This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are similarities and significant differences between the housing recession we’ve seen this year versus 2008, and looking at specific factors in both timeframes gives us an idea of what to expect in 2023. Let’s look at the recessionary factors we see now versus 2008. First, we must define what we mean by recession.

Purchase application data is now below 2008 levels! But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. It’s a first-world problem; homeowners are in perfect financial shape and control of their lives, unlike what we saw from 2005-2008.

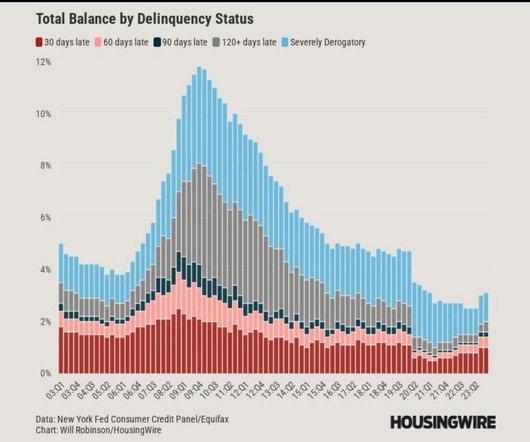

housing credit looks very different than in 2005, 2006, 2007 or 2008. As shown below, we saw massive credit stress in the data from 2005 to 2008, all before the job loss recession happened. This is very unlike 2008, where we had four years of credit stress building up in the system. The truth is, U.S.

The lofty home prices we’ve seen in recent months have some comparing aspects of today with those foreshadowing the housing bubble that preceded the 2008 market crash and, ultimately, what has come to be known as the Great Recession. The aftermath of the 2008 crisis led to significant attrition among real estate agents.

One was from 2008-2019 and the other was from 2020-2024. Boomers are staying in their homes longer, so remaining homeowners.Housing tenure doubled in America from five to seven years from 1985-2007 to 11-13 years from 2008-2025. from 2008-2016. From Census : The homeownership rate of 65.7

Notably, the rate of multifamily delinquencies currently stands at under 1%, but it is at levels above the 2008 recession. As always, you have to examine the data closely before concluding anything on the internet. However, there is a big difference between apartment lending and homeowners who have a 30-year fixed-rate mortgage.

Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008. Together, the median age of all homebuyers sits at 56. The trendline is startling.

months we saw with distressed sellers in 2008. That situation is not present in todays housing market as active inventory is almost 1 million, not 4 million like in 2007. Also, the monthly supply is 3.3 months, not the 10.8

We fell behind on home-building after 2008 and never quite caught up. Theres a shortage of affordable housing in the U.S. What can we do about it? The answer seems obvious: Build more houses, fast. Easier said than done. Theres a shortage of labor.

Cornish also dives into his experience at a local Iowa bank after leaving Wells Fargo following the post- housing crisis industry changes in 2008. Cornish: Don’t quote me on the exact year, but I think I made $19 million in 2008. I didn’t have any choice but to succeed. I can’t believe we have to verify income.

A MLS participants ability to display another brokerages listings on its own VOW site stems from a 2008 settlement between the Department of Justice and NAR. Prior to 2008 NARs rules allowed listing brokerages to opt-out of allowing another brokerage to display their listings on its website.

The Federal Housing Finance Agency (FHFA) on Thursday announced that it initiated 43,459 foreclosure prevention actions in the third quarter of 2024, bringing the total number of homeowners helped to more than 7 million since the government-sponsored enterprises (GSEs) entered conservatorship in 2008.

By comparison, first-time buyers comprised 40% of the market before 2008. HomeLight notes that this is becoming more common for existing-home sales. According to the National Association of Realtors (NAR), only 24% of recent buyers were first-timers.

Its a stunning number given how bad the market was in the years after the financial crisis in 2008. According to NAR, existing-home sales finished 2024 at a dismal 4.06 million, which is the lowest since 1995, a period when existing-home sales never topped 4 million. But new-home sales are a relative bright spot. According to U.S.

According to a National Association of Realtors (NAR) report in July, veteran homeownership has steadily increased since 2008, with veterans outpacing civilian buyers in some markets. .” Data shows that more veterans have been gearing up for homeownership in 2024.

