This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Newlistings data has been moving lower over the last few weeks. The moves haven’t been significant and our weekly pending contracts data picked up this week. But, we need to see more growth in newlistings data just to grow from 2023 levels.

This is measurable in both the total unsold inventory and the number of newlistings each week. There are 358,000 single-family homes in contract right now, and they are priced only 50 basis points above last year at this time. Well, newlistings are climbing. In this chart, we have the weekly newlistings rate.

The rules of supply and demand economics always end up winning and weekly newlisting data is key. Newlisting data is growing year over year, but it will be the second-lowest newlisting data ever recorded in history. This contract data will grow if mortgage rates head lower and stay lower.

People are quick to panic over any part of the housing market that looks stressed, fearing we’ll see 2008 levels of destruction all over again. The housing bubble crash years of 2008-2011 saw a surge in foreclosures due to the lack of selling equity and this also profoundly impacted housing demand. of homes were underwater.

Some of this week’s inventory decline was helped by western Florida, which had a lot of withdrawn listings and very few newlistings due to the two hurricanes. Newlistings tick up Newlistings ticked up to 63,000 plus 10,000 more immediate sales. That happened in the 2008 bubble burst.

It happened in 2008 and then didn’t happen again until 2023. Our housing market tracker counts weekly active single-family listings, those homes that aren’t in the contract, and the raw available number of homes for sale. We have a big difference in the data on single-family permits and 5-unit permits.

Active inventory fell 1,109, and newlisting data made a lovely comeback week to week but was still noticeably down year over year. One piece of good news last week was that the newlisting data, which saw a significant collapse two weeks ago, rebounded excellently to return to a usual trend.

17-24), Inventory fell from 437,282 to 430,395 The recent inventory bottom was in 2022 at 240,194 The inventory peak for 2023 was 569,898 For context, active listings for this week in 2015 were 958,304 Newlistings data Newlistings data is growing year over year and increasing week to week, but I wish we were seeing more significant growth.

It’s not unusual for a little jump in newlistings in September. There are 345,000 single-family homes in the contract pending stage. In this chart the height of each bar is the total count of homes in contract. The light portion of the bar are the new transactions each week. This is a trend worth watching.

There is one simple reason for this: it’s not 2008. However, the glaring difference today versus the recession of 2008, is that in 2007 the builders had to deal with over 4 million active listings as competition for their pricey new homes. Let me be honest here: we got lucky as a country.

In the nearby metro area of Cape Coral-Fort Myers , active single-family inventory over the previous 90 days averaged 6,500 listings as of March 15, above its March 2020 level of 5,044 listings and approaching its March 2019 level of 7,243 listings. Smith attributes the uptick in inventory to a bump in newlistings.

Exclusivity: No Trial period: No Contract requirements: Annual contract required SmartZip is a lead generation, marketing and CRM solution founded in 2008. Smart Data With a Smart Data subscription, you’ll have access to a software platform that works with an algorithm to help you find newlistings and gain a competitive edge.

The median price of the newlistings this week is $399,900. As the summer progresses, each subsequent week of newlistings gets priced at a slight discount to the previous weeks. The median price of the homes in contract is $385,000. There are now 376,000 single-family homes in contract.

The rate of homes hitting the market was also about one-third stronger than in January 2024 and, at 2533 newlistings, it is the most of any January in four years. That is quite a rebound from late 2024 when only 950 listings hit the market for all home types single-family, townhomes and condos combined.

The chart (below) puts it in sharp focus: Except for the pandemic year of 2020 when there were 2559 newlistings that April, last month was the slowest April since at least 2008 when easy access to Northwest Multiple Listing Service data became available. Where are all the sellers? You can’t buy what’s not for sale!

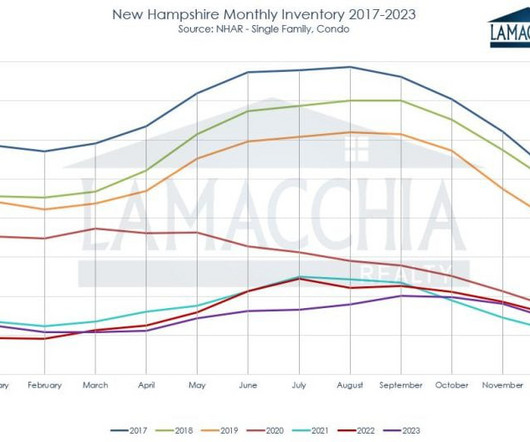

This report breaks down state-wide sales (previous years mostly covered Southern NH and the Lakes Region ), average prices, the number of active listings, and how many listings went under contract for 2023 compared to 2022, and discusses what is predicted to unfold in 2024. Average prices for closed sales increased by 7.2%

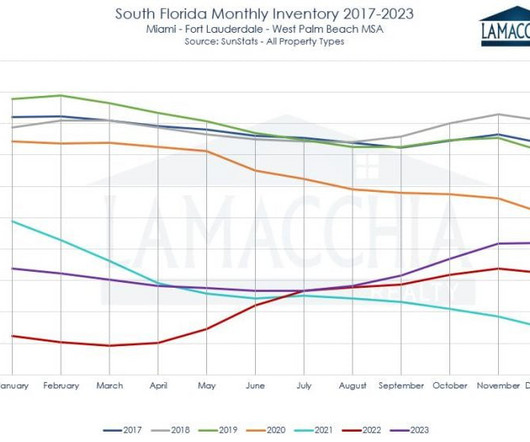

The 2023 South Florida real estate market, like national trends, saw a decrease in sales, an increase in prices, and a decrease in the number of homes listed and placed under contract. The number of homes listed decreased by 10% The number of homes placed under contract decreased by 14.1% Pending Sales Decreased by 14.1%

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2023 compared to 2022 and discusses what is predicted to unfold in 2024. Lowest number of homes listed in recorded history, decreased by 18.7% Average prices for closed sales increased by 3.4%

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. Average prices for closed sales increased by 11% The number of homes listed increased by 12.5%

Highlighted in this report are the average sale prices for single-family, condominiums, and multi-family homes in Massachusetts along with the number of homes listed for sale, placed under contract, and price adjustments. Homes Listed for Sale. People will list if they need to make a move. Sales Decrease by 11.3%.

