This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. A few months ago, I was asked to go on CNBC and talk about why I call this a housing recession and why this year reminds me a lot of 2018, but much worse on the four items above.

Homebuyers have become older and wealthier Young people are having a particularly hard time in the housingmarket. Its no surprise that the share of first-time homebuyers has plummeted to a historic low of 24%, down from 32% last year and far below the pre-2008 norm of 40%. 26, 2025 and hear Daryl Fairweather in person.

When you hear people say that the current housingmarket is like 2008 all over again, you may want to remind them of the huge differences between this market and that one. The previous economic expansion, from 2010-2019, wasn’t a housing bubble. But is it a bubble? Become a member today. Already a member?

Purchase application data is now below 2008 levels! But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. However, the housingmarket did run into one problem in 2020. nominal per year at most.

My housing economic model started in 2010 and I separated my work into two different timelines. One was from 2008-2019 and the other was from 2020-2024. The weaker demographics for homeownership and the disappearance of exotic loan options meant that the market couldn’t maintain such high numbers for long. from 2008-2016.

Existing home sales ended the year on a positive note , which aligns with our weekly HousingMarket Tracker data, but something surprising is that home prices firmed up late in the year as well. However, housing demand surged when mortgage rates fell in the early 1980s during a recession. Also, the monthly supply is 3.3

The lofty home prices we’ve seen in recent months have some comparing aspects of today with those foreshadowing the housing bubble that preceded the 2008market crash and, ultimately, what has come to be known as the Great Recession. The aftermath of the 2008 crisis led to significant attrition among real estate agents.

housingmarket this year? If we stick to the facts, however, we can glean a few important take-homes as to what risks the housingmarket faces for 2021 and beyond. First and foremost, it is important to remember that more Americans are buying homes with mortgages in 2020 and 2021 than any single year from 2008-2019.

During the previous economic expansion from 2008 to 2019, the housingmarket was subject to the constant refrain of build more homes. The previous economic expansion from 2008 to 2019 was the weakest housing recovery ever. Because that period followed a housing boom and bust when inventory was overbuilt.

The following Q&A comes from the HW+ exclusive Slack channel, where HousingWire’s Lead Analyst Logan Mohtashami answered questions on what to make of the latest housing data, his forecast for the rest of this year, and whether or not the housingmarket is returning to normal. Become a member today. Already a member?

Just when I thought days on market were returning to normal, that number for existing homes fell back down to 22 days. If the days on the market are at a teenager level or even lower, it’s never a good sign for the housingmarket. housingmarket inventory channels have changed due to how the U.S.

The housingmarket in 2024 was about as frustrating for the real estate industry as you can imagine. Its a stunning number given how bad the market was in the years after the financial crisis in 2008. Whether 2025 will be a better market depends on who you ask. But new-home sales are a relative bright spot.

The June housing starts data beat estimates with positive revisions, however, this doesn’t change the housingmarket recession call that I made last month. We won’t see a sales decline in scale terms as we had from 2005-2008 since we simply have never had that type of sales and credit demand.

increase above the revised June estimate in housing starts in July. This means we can add housing starts to our growing collection of V-shaped recovery charts for the 2020 housingmarket. From the report: Privately-owned housing starts in July were at a seasonally adjusted annual rate of 1,496,000.

million , with double-digit home-price growth driving a housingmarket that is still savagely unhealthy. This is something that I said would change the tone of housing, and we are seeing that result this year as sales decline and inventory picks up. We are not taking the unhealthy housingmarket theme off this marketplace.

The 2022 housingmarket was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Housing recession. That would be a positive for demand.

For the housingmarket, that recovery could look different from the larger economy. and many businesses began to close, the housingmarket proved to be incredibly resilient, thriving amid record low interest rates and high consumer demand. . looks to recover from the pandemic that has gripped our nation in 2020.

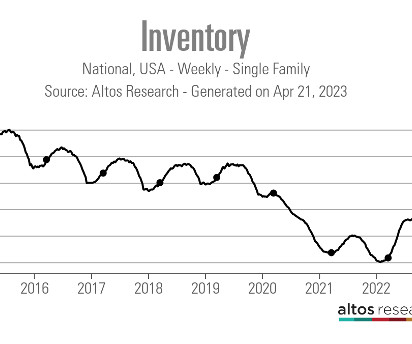

Can we now say that the housingmarket ‘s spring selling season is finally underway? Since 2020, the seasonal bottom for housing inventory has arrived several months later than normal, making it more complicated to track housing inventory data. months shows how far we are from 2008housing economics.

This will send home sales to highs not seen since before the Great Recession of 2008. Get $75 off your initial membership with coupon code “intro75” The post 2021 housingmarket forecast: What will fuel home sales? appeared first on HousingWire.

Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008. Together, the median age of all homebuyers sits at 56. The trendline is startling.

I’m talking about housingmarket crash headlines. The housing data has been wild this year. These dramatic peaks and valleys in the data have fed the demons of greed and fear that infest the minds our extreme housing bulls and the fierce housingmarket bears – leading to equally wild speculations about the future of U.S.

Today’s housingmarket suffers from affordability issues due to mortgage rates in the 7s and high home prices. People are quick to panic over any part of the housingmarket that looks stressed, fearing we’ll see 2008 levels of destruction all over again. Why choose 2011?

Since they were distressed forced sellers, inventory skyrocketed in 2006 and stayed very elevated in 2007 and 2008. Since the summer of 2020, I have believed the housingmarket could change in terms of cooling down, but it would require the 10-year yield to break over 1.94%. Total inventory levels. NAR: Total Inventory levels 1.22

The 2023 housingmarket faced one of the same roadblocks we saw in 2022: mortgage rates were too high for home sales growth. Now that we’re in 2024, the Federal Reserve ‘s rate hike cycle is over, so let’s look at what that means for housing demand and home prices. Let’s look at that dynamic.

