This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. A few months ago, I was asked to go on CNBC and talk about why I call this a housing recession and why this year reminds me a lot of 2018, but much worse on the four items above.

The lofty home prices we’ve seen in recent months have some comparing aspects of today with those foreshadowing the housing bubble that preceded the 2008market crash and, ultimately, what has come to be known as the Great Recession. The aftermath of the 2008 crisis led to significant attrition among real estate agents.

Notably, the rate of multifamily delinquencies currently stands at under 1%, but it is at levels above the 2008 recession. However, there is a big difference between apartment lending and homeowners who have a 30-year fixed-rate mortgage. As always, you have to examine the data closely before concluding anything on the internet.

During the previous economic expansion from 2008 to 2019, the housingmarket was subject to the constant refrain of build more homes. The previous economic expansion from 2008 to 2019 was the weakest housing recovery ever. Because that period followed a housing boom and bust when inventory was overbuilt.

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. One of the biggest reasons home sales crashed from their peak in 2005 was that the credit available to facilitate that boom in lending simply collapsed. The short (and long) answer is no, not a chance.

One of the reasons that I moved into the “team higher mortgage rate” camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housingmarket savagely unhealthy. The years 2020-2024 were always going to be different from 2008-2019. Monthly supply data being at 1.7

The 2023 housingmarket faced one of the same roadblocks we saw in 2022: mortgage rates were too high for home sales growth. Now that we’re in 2024, the Federal Reserve ‘s rate hike cycle is over, so let’s look at what that means for housing demand and home prices. Let’s look at that dynamic.

housingmarket and compare those to where we are today — in the middle of one of the most epic years in our country’s history, due to COVID-19. No doubt about it, the COVID crisis has taken some juice out of the 2020 housingmarket. The February housing data, pre-COVID, was juicy indeed. higher than a year ago.

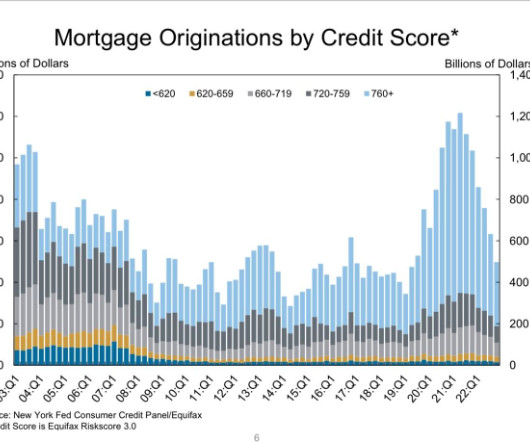

didn’t go into recession until 2008. Even though the labor market is currently showing signs of getting softer , there is no job-loss recession yet. As you can see in the chart below, there is a big difference between the current housingmarket and those looking for a repeat of 2008.

However, there are a number of attention-grabbing headlines, which unfortunately only compare today’s housingmarket to the very recent history of the last two years. It is always good to know where we are with the real estate market, but it is essential to keep all data in historical perspective. . Historically 2.5

neighborhood, housingmarket, Fall, homes, new house sales, forbearance. The Federal Reserve ’s 75 basis point interest rate hike – its largest since 1994 – proves the central bank is laser-focused on slowing inflation, but loan officers and housing economists don’t expect mortgage rates to come down until consumer prices fall.

Through numerous interviews with industry players, HousingWire assessed the rapidly changing housingmarket to determine who remains vulnerable to the higher-rate environment, and who’s primed to capitalize in the months ahead. I don’t think it’s a win for anyone on the lending side. The culling.

With the banking crisis spurring more talk of a recession, the question now is: What would housing credit look like in a recession? housingmarket would crash during the pandemic. One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages.

Homebuilder constraints Unlike the prelude to the 2008housingmarket crash, homebuilders today face unique challenges that mitigate the risk of overbuilding. Millennials, a sizable chunk of people in their prime buying years, are entering the housingmarket in force.

Post-2010, lending standards in America became normal again, and while I still believe they’re very liberal, they’re sane. This was very critical to not only the housingmarket but also the health of the U.S. The most important factor is that debt structures are vanilla.

That’s not to say that the data points the Fed used are incorrect — in fact, we are in a savagely unhealthy housingmarket , but it’s not a bubble. First, because there is no speculative debt demand going on today, there can’t be a housing bubble. housingmarket behavior for the first time since the boom of the early 2000s.

For example, from 1985-2007, housing tenure was five to seven years; from 2008-2024, it grew to 11-13 years. housingmarket, which offers a 30-year fixed mortgage, especially compared to countries like Canada that have had to try 90-year loan modifications. This is the risk of late-cycle lending in the U.S.,

The real estate market in China, both commercial and residential, have been unwinding over the last few years. in 2008 and 2009. Lax lending standards and cheap credit, plus a popular belief that real estate values never decline, created a massive bubble. Following a pattern eerily similar to the U.S.

People’s first reaction was to wonder if this was 2008 all over again. Well, it isn’t 2008, but this type of loan does have risk — and it’s the risk that is traditional among all late economic cycle lending in America when the loan requires low or no downpayment. We have a much better housing ecosystem now for sure.

It goes to show what the failure to build enough homes from 2006 to the present combined with ultra-low, unrealistic mortgage rates and massive amounts of fiscal stimulus can do to the housingmarket. This is something that housing industry leaders should be thinking about — carefully. The history of housing.

HousingWire spoke to Doug Perry, Citadel’s new managing director of Wholesale and Retail Sales, about his plans for Citadel and the current state of non-QM lending. HW: What does the demand for non-QM lending look like now following the sector’s pause earlier this year? Underlying demand for non-QM lending products remains strong.

