rates fell from 13.24% in 1983 to 7.81% in 1996, it took that long for housing sales to reach the levels they did in 1978 to 1979.

Despite mortgage rates reaching the highest level in 14 years, mortgage applications increased 4.2% from the prior week, according to the latest Mortgage Bankers Association (MBA) survey for the week ending June 17. Rates for mortgage loans were strongly impacted by tightening monetary policy to combat rising inflation.

South Carolina-based Movement Mortgage laid off around 170 employees in March, another case of a top-25 mortgage lender paring back its workforce due to a more challenging origination landscape. . compared to the previous year, according to Inside Mortgage Finance. The higher-rate landscape is affecting all mortgage companies.

The premise of a mortgage rate lockdown is simple: so many American households have such low mortgage rates that some will never move once rates rise, which then locks up housing inventory. It all started when mortgage rates jumped from 5.25% to 6.25% this year and I saw how home sellers reacted to that move.

The recent CoreLogic Homeowner Equity Insights report for Q3 shows a continued positive trend of a lack of underwater mortgages in America today. Underwater mortgages where borrowers owe more on their home than what it is worth pose a risk of foreclosure and hinder people from selling their homes, something that was rampant after 2008.

Because each week we have 815% more sellers than last year, the total inventory will continue to build unless and until demand shifts dramatically, which would require notably lower mortgage rates. September 2024 was the moment when mortgage rates hit their lowest point of the last year. Those do not seem imminent. Its getting close.

One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages. today and why they’re so different than the period of 2002-2008. There is usually a 1.60%- 1.80% difference between the 10-year yield and 30-year mortgage rate, but now we are at 3%.

The Federal Housing Finance Agency (FHFA) this week announced a new product proposal for government-sponsored enterprise (GSE) Freddie Mac that would allow the agency to purchase certain single-family, closed-end second mortgages. FHFA Director Sandra Thompson explained that such options are needed in the current mortgage rate environment.

On the other hand, mortgage rates have gone down more than 1% since Oct. The builders’ stock prices have done well as mortgage rates have fallen , and this illustrates the simplicity of the homebuilders’ position: their story is really about mortgage rates and moving products. months and above. But since Oct.

But his first big test came in the mid-1980s during the savings and loan crisis a time when the mortgage market dried up and title companies were hit hard. Stone has previously served as vice chairman of Metrocities Mortgage and as chairman of Austin-based The Stone Group. When the 2008 financial crisis hit, what he saw alarmed him.

First-time homebuyers face higher barriers than ever before Affordability is near-record lows as mortgage payments for the median-priced home have reached historic highs. Even though homebuyers are getting older and increasingly paying cash, those taking on new mortgage debt are younger buyers from racially diverse backgrounds.

Federal Housing Finance Agency (FHFA) Director Sandra Thompson recently announced its conditional approval of Freddie Mac pilot to purchase second mortgages. Second mortgage loans are specifically authorized in Freddie Mac ’s charter [Section 305(a)(4) – 12 USC 1454(a)(4)]. That is where the Freddie Mac second mortgage comes in.

Department of Housing and Urban Development (HUD)’s Home Equity Conversion Mortgage (HECM) counseling program was cited as an example. This program provides counseling to all applicants of the federally insured reverse mortgage program, the Home Equity Conversion Mortgage program,” the report stated.

of homes with mortgages were underwater, totaling just over 11 million homes. However, the situation has significantly improved since then, thanks to the Qualified Mortgage rule (QM) that was implemented in 2010. of homes that have a mortgage. of homes that have a mortgage. What a difference a cycle makes, right?

Mortgage lenders took a loss of about $40 on each loan they originated in the fourth quarter down from a net gain of $701 per loan in the third quarter, according to the Mortgage Bankers Associations (MBA) Quarterly Mortgage Bankers Performance Report.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content