The company notified its clients earlier this month that based on the S&P CoreLogic Case-Shiller US National Home Price NSA Index’s projected decline, the housingmarket has fallen out of favor with Goldman Sachs. The company is eyeing the San Jose, Austin, Phoenix, and San Diego markets in particular.

The weekly data shows some good news for the housingmarket ! With mortgage rates also falling, I am hopeful that more people will list their homes and buy another, so we can get back to a more functional housingmarket. But after this week’s report, we should have a low-level base formed for housing to stabilize.

A total of 30,227 homes faced foreclosure filings, a far cry from the 300,000 per month seen during the 2008 financial crisis. But this doesn’t mean risk isn’t present in today’s market. According to the monthly foreclosure report from Attom , foreclosure filings fell 5.3% compared to July and completed foreclosures dropped by 12%.

However, the real story of 2022 is that the savagely unhealthy housingmarket continues as inventory is still lower than last year, sending home prices growth into double digits again. housingmarket; the 10-year is above 1.94%, something that didn’t happen in 2020 or 2021. From NAR : Total existing-home sales dipped 2.7%

The rise of active listings in this spring housingmarket reminds me of a zombie slowly rising from its grave. Yes, we found the seasonal bottom for housing inventory on April 14, but this year’s rise in active listings has been tepid at best. Can you imagine the housingmarket at that point?

Did today’s existing home sales report give us a playbook for housing in 2024? I would argue yes, and the housingmarket today looks a lot like what we saw in late 2022. I give more details in this interview on why I believe the housingmarket dynamics shifted on Nov. months in 2008. months in Oct.

Notably, the rate of multifamily delinquencies currently stands at under 1%, but it is at levels above the 2008 recession. As always, you have to examine the data closely before concluding anything on the internet. However, there is a big difference between apartment lending and homeowners who have a 30-year fixed-rate mortgage.

didn’t go into recession until 2008. Even though the labor market is currently showing signs of getting softer , there is no job-loss recession yet. As you can see in the chart below, there is a big difference between the current housingmarket and those looking for a repeat of 2008.

housingmarket and compare those to where we are today — in the middle of one of the most epic years in our country’s history, due to COVID-19. No doubt about it, the COVID crisis has taken some juice out of the 2020 housingmarket. The February housing data, pre-COVID, was juicy indeed.

The spring housingmarket music is playing, and purchase application data and active listing inventory rose together last week. didn’t go into recession until 2008. As you can see in the chart below, there is a big difference between these two different historic housing economic cycles.

The last two years of soaring mortgage rates and rising home prices have brought the fastest erosion in housingmarket affordability in modern history, and it’s hurt first-time homebuyers the most. Inventory remains one of the driving forces in this difficult housingmarket.

This data line lags the current housingmarket as it’s a few months old. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. Even today, the MBA purchase application index is below 2008 levels. To have that market, we need total inventory data to get back to 1.52-1.93

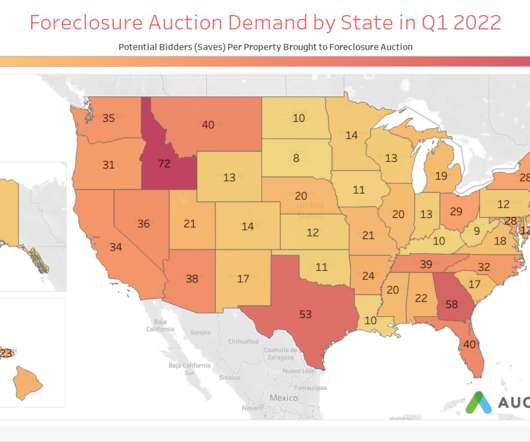

Retail housingmarket data from June showing early signs of a real estate slowdown was foreshadowed three months earlier in buyer behavior at foreclosure auctions. The downshift in buyer behavior at the foreclosure auction came two months before the downshift showed up in retail housingmarket data.

This article is part of our housingmarket update series. At the end of this series, you can join us on May 10 for a HousingMarket Update webinar. Demographics still point towards a market with strong demand – the largest cohort of millennials, the largest generation in U.S. The post Has the housingmarket peaked?

The financial and housingmarkets are still trying to sort out the banking crisis and whether we have seen the last Fed rate hike in this cycle. These events led to lower mortgage rates and increased purchase application data last week, but decreased housing inventory. In a regular market, they would be closer to 5.25%.

neighborhood, housingmarket, Fall, homes, new house sales, forbearance. The Federal Reserve ’s 75 basis point interest rate hike – its largest since 1994 – proves the central bank is laser-focused on slowing inflation, but loan officers and housing economists don’t expect mortgage rates to come down until consumer prices fall.

However, there are a number of attention-grabbing headlines, which unfortunately only compare today’s housingmarket to the very recent history of the last two years. It is always good to know where we are with the real estate market, but it is essential to keep all data in historical perspective. . Historically 2.5

The housingmarket functions differently than other markets because it can be characterized as a heterogeneous, thinly traded, illiquid market. In other words, it’s a diverse market with a wide variety of different homes of varying ages and levels of repair, and sales happen very rarely. The result is fewer sales.

Through numerous interviews with industry players, HousingWire assessed the rapidly changing housingmarket to determine who remains vulnerable to the higher-rate environment, and who’s primed to capitalize in the months ahead. The post Winners and losers of this volatile housingmarket appeared first on HousingWire.

This “higher for longer” conventional wisdom is working its way through the housingmarket. In order for the market to feel more healthy, we need more transactions. The fact that home prices are up year over year just helps us see that there is no 2008 apocalypse happening. Early in the year, people were buying at 6.5%

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content