Movement CEO Casey Crawford , a former pro football player who founded the distributed retail nonbank in 2008, said in a statement that Smith has a “track record of leading companies through aggressive growth and transformation.” compared to the same period last year, according to Inside Mortgage Finance (IMF).

million building permits issued annually, but the financial crisis of 2008 led to a sharp decline. Residential Real Estate and Housing Shortages The construction of single-family homes peaked in the early 2000s with around 1.3

The acquisition follows more than 30 made by Evernest since the company arrived on-scene in 2008. The company will acquire tech-enabled property management platform Poplar Homes alongside $15 million in growth-centered funding. The company’s management portfolio will reportedly rise to 230,000 units across 50 markets.

A staffer who spoke with the outlet under the condition of anonymity cast doubts on the ability of the plan to succeed, citing the unregulated nature of the technology and the 2008 housing crisis as evidence of a need to proceed cautiously. I dont see any way this will help anything. I see a lot of ways this could hurt.

Wallace served as managing director at financial services firm Lehman Brothers before the company went bankrupt in 2008 following the nationwide financial crisis. The new COO’s leadership journey began in the capital market sector.

This typically happens in a recession, however, the notion that credit lending in America will collapse as it did from 2005 to 2008 couldn’t be more incorrect, as we haven’t had a credit boom in the period between 2008-2022. The short (and long) answer is no, not a chance. It really is that simple, folks.

today and why they’re so different than the period of 2002-2008. However, the current housing market is much different than the credit boom-and-bust cycle of 2002-2008, and it’s vital to understand why. However, we aren’t going to see the credit availability collapse in the same way we did in 2008.

Before Compass, Sheridan also operated her own PR firm, epgPR , from 2008 to 2017. The Georgetown University graduate joined Compass in 2018 as regional public relations leader on the corporate communications team. These leadership changes follow a trend of growth moves made by Compass in 2024.

Pejacsevich and Buzzelli founded Atoka Properties before acquiring Middleburg Real Estate in 2008. In June 2023, McEnearney Associates teamed up with the Peter Pejacsevich and Scott Buzzelli-led Middleburg Real Estate/Atoka Properties. This partnership has been a natural fit from the beginning,” Pejacsevich said in a statement.

Preserving Affordable Homeownership builds on the Lincoln Institutes 2008 Policy Focus Report The City-CLT Partnership , coauthored by Davis and Rick Jacobus. CLTs remain in the picture long after a home is purchased, ensuring that affordability lasts, homes are maintained, and newly minted homeowners succeed.

Angel Oak, founded in 2008, owns mortgage originator Angel Oak Mortgage Solutions (AOMC) and asset management arm Angel Oak Capital Advisors. Brookfield will take a 50.1% Angel Oak will still operate independently, with co-foundersSreeni PrabhuandMike Fiermanremaining as co-CEOs.

First and foremost, it is important to remember that more Americans are buying homes with mortgages in 2020 and 2021 than any single year from 2008-2019. From 2008 to 2019 we had the weakest housing recovery ever, following a bust. We had no chance of reaching this number during the years 2008 to 2019.

Its no surprise that the share of first-time homebuyers has plummeted to a historic low of 24%, down from 32% last year and far below the pre-2008 norm of 40%. Nearly 40% of homeowners surveyed by Redfin admit they couldnt afford their current home if they waited to buy until today.

For example, from 1985-2007, housing tenure was five to seven years; from 2008-2024, it grew to 11-13 years. foreclosure data looks very healthy right now, especially compared to the terrible period of 2005-2008, all before the job loss recession 2008 happened. It’s good to remember that U.S.

Going into 2023, people thought housing inventory would skyrocket, home prices would crash, and we would see the housing market of 2008 all over again. In 2008, this number for that week was 249,655. From 2008-2011, new listings data averaged between 250,000 and 400,000 , peaking near 400,000 in 2011.

With home prices at all-time highs and concern that the labor market will break going into a recessionary period, is another 2008-style crash a possibility? Foreclosures and bankruptcy data One of the most prominent credit stress data lines I have ever seen came during 2005-2008. Is the U.S. headed for another housing bubble crash?