Describing the modern-day mortgage market as challenging would be an understatement, to say the least. The average rate throughout 2024 for 30-year fixed mortgages was 6.72% higher than it was during the 2008market crash. It reflects another pressing issue of imbalanced supply and demand in the housingmarket.

. “This is about the same rate of price growth that occurred during the 2002 through 2006 period when subprime lending drove exuberant housing demand. “But that is where the similarities end.

Michael Gevurtz, CEO and Founder, Bluebird Lending This article originally appeared in the February 2025 edition of MortgagePoint magazine, online now. We were in a slow recovery from the 2008 great recession, and lenders were still hesitant to commit to projects. The housingmarket will normalize despite politics.

This article is part of our housingmarket economic update series. At the end of this series, you can join us on May 10 for a HousingMarket Update webinar. Homes that reach the market sell quickly, bidding wars are the new normal and the investor share of sales continues to rise.

Both these laws paved the way for more responsible lending and a more responsible consumer. Then we saw an uptick in people filing for foreclosures and bankruptcy during an economic expansion from 2005 to 2008. All my six recession red flags were raised toward the end of 2006, and the recession didn’t start until later in 2008.

Still, this seems like a booming housingmarket, right? I have often claimed that 2008-2019 would have the weakest housing recovery ever in history. I also said that the new home sales recovery would be fairly anemic, housing starts would never start a year at 1.5 year to date compared to 2019 levels. And it did.

But one analysis from the 2008 mortgage crisis found that “loans in majority-Black ZIP Codes were more likely to be FHA loans, suggesting that FHA played an outsized role in post-crisis homeownership in majority-Black neighborhoods,” the paper explained.

This was “likely attributable to massive government stimulus and other support programs designed to stabilize the housingmarket during the COVID-19 pandemic,” according to the report. Bias in lending is a challenge that the mortgage industry has been struggling with, as seen from a handful of suits. in 2021 from 77.7%

As 2022 proves to be a challenging year for the housingmarket, lenders are looking to take advantage of potential downtime by improving their internal processes. Applications for ARMs rose this year for the first time since interest in ARMs waned due to the role they played in the housing crash of 2008.

The Housing and Economic Recovery Act of 2008 (HERA) “codified housing goals and added a Duty to Serve, which gives FHFA the tools to ensure that Fannie and Freddie stay focused on affordable housing and serving the housing needs of low- and moderate-income families instead of using a federal backstop to just cherry-pick the most lucrative loans.”

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housingmarket was last year — and it got a lot worse this year — it’s a blessing that was much needed. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housingmarket we had from 2002-2005.

Mortgage lenders and real estate investment firms this month entered tight housingmarkets in the Midwest and the Northwest to better reach prospective homebuyers, despite a challenging mortgage market. Chicago’s housingmarket started out hot in 2022. Department of Agriculture (USDA). during the same time.

Banks have largely retreated from mortgage lending since the 2008Housing Crisis — an issue which the SVB borrower short/lend long risks are further exacerbating. CHLA might also point out that banks do not exactly have the best track record in terms of second mortgage lending.

In this series of interviews, we focus on the people who are shaping the state of housing at the top — the policy and regulation experts. The FHFA and the GSEs are essential to painting the picture of today’s housingmarket and industry trends. KS: At its peak, independent mortgage brokers represented 60% of the mortgage market.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. I have documented the history of these housing price crash addicts for a decade now. Case in point, purchase application data is already below 2008 levels today.

Despite what they promised, we sit here today with the United States housingmarket outperforming all other economic sectors in the world during the pandemic. In order for the housingmarket to crash due to too many loans going into default when forbearance programs end, the number of loans in these programs needs to grow.

The 2022 housingmarket has been underscored by interest rate spikes and refi decline and lenders are working hard to adjust to new borrower trends. However, purchase lending has faced continued downward pressure due to affordability constraints. Prioritizing home equity solutions in a rising rate environment.

housingmarket was the single best outperforming economic sector globally during the COVID-19 pandemic in 2020. Due to the solid demand for homes, housing supply for both new and existing homes are at all-time lows. 1) End forbearance plans immediately so more homes come on the market. New Home Supply. Hard pass.

The NMDB program enables FHFA to meet the statutory requirements of section 1324(c) of the Federal Housing Enterprises Financial Safety and Soundness Act of 1992, as amended by the Housing and Economic Recovery Act of 2008, to conduct a monthly mortgage market survey.

Silicon Valley Bank collapsed last week, the biggest bank failure since Washington Mutual in 2008. It will be hard to be completely confident in the near term that Sunday’s intervention will halt the pressure on smaller banks, who play a large macroeconomic role and could become considerably more conservative in their lending.”

History of the DTS program FHFA issued a final rule in 2016 that implemented the DTS provisions of the Housing and Economic Recovery Act of 2008 (HERA). Keeping stock of manufactured home supply According to 2021 American Housing Survey (AHS) , compiled by the U.S. Department of Housing & Urban Development (HUD) and U.S.

America’s fix-and-flip short-term property market is estimated to be worth as much as $68 billion a year, according to F2 Finance. The opportunity is interesting in the sense that there’s a housing shortage. We are able to essentially lend against the asset and move very quickly,” Faes said. LendInvest has more than $4.7

billion below the amount FHA analysts believe would be needed to maintain the ability to pay mortgage insurance claims in the wake of an adverse credit event similar to the 2008 financial crisis. By 2008, the capital ratio had dropped to 3.2%, and, by 2012, it had cratered into negative territory, -1.4%, requiring a $1.7

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content