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. The number of homes listed increased by 7.7% The number of homes placed under contract (pending) increased by 4.2%

Highlighted in this report are the average sale prices for single-family, condominiums, and multi-family homes in Massachusetts along with the number of homes listed for sale, placed under contract, and price adjustments. Pending Home Sales (contracts accepted) The number of homes placed under contract declined 20.8%

We are seeing more newlistings across the country, and it’s something we’re also seeing locally. Listings have increased much more in portions of Texas and Florida especially, so it’s important to recognize the trend isn’t the same in everywhere. Forget about other overpriced listings. It’s just not 2021 any longer.

Meantime, the number of contractlistings – known as Pending sales – rose 6.1% Realtor.com reported that our broader market (including Bellevue and Tacoma) experienced the sharpest rise in newlistings compared with last year, up 42%. The number of Active listings is another eye-opener. was up 27% YoY.

Homes Listed – All of NH. Newlistings in 2021 followed a less treacherous trendline in 2021 than 2020 but still couldn’t quite keep up with pre-pandemic markets. decrease in the state of New Hampshire brought listings to 27,131 from 28,127 the previous year. Homes Pending (contract accepted) – All of NH.

fewer newlistings, the rate of sales rose 1.7% Two data points stood out from the latest report by the Northwest Multiple Listing Service: The aforementioned newlistings for all homes in the county – 2684 – is at a low not seen for an August since records were shared with brokers (like me) dating back to the mid-1990s.

The number of newlistings for all home types – single-family, townhomes and condos combined – in King (887) fell 47% from November and declined 36% from December 2021. Homes going under contract (Pending sales) dropped 25% from the previous month and by 30% year-on-year (YoY) – staggering drop-offs.

How the housing market affects the rest of the economy How to approach the current housing market as a seller Final advice for buyers in the current housing market Are buyers pulling out of contracts at the last minute? Newlistings are down 6%, so there are less homes coming onto the market than there were this time last year.

The number of newlistings for all home types – single-family, townhomes and condos combined – in King (887) fell 47% from November and declined 36% from December 2021. Homes going under contract (Pending sales) dropped 25% from the previous month and 30% year-on-year (YoY) – staggering drop-offs.

The county saw the combined number of single-family, townhome and condo listings increase in June by 4.4% While that percentage may appear strong, it’s nothing compared to the April-to-May rise of 18%, signaling a probable cooling of newlistings in the future. New single-family-home listings rose 3.8%

You would be hard-pressed to find economists proclaiming that today’s housing environment in the PNW is nearing anything close to the 2008-type bust. the highest percentage since Q3 of 2008. ” The increased number of listings and slight slow-down of the market have helped boost inventory numbers. bath , 6920 sq.

were flipped last year, down 29% from 2022 and the largest annual drop since 2008. We are seeing more homes for sale in submarkets – except for Mercer Island and Woodinville, where active listings are down 30%+ – compared with a year ago. With the settlement, a wave of newlistings hit the market in the past several weeks.

The number of newlistings of all home types (single-family, townhome and condo) in King County climbed 6.4% (1866 units) from January to February, as expected, and total inventory at the start of March (2064) was 111% higher than a year ago. The figures are by no means a sign of a pending pricing meltdown.

We didn’t see a wave of panic selling like we did in 2008. 5) New construction in Texas surged in 2023 Three major Texas metro areas made the top 10 list of highest new home construction rates in the nation. This is probably one of the factors that kept our housing market from spiraling completely off the rails.

month backlogs of contract work, as of Q4 (latest data available), which is down from the peak of 4.8 Except for the pandemic year of 2020, last month was the slowest April since at least 2008 when easy access to Northwest Multiple Listing Service data became available. Kitchen and bath professionals are reporting 3.9-month

The excess of inventory that occurred in 2007, 2008 and ’09, was an anomaly,” said Marci Rossell, former chief economist for CNBC. There was plenty of excess in our region too, with about 23,700 listings (comprising all home types) across King and Snohomish counties in July 2008 (green). There is so much to love.

Memories of the Great Recession still linger for anyone linked to the real estate industry – including the estimated seven million households that lost their homes to foreclosures around 2008-2010. One-tenth surveyed said they have added language to contracts that require buyers to share in the materials costs if they continue to rise.

The rate today is the same as in the late 1960s, except during the housing bubble of 2008-2010 when ownership rose – and we know how that ended up! After a continued rise in sales activity through March, the number of Seattle listings under contract and newlistings have eased. month to month (436) and 6.1%

Or will we see it in the weekly newlistings volume? So even if home prices crash 20% across the board bigger than 2008 American homeowners will still have a ton of equity. There are 368,000 single-family homes in contract. Homes in contract now will close mostly in April and May. But still, more sellers.

Weekly pending sales Below is the Altos Research weekly pending contract data to show real-time demand. Weekly housing inventory data Two weeks ago, housing inventory fell a bit more than I anticipated and so did the newlistings data. I assumed that maybe the election held some people back from listing their homes.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content