We aren’t anywhere close to the housing bubble dynamics we had from 2002 to 2008; that environment is simply impossible to replicate. In the past, the speculative credit boom led to people filing for bankruptcies and foreclosures in 2005, 2006, 2007 and 2008. Then after all that, we had the great recession.

In the third quarter, the FHFA announced that its house price index saw the largest increase since the metric was introduced in 2008. A 2008 law determines the conforming loan limits for Fannie Mae and Freddie Mac. Median home values exploded across dozens of housing markets across the country in 2021. House prices increased 18.5%

After falling out of favor due to their role in the 2008 housing crash, adjustable-rate mortgages (ARMs) have gained popularity over the past few years. Regarding the vintage 2003 to 2008 ARM loans, ICE said that their performance “remains resilient,“ with ARM delinquency rates increasing modestly compared to their fixed-rate counterparts.

The two election cycles in which home sales fell more than expected were in 2000 and 2008, years in which the economy was in a recession — with 2008 being a dramatic recession directly related to the housing market. “Of

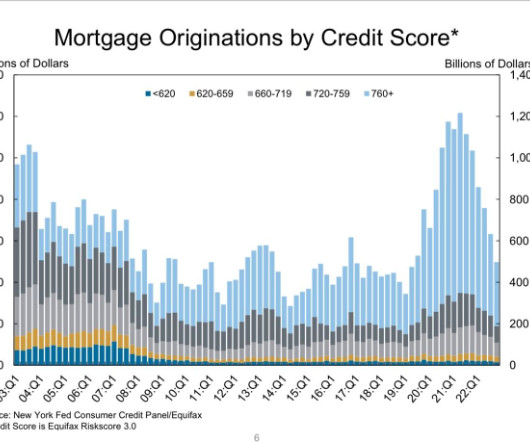

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Just look how lousy credit looked below in 2005, 2006 and 2007 — all before the job-loss recession in 2008. Demographics also play a role here.

A total of 30,227 homes faced foreclosure filings, a far cry from the 300,000 per month seen during the 2008 financial crisis. According to the monthly foreclosure report from Attom , foreclosure filings fell 5.3% compared to July and completed foreclosures dropped by 12%. But this doesn’t mean risk isn’t present in today’s market.

Now don’t get me wrong: demand is better in 2020 and 2021 than in any single year from 2008 to 2019. But we should ask: Why is inventory so much lower now if purchase application data is at 2009 levels — a period in time when inventory was rising noticeably in 2006, 2007, 2008 and 2009? Credit stress was evident from 2005 to 2008.

Longer term, HERA and conservatorship reforms have addressed the major risk characteristics of the pre-2008 version of the GSEs credit risk transfers that are being used to transfer risk away from taxpayers and to provide market discipline — a kind of early warning sign if the GSEs are going off the rails. GSE housing goals.

People’s first reaction was to wonder if this was 2008 all over again. Well, it isn’t 2008, but this type of loan does have risk — and it’s the risk that is traditional among all late economic cycle lending in America when the loan requires low or no downpayment.

last year rose to 29.6%, but still stood at the third-lowest level since 2008. The profit margin on the typical home flips around the U.S. The ROI on median-priced home flips nationwide has dropped 16 percentage points since 2020 and is off by 25 points since the highwater mark over the past decade hit in 2016.

People are quick to panic over any part of the housing market that looks stressed, fearing we’ll see 2008 levels of destruction all over again. The housing bubble crash years of 2008-2011 saw a surge in foreclosures due to the lack of selling equity and this also profoundly impacted housing demand. of homes were underwater.

Since the 2008 housing crisis , there have been significant changes that prompted the Treasury to place Fannie Mae and Freddie Mac under conservatorship. In fact, this was never the route intended by Congress when it passed HERA in 2008. So how do we get there?

from 2007 to 2008. from 2008 to 2009. in unit sales from the peak of 2005 to the trough of 2008. The next major downturn, which started in 2006, saw unit sales fall 10.3% from 2005 to 2006, then another 22.4% from 2006 to 2007 and another 20.9% There was a slight upturn in 2009, with unit sales increasing by 2.6